Understanding the State Net Operating Loss ProvisionsTax Foundation

State Net Operating Loss (NOL) Provisions are designed to help businesses within a state offset taxable income with previous losses. The purpose of these provisions is to reduce tax liabilities, thereby providing relief and promoting business continuity during financial downturns. This guide examines the intricacies of the State Net Operating Loss ProvisionsTax Foundation, highlighting practical usage, legal frameworks, and specific scenarios under which these provisions apply.

How to Use the State Net Operating Loss Provisions

-

Identify Eligibility: Determine if your corporation qualifies for NOL provisions based on state-specific criteria. Typically, C corporations, S corporations, and partnerships with incurred losses can apply.

-

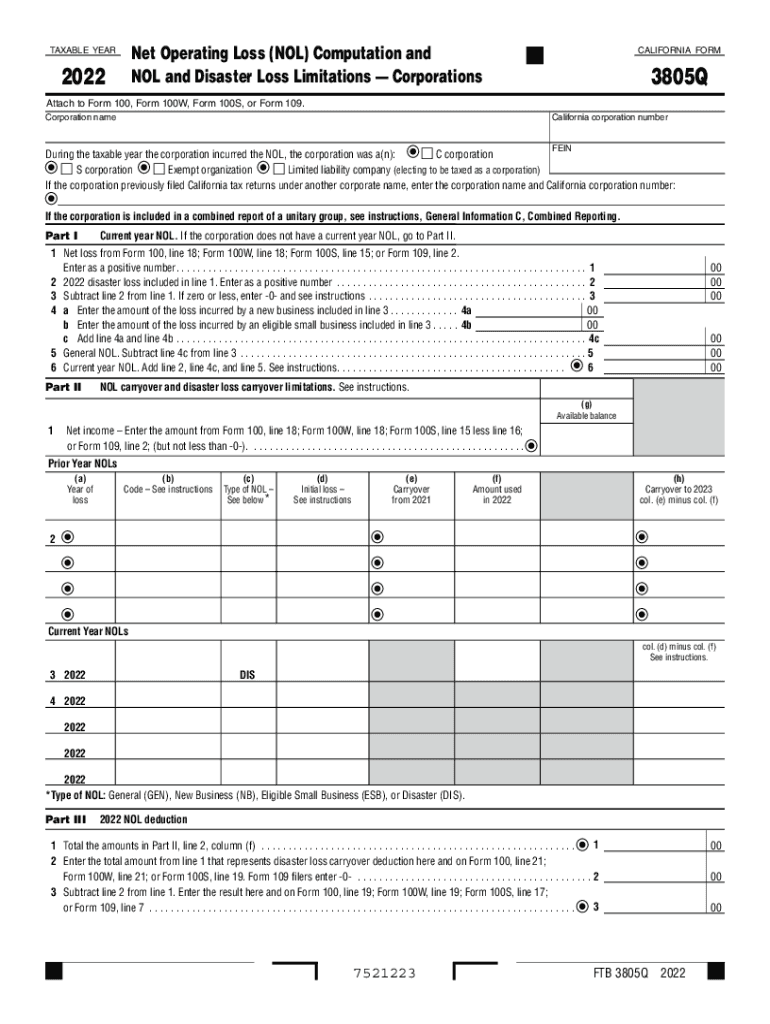

Calculate NOL: For precise calculations, businesses need to report current year losses, including any disaster loss limitations and carryovers from previous years.

-

Documentation: Ensure accurate records of loss-related documentation, including disaster loss affidavits and small business loss reports, are maintained for submission.

Steps to Complete the State Net Operating Loss ProvisionsTax Foundation

-

Form Collection: Obtain the necessary NOL forms from your state tax authority or use software compatible with these provisions like TurboTax.

-

Complete Required Sections: Fill in the sections requiring details about your business entity type, incurred losses, and any carryover calculations.

-

Attach Supplementary Documents: Include disaster loss limitations, small business deductions, and any applicable previous year carryovers.

-

Review and Submit: Double-check entries for accuracy and submit through designated channels, such as online submission platforms or mailing to the state tax office.

Important Terms Related to State Net Operating Loss Provisions

- Carryback: Refers to applying an NOL to previous tax years to receive a refund for prior paid taxes.

- Carryforward: Utilization of NOL in future years to offset future taxable income.

- Disaster Loss: Specific losses caused by declared disasters, impacting NOL calculations.

Legal Considerations for State Net Operating Loss Provisions

Compliance with legal statutes governing NOL calculations is crucial. Each state may have variations in how they handle NOL carrybacks and carryforwards. Additionally, accurate reporting is required to avoid penalties or disputes with tax authorities.

State-Specific Rules for the State Net Operating Loss Provisions

Each state might implement unique requirements regarding NOL handling:

- California: NOL suspensions may apply, and entities should adhere to disaster loss limitations.

- New York: Different NOL carryforward limits and periods may exist, requiring detailed attention to state regulations.

Examples of Using State Net Operating Loss Provisions

Consider a tech startup in California that experienced financial losses from a product launch failure. By utilizing the State NOL Provisions, it calculates the carryforward to reduce taxable income for upcoming profitable years. Each documented loss, including losses from specific years or related to economic downturns, helps in substantial tax savings.

Required Documents for Filing

- Tax forms specific to your state

- Documentation of income losses, carryovers, and any disaster-related loss documentation

- Entity type verification documents

Filing Deadlines and Important Dates

Filing deadlines vary by state and coincide with the standard corporate tax filing periods. Ensure timely compliance to avoid penalties and maximize the advantage of the NOL provisions.

Form Submission Methods

- Online Submission: Preferred for ease and speed, requiring a digital signature.

- Mail Submission: Hard copies can be mailed or filed in-person at local tax offices, depending on state preference.

Business Types Benefiting Most from NOL Provisions

Businesses experiencing variable income, such as startups, seasonal businesses, or those undergoing restructuring, stand to benefit significantly. For instance, small entities and tech companies facing initial investment losses can utilize provisions to stabilize their financial standing.

The information provided here outlines integral components of utilizing the State Net Operating Loss ProvisionsTax Foundation. This ensures businesses apply, calculate accurately, and adhere to state-specific regulations proficiently, optimizing financial strategies effectively.