Definition & Meaning

A "Pass-Through Entity Return of Income" refers to a tax form used by pass-through entities such as partnerships, S corporations, and certain types of limited liability companies (LLCs) to report their income, deductions, and credits to the Internal Revenue Service (IRS). Unlike corporations, pass-through entities do not pay income taxes at the entity level. Instead, income is reported on the personal tax returns of the owners or shareholders, who then pay taxes at their individual income tax rates. This approach helps eliminate the issue of double taxation.

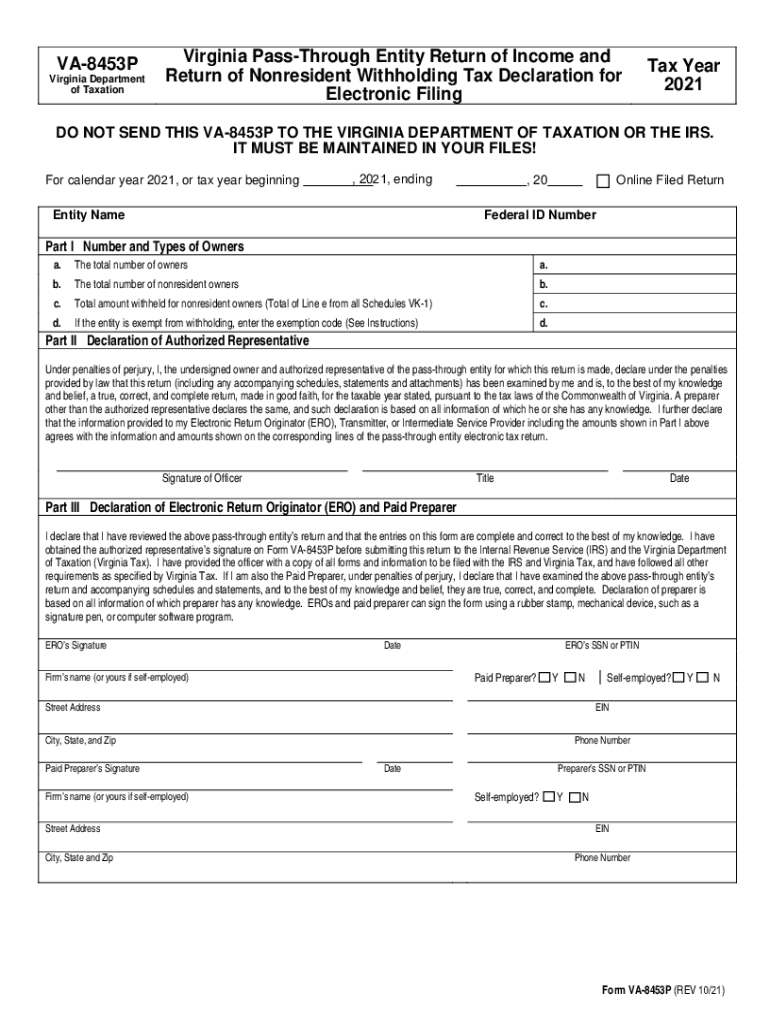

How to Use the Formalu Forms91829 Pass-Through Entity Return Of Income And Return Of

Entities must use the "formalu forms91829Pass-Through Entity Return Of Income And Return Of" to accurately report financial activities. Here’s a step-by-step breakdown:

- Collect Financial Records: Gather all relevant financial documents, including statements of income, expenses, and distributions.

- Complete Identification Section: Fill in information about the entity, such as name, address, and taxpayer identification number (TIN).

- Report Income and Deductions: Include all sources of income and claim all allowable deductions to calculate net income.

- Calculate Shareholder Allocations: Determine each shareholder’s share of the income or loss, which they will report on their individual tax returns.

- Complete Supplementary Schedules: Add supplementary schedules if needed, such as Schedule K-1, which outlines each shareholder's share of the earnings.

Steps to Complete the Formalu Forms91829 Pass-Through Entity Return Of Income And Return Of

Proper filing involves several steps:

- Identify Filing Requirements: Confirm if the entity is required to file, based on the IRS and state guidelines.

- Prepare Schedules: Complete necessary schedules, such as Schedule K-1, that report income and credits distribution among shareholders.

- Check State-Specific Instructions: Verify any additional state-specific requirements that might impact the form's completion.

- Review and Sign: Double-check the completed form for accuracy and have an authorized representative sign it.

- File Before Deadline: Submit the form by the deadline to avoid penalties.

Key Elements of the Formalu Forms91829 Pass-Through Entity Return Of Income And Return Of

Here are the key elements involved:

- Identification Information: Includes the entity’s name, address, and TIN.

- Income Reporting: Sections to report different types of income, including ordinary business income and other gains.

- Deductions and Credits: Opportunities to capture deductions and credits that reduce taxable income.

- Shareholder Information: Details about the shareholders or partners, including their percentage of ownership and income allocation.

- Tax Payments: Any estimated tax payments made during the year.

Who Typically Uses the Formalu Forms91829 Pass-Through Entity Return Of Income And Return Of

Typically used by:

- Partnerships: Entities that distribute earnings among partners.

- S Corporations: Entities that pass corporate income, losses, deductions, and credits to shareholders.

- LLCs: That elect taxation as a partnership or S corporation.

These entities utilize the form to avoid double taxation at the entity level.

Important Terms Related to Formalu Forms91829 Pass-Through Entity Return Of Income And Return Of

- Pass-Through Entities: Business structures where income is passed directly to owners or investors.

- Schedule K-1: An IRS tax form used to report income distributions from pass-through entities to their owners.

- Distributions: Payments made by a business to its shareholders or partners representing the earnings of the entity.

Filing Deadlines / Important Dates

- Federal Deadline: Typically, the deadline for filing the pass-through entity return is the 15th day of the third month after the end of the entity’s tax year. For calendar year entities, this is March 15.

- State Deadlines: Vary by state; check state-specific requirements.

- Extensions: Available if requested by filing Form 7004 prior to the original deadline.

Penalties for Non-Compliance

Entities face penalties for failing to file correctly:

- Failure to File: A penalty accrues for each month, or part thereof, the return is late, generally up to a maximum period.

- Accuracy-Related Penalties: If the IRS finds incorrect information or under-reported income, penalty charges might apply.

- Failure to Furnish K-1s: Entities must provide timely and correct Schedule K-1s to shareholders or partners. Failure results in fines.