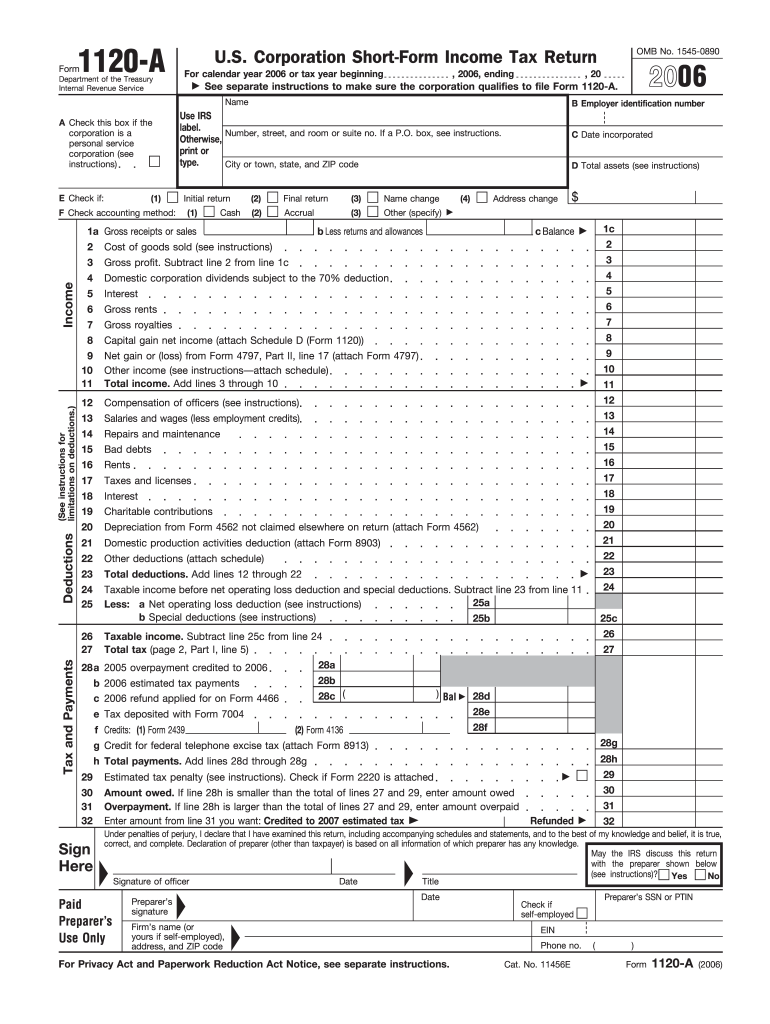

Definition and Purpose of Form 1120-A

Form 1120-A, historically recognized as the U.S. Corporation Short-Form Income Tax Return, was utilized by eligible small corporations to report income, deductions, credits, and calculate their tax liabilities for the year 2006. This form was particularly relevant for corporations with simpler financial structures due to its more concise nature compared to the regular Form 1120.

- Simplicity: Targeted corporations with straightforward operational structures.

- Scope: Included sections for gross receipts, deductions, and accounting methods.

- Eligibility: Applicable to small corporations meeting specific size and revenue criteria.

How to Use Form 1120-A

Corporations used Form 1120-A to fulfill their federal tax obligations, ensuring compliance with IRS requirements.

- Gather Financial Records: Collect income statements, receipts, and deduction records.

- Complete Required Sections: Fill in gross receipts, taxable income, and deductions.

- Calculate Tax Liability: Use information from the form to determine total taxes owed or overpaid.

- Verification: Double-check all entries for accuracy and completeness.

Obtaining Form 1120-A

Although Form 1120-A was for tax year 2006, historical copies can provide insights for educational or retrospective analysis.

- Access Methods: Available through IRS archives for historical research and reference.

- Digital Access: Can be viewed online for legacy tax scenario modeling and study.

- Paper Forms: Some tax firms may maintain archives of older forms for documentation purposes.

Steps to Complete Form 1120-A

- Input Basic Information: Enter corporation name, address, and Employer Identification Number (EIN).

- Gross Receipts & Income: Report sales, services, and other revenue streams.

- Deductions: Include business expenses like wages, rent, and supplies.

- Tax Calculations: Determine and report applicable tax credits.

- Review & Sign: Ensure all fields are completed, then sign the form for submission.

- Accuracy Check: Validate numeric calculations and entries to avoid IRS adjustments or penalties.

Key Elements of Form 1120-A

The structure of Form 1120-A provides a framework for reporting and understanding corporate financial obligations.

-

Gross Income Reporting: Explicit areas for revenue and adjustments.

-

Deductions Section: Schedules for allowable deductions under IRS guidelines.

-

Tax Liability Calculation: Methodologies to compute owed taxes.

-

Accounting Methods: Choices between accrual and cash basis for transaction reporting.

IRS Guidelines for Form 1120-A

Following IRS guidelines when completing Form 1120-A ensures compliance and accuracy.

- Income Reporting Standards: Adhering to IRS-approved methods of accounting and reporting.

- Deduction Validation: Ensuring deductions claimed are permissible and adequately documented.

- Tax Credit Application: Correctly applying eligible tax credits to lower overall tax liability.

Filing Deadlines and Important Dates

While the original Form 1120-A was for 2006, understanding past tax deadlines helps contextually.

- Typical IRS Timeline: Historical due dates around March 15 for corporations.

- Extensions: Availability for deadline extensions via Form 7004, if necessary.

- Amendments: Procedures for amending previously filed forms using Form 1120-X.

Required Documents for Form 1120-A

Preparing supporting documents helps streamline the completion and filing process.

- Income Statements: Records of all sales, services, and other income sources.

- Expense Documentation: Receipts, invoices, and records for deductible costs.

- Financial Statements: Balance sheets or profit and loss statements required for certain entries.

Understanding how these elements function together within Form 1120-A's framework provides essential insights into its application for past tax requirements.