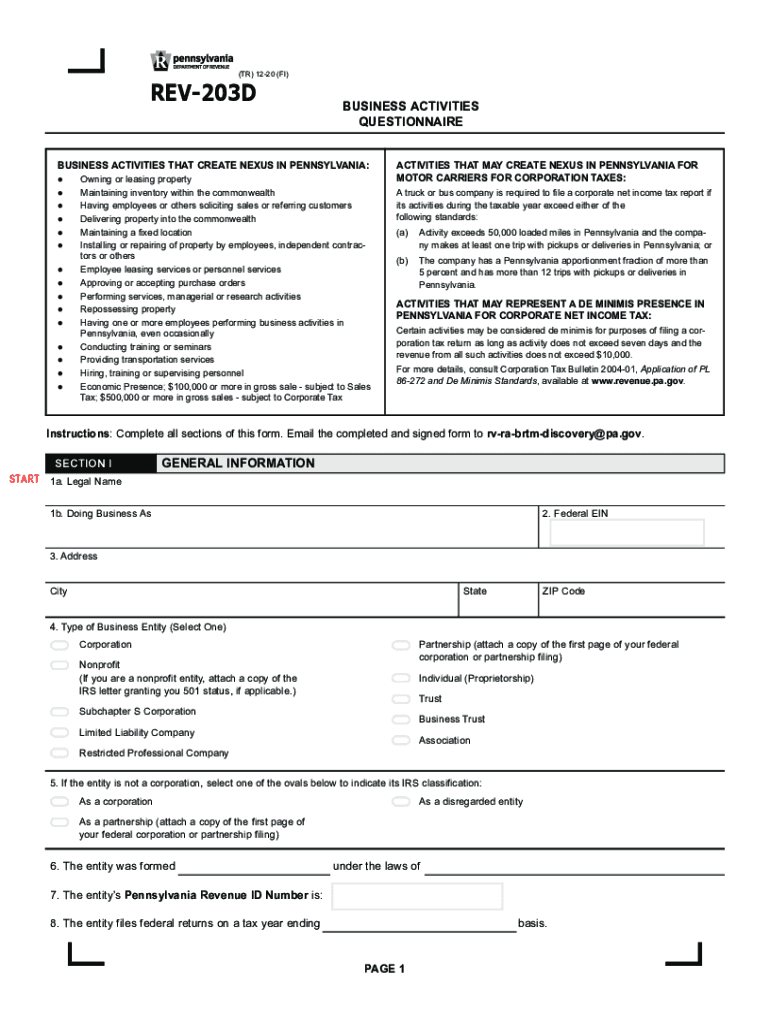

Definition & Meaning

The "rev 203d" form is a critical business activities questionnaire used by entities operating in Pennsylvania. It is designed to assess various activities that may establish a tax nexus within the state. This nexus determination is pivotal for businesses as it dictates tax obligations. Understanding the scope and purpose of the rev 203d assists businesses in ensuring compliance with Pennsylvania’s tax regulations. The form specifically addresses circumstances such as owning property, maintaining inventory, or employing staff within the state, each of which could potentially create tax implications.

How to Use the rev 203d

Entities operating in Pennsylvania must complete the rev 203d form to evaluate their business activities for tax purposes. This involves providing detailed responses about the nature and extent of business engagements within the state. Key components include information about physical presence, such as owned property or inventory, and operations, such as employee presence or sales thresholds. Businesses should carefully analyze their activities during the reporting period to ensure accurate and comprehensive reporting on the form.

Steps to Complete the rev 203d

- Gather Required Information: Collate data on property ownership, inventory levels, employee numbers, and sales activities in Pennsylvania.

- Understand Criteria: Familiarize yourself with the specific criteria that could establish a tax nexus. These include physical presence, economic activities, and personnel operations within the state.

- Complete the Form: Carefully fill out each section of the rev 203d, ensuring that all descriptions of business activities are clear and comprehensive.

- Review for Accuracy: Before submission, double-check the form for any errors or omissions that could affect the tax nexus determination.

- Submit the Form: Send the completed form to the relevant Pennsylvania tax authority by the designated deadline.

Key Elements of the rev 203d

- Business Activities Detailing: Requires in-depth disclosure of activities that might establish a tax presence in Pennsylvania.

- Federal Identification Information: Includes sections for inputting federal tax identification numbers to align state and federal tax records.

- Motor Carrier Specifics: For businesses in the transportation sector, there are specifics on how motor carriers should report their activities concerning corporate taxes.

Legal Use of the rev 203d

Filling out the rev 203d is a legal requirement for businesses operating in Pennsylvania and helps determine tax liability. Failure to accurately complete the form can lead to legal and financial repercussions, including penalties or audits. As such, businesses must approach the process seriously, focusing on precise and honest reporting. The form enforces transparency and accountability in business practices within the state.

State-Specific Rules for the rev 203d

Pennsylvania has distinct conditions under which a business entity might be obligated to submit this form. These rules are reflective of the state's efforts to ensure a fair taxation system by accurately identifying businesses that have a taxable presence. The criteria for submitting the rev 203d include variations in industries, size of operations, and the nature of business contacts with the state.

Filing Deadlines

Timely submission of the rev 203d is crucial. Businesses should be aware of specific dates by which the form must be filed each tax period. Missing these deadlines can result in penalties or increased scrutiny from tax authorities. Establishing reminders and scheduling sufficient preparation time are advisable practices for maintaining compliance with all filing requirements.

Penalties for Non-Compliance

Non-compliance with the requirements of the rev 203d form can result in significant penalties. This can involve financial penalties, interest on unpaid taxes, and potentially more severe legal consequences such as audits or restrictions on business operations. Businesses must ensure accurate and timely submission of the form to avoid such ramifications. Moreover, maintaining comprehensive documentation of activities reported on the form can provide defense in the event of disputes or audits.