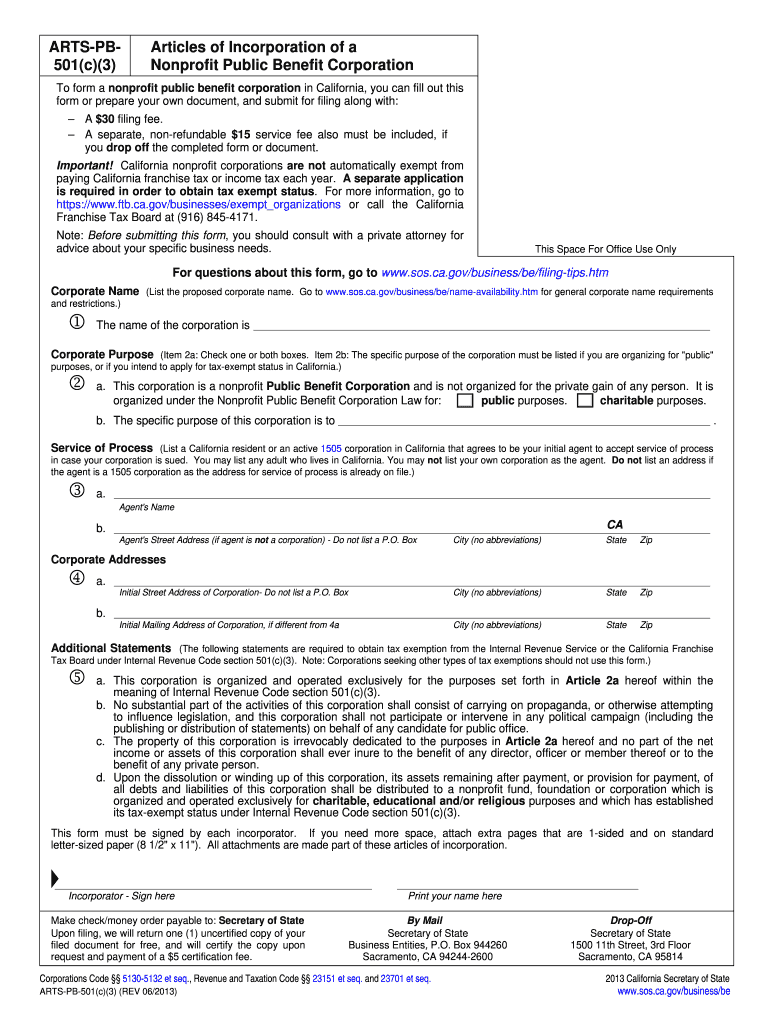

Definition and Meaning of Arts PB 501(c)(3)

The Arts PB 501(c)(3) form serves as a crucial document for organizations seeking tax-exempt status under Internal Revenue Code section 501(c)(3). This designation is reserved for nonprofit entities that operate for charitable, educational, scientific, or religious purposes. By achieving 501(c)(3) classification, organizations can benefit from tax exemptions and provide donors with the ability to make tax-deductible contributions. The term “PB” typically refers to "Public Benefit", indicating that the organization is set up for the public's advantage rather than private gain.

Organizations must clearly establish their purpose within the application, detailing how they plan to serve the community or specific public interests. To meet the IRS requirements for arts-centric nonprofits, an organization must demonstrate a strong commitment to cultural or artistic endeavors, such as promoting the arts, organizing performances, or supporting artists through various programs.

Nonprofits must also include a detailed narrative describing their mission, the population served, and how they plan to utilize funds raised. This clear definition is essential not only for IRS approval but also for gaining the trust of potential donors and stakeholders.

Steps to Complete the Arts PB 501(c)(3)

Completing the Arts PB 501(c)(3) application involves several steps, each essential to ensuring compliance with IRS regulations:

-

Define Organizational Purpose:

- Clearly articulate the mission and objectives of the nonprofit.

- Describe specific activities supporting arts and public benefit.

-

Organizational Structure:

- Establish a board of directors and create bylaws.

- Ensure adherence to state regulations regarding nonprofit governance.

