Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send iht 35 via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out iht35 form with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the iht35 form in the editor.

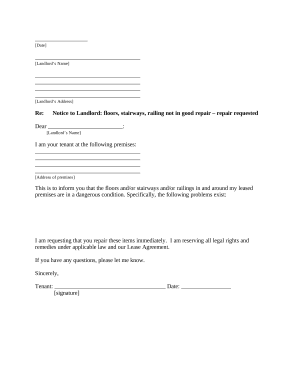

Begin by entering the deceased’s surname and first name(s) along with the date of death in the specified format (DD MM YYYY). This information is crucial for identifying the estate.

In Section 1, list all qualifying investments sold within 12 months of the date of death. Include details such as full descriptions, sale prices, and dates. Ensure you only include shares listed on recognized stock exchanges.

If there were any purchases of qualifying investments made by you in the same capacity after the date of death, answer 'Yes' in Section 2 and provide details. If not, proceed to question 3.

Complete Sections regarding any capital payments received or changes in holdings. Be thorough to ensure accuracy.

Finally, review your entries for completeness and accuracy before signing off as the appropriate person(s) at the end of the form.

Start using our platform today to fill out your iht35 form easily and for free!

by P Krnsteiner 2023 Cited by 30 This repeated heating is often termed intrinsic heat treatment (IHT) [3540]. The effect of the IHT on the microstructure of LAM-produced parts

IHT35. 1007238.583. 431119.3054. 3770. 7. 1. 12. IHT36. 1007693.23. 431640.6536. 3793 form 45 to 49 degrees F, and mean annual precipitation ranges from 12

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.