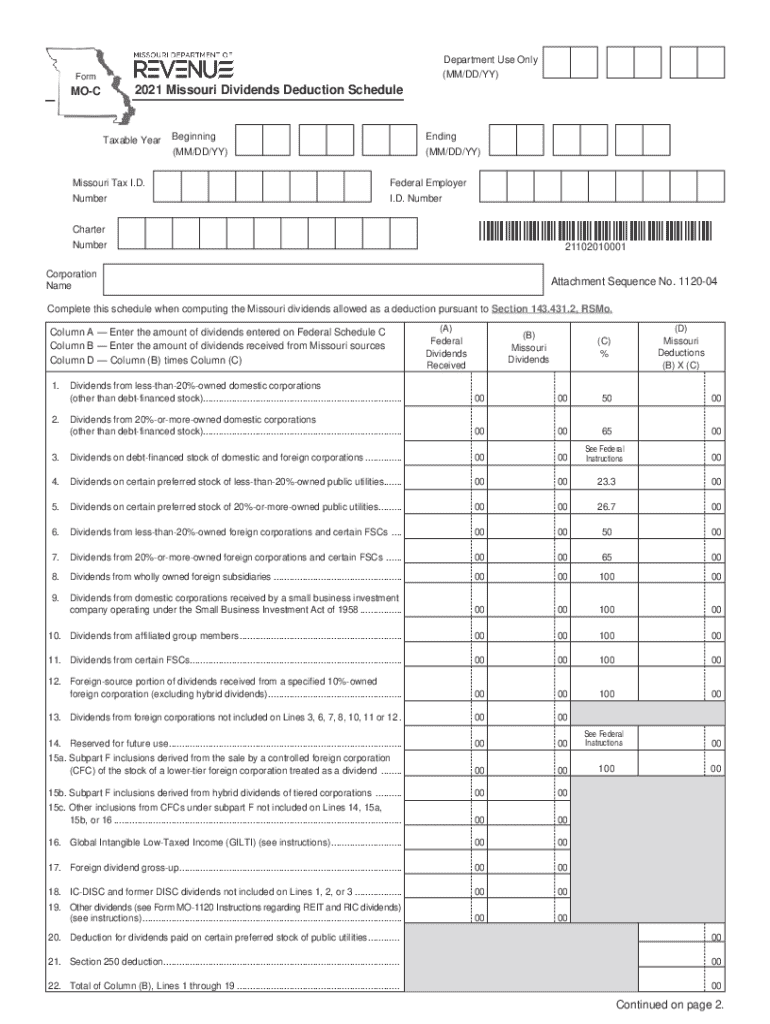

Definition and Purpose of MO-C 2021 Missouri Dividends Deduction Schedule

The MO-C 2021 Missouri Dividends Deduction Schedule is a crucial tax form used by corporations in Missouri to report and calculate allowable deductions for dividends received. This form is a reflection of Section 143.431.2 of the Revised Statutes of Missouri (RSMo), which provides guidelines for these deductions. It plays a central role in ensuring that corporations accurately calculate their dividend deductions, which ultimately affects their overall tax liabilities. Understanding this form is essential for any entity looking to reduce its taxable income through dividend deductions.

Steps to Complete the MO-C 2021 Form

-

Gather Essential Documents: Ensure you have all relevant financial documentation, including dividend statements and corporate financial records.

-

Enter Corporate Information: Begin by filling in your corporation's name, address, and taxpayer identification number (TIN).

-

Report Dividends: List all dividends received, their sources, and categorize them as domestic or foreign, as the deduction percentages may vary.

-

Calculate Allowable Deductions: Apply the applicable deduction percentage to each category of dividends based on Missouri's guidelines.

-

Summarize and Transfer Totals: Add up the deduction amounts and transfer these totals to the relevant sections of your corporate tax return.

-

Review for Accuracy: Cross-check all entries for compliance and accuracy before submission.

Key Elements of the MO-C 2021 Form

-

Taxpayer Information Section: Includes spaces for basic corporate details and TIN, which ensure proper identification of the filing entity.

-

Dividend Classification: Requires detailed breakdowns of dividends into specific categories (e.g., domestic corporations, foreign entities), influencing how deductions are calculated.

-

Deduction Calculation Area: Provides columns and rows to compute and record the allowable deductions, integral to reducing corporate tax obligations.

-

Submission Instructions: Offers guidance on where and how to submit the completed form, whether electronically or via mail.

Eligibility Criteria for Using the MO-C 2021 Form

This form is tailored for corporations based in Missouri that have received dividends and are eligible to claim deductions for these. Eligibility is determined by assessing the types of dividends received and understanding Missouri's statutory regulations surrounding these financial assets. Corporations must evaluate their dividend transactions against the standards set forth in Section 143.431.2, RSMo, to determine eligibility for deductions.

State-Specific Rules and Considerations

Missouri imposes unique rules around the classification and deduction of dividends compared to other states. These state-specific regulations dictate how deductions are applied, including varied deduction percentages for domestic versus international dividends and differing treatment of dividends from related parties. Corporations must carefully assess these distinctions to ensure compliance and optimal tax benefits.

Legal Use and Compliance Requirements

The legal foundation of the MO-C 2021 form is built on Missouri's tax laws, requiring corporations to adhere strictly to the documentation and reporting mandates stipulated. Compliance includes accurate representation of financial data, complete and truthful declarations of dividends, and submission of the form within the designated deadlines. Non-compliance can lead to significant fines or legal scrutiny.

Penalties for Non-Compliance

Failing to properly complete and submit the MO-C 2021 Missouri Dividends Deduction Schedule can result in several penalties. Corporations might face fines, interest on underpaid taxes, or audits by the Missouri Department of Revenue. Ensuring timely and accurate submission of this form, along with all required backup documentation, is crucial in mitigating such risks.

Digital vs. Paper Version of the Form

The MO-C 2021 can be filed either digitally or in traditional paper format. The digital filing option typically offers faster processing and validation by Missouri tax authorities, reducing turnaround times for any inquiries or corrections. However, the paper version is still widely accepted and may be preferred by corporations with limited access to digital tools. Each method has specific guidelines for submission, requiring careful attention to detail irrespective of format choice.

Who Typically Uses the Form MO-C 2021

The primary users of the MO-C 2021 form are Missouri-based corporations, including various business entities like C-corporations and S-corporations, subject to Missouri's corporate income tax laws. Financial professionals, including accountants and tax advisors working for these entities, also play a significant role in preparing and filing this form to ensure that their clients remain in good standing with state taxation authorities.

Important Terms Related to the Form

- Dividend: A portion of a company's earnings distributed to shareholders, key to this form as it determines deduction eligibility.

- Deduction Percentage: The rate at which dividend values can be deducted from taxable income, essential for accurate calculations on the form.

- RSMo: The Revised Statutes of Missouri, the legal context within which the form operates.

- TIN: Tax Identification Number, necessary for corporate identification on all tax-related documents.

Taxpayer Scenarios: Case Studies

-

Multi-State Corporation: A Missouri corporation with operations across state lines might apply different deduction rates based on dividend sources, affecting their taxable income in each jurisdiction.

-

Start-up Entity: A newer company starting to generate dividend income may use this form to understand potential tax savings from corporate dividends.

-

Established Large Corporation: With significant domestic and international dividend portfolios, this corporation optimally uses deductions to manage a considerable tax burden.

Each scenario provides unique challenges and opportunities in the use of the MO-C 2021, highlighting its versatility and critical role in corporate tax strategy.