-

Compile Required Documentation:

- Gather necessary documents, such as articles of incorporation, bylaws, and financial statements.

- Prepare a detailed narrative outlining the organization’s programs and how they align with public benefit.

-

Complete IRS Form 1023:

- Fill out IRS Form 1023, the application for recognition of exemption.

- Provide additional schedules relevant to the organization’s operations in the arts.

-

Review and Submit Application:

- Review the entire application for completeness and accuracy.

- Submit the completed form to the IRS along with the applicable filing fee.

-

Await IRS Determination:

- After submission, the organization should be prepared for potential inquiries from the IRS.

- Respond promptly to any requests for additional information to expedite the approval process.

Successful completion of these steps will lead to the organization being recognized as tax-exempt under 501(c)(3), enabling it to actively pursue funding opportunities and support its mission.

Important Terms Related to Arts PB 501(c)(3)

Understanding specific terms related to the Arts PB 501(c)(3) is vital for compliance and operational management:

- Tax-Exempt Status: A designation allowing organizations to avoid federal income tax on earnings related to their exempt purposes.

- Public Charity vs. Private Foundation: Public charities receive a substantial part of their funding from the general public and are subject to different regulations than private foundations, which are typically funded by a single source, such as an individual or corporation.

- Charitable Contributions: Donations made to a 501(c)(3) organization that can be deducted from a donor's taxable income.

- Articles of Incorporation: A legal document establishing the existence of a nonprofit corporation in the state in which it is formed.

- Bylaws: Internal guidelines governing the nonprofit’s operations, including the duty of the board of directors and organizational membership rules.

Familiarity with these terms will assist in navigating the legal and operational landscape of maintaining a successful arts-based nonprofit organization.

Filing Deadlines and Important Dates

Awareness of filing deadlines is critical for maintaining compliance with IRS regulations and ensuring timely processing of the Arts PB 501(c)(3) application:

- Initial Application Deadline: Organizations are encouraged to submit Form 1023 within 27 months of incorporation to qualify for retroactive tax-exempt status from the date of incorporation.

- Annual Filing Requirements: Once established, 501(c)(3) organizations must file an annual return (Form 990, 990-EZ, or 990-N) based on their gross receipts to maintain compliance and transparency.

- State-Specific Deadlines: In addition to federal requirements, organizations must adhere to their respective state laws concerning nonprofit filings and maintain their good standing by fulfilling state-mandated deadlines.

Tracking these deadlines ensures that organizations remain compliant and retain their tax-exempt status, allowing them to focus on their missions within the arts community.

Application Process and Approval Time

The application process for the Arts PB 501(c)(3) can be complex and time-consuming:

- Preparation Time: Preparing the application, including gathering all necessary documents and completing IRS Form 1023, typically takes several weeks to months depending on the organization's readiness and complexity.

- IRS Processing Time: Once submitted, the IRS can take anywhere from two to six months to process the application. Organizations should remain accessible to the IRS for follow-up questions or additional documents as required.

- Potential Delays: Factors that may extend processing times include incomplete applications, unclear organizational purposes, or failure to meet IRS requirements.

Organizations should plan accordingly and be patient through this process, as obtaining 501(c)(3) status is a significant step toward accessing funding opportunities and achieving their mission.

Examples of Using the Arts PB 501(c)(3)

Real-world applications of the Arts PB 501(c)(3) can vary widely, showcasing the diverse missions and impacts of arts-related nonprofits:

- Community Arts Centers: Many local organizations operate as arts PB 501(c)(3) entities, providing community access to arts education and performing arts programs, fostering local talent and community engagement.

- Performing Arts Organizations: These groups utilize their tax-exempt status to fund performances, workshops, and outreach initiatives aimed at promoting the cultural landscape.

- Artist Residencies and Grants: Certain organizations focus specifically on providing funding and resources to artists, facilitating their work and showcasing their contributions to the arts.

These examples illustrate how diverse nonprofits leverage the Arts PB 501(c)(3) designation to enhance public access to arts and culture while fulfilling their unique missions.