Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out 2013 sa 700 form with DocHub

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the 2013 sa 700 form in our editor.

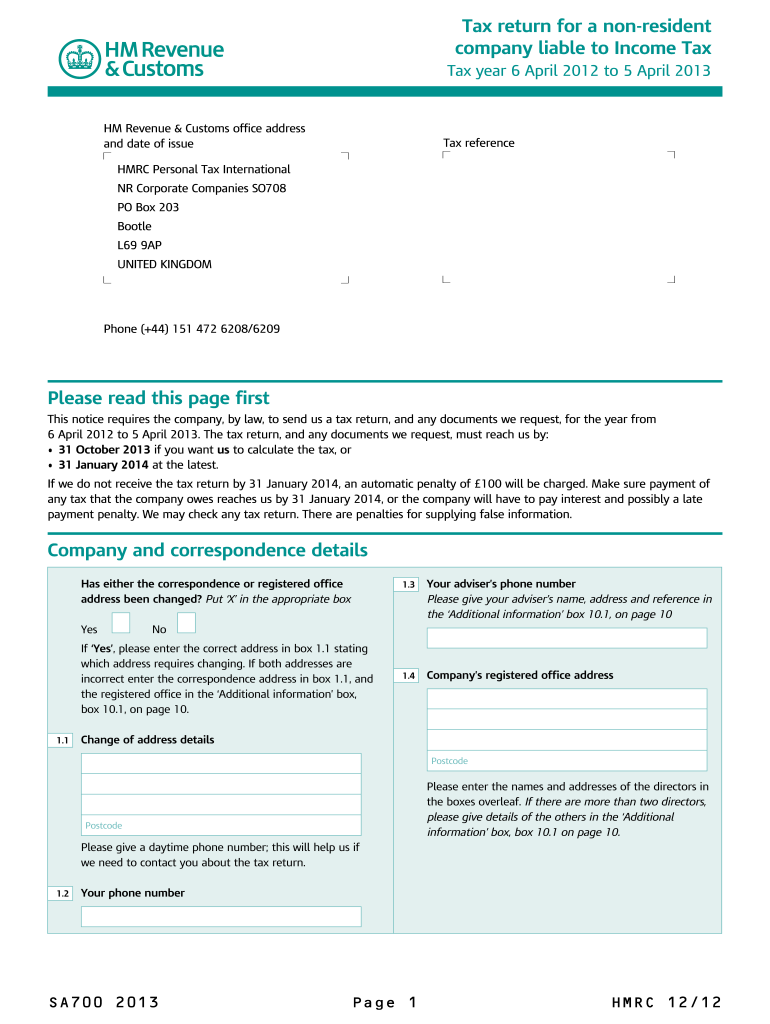

Begin by entering your company and correspondence details. Ensure that you provide accurate information for the first and second directors, including their updated addresses and phone numbers.

In the UK property income section, indicate whether your company received rental income by marking 'Yes' or 'No'. If applicable, provide details of any partnerships or unit trusts.

Fill in the furnished holiday lettings section if relevant. Enter income and expenses accurately in the designated boxes to calculate net profit.

Complete the tax adjustments section, ensuring all figures are correctly calculated based on previous entries. This includes capital allowances and balancing charges.

Finally, review all sections for accuracy before signing the declaration at the end of the form. Use our platform's features to save your progress and ensure everything is complete.

Start using our platform today to fill out your 2013 sa 700 form online for free!

Key Takeaways Examples of auditing evidence include bank accounts, management accounts, payrolls, bank statements, invoices, and receipts. Good auditing evidence should be sufficient, reliable, provided from an appropriate source, and relevant to the audit at hand.

What does SA 700 deal with?

SA 700 deals with the responsibility of the auditor in forming his/her opinion on financial statements. This standard also deals with content and form of the auditors report that is issued as an outcome of the audit of the financial statements.

What are key items in auditing?

Key items. The auditor may decide to select specific items within a population because they are important to accomplishing the objective of the audit procedure or exhibit some other characteristic, e.g., items that are suspicious, unusual, or particularly risk-prone or items that have a history of error.

What are examples of key audit matters?

Potential examples of Key Audit Matters Certain complex areas relating to revenue recognition. Provisions and contingencies. Taxation matters (multiple tax jurisdictions, uncertain tax positions, deferred tax assets) Assessment of impairment. Put arrangements over non-controlling interests. IT systems and controls.

How to report going concern in audit report?

If the auditor considers that the going concern basis is appropriate and that the disclosures are adequate, then the audit opinion will be unmodified and the auditors report will include a section headed Material Uncertainty Related to Going Concern which explains the uncertainty.

Related Searches

2013 sa 700 form pdf2013 sa 700 form pdf download2013 sa 700 form download2013 sa 700 form onlineSA700 YamahaSA100 formSA109 formSA forms

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

What are the contents of audit report as per Companies Act 2013?

CONTENTS OF AUDIT REPORT AS PER COMPANIES ACT 2013:- TRUE FAIR VIEW EXHIBITED BY THE FINANCIAL STATEMENTS [ SECTION 143(2)] AVAILABILITY OF INFORMATION EXPLANATION [ SEC. 143(3)(A)] MAINTENANCE OF PROPER BOOKS OF ACCOUNTS [ SEC. 143(3)(B)] REPORT OF THE BRANCH AUDITOR[SEC.

What are key audit matters as per SA 701?

Purpose of SA 701 Describing key audit matters provides additional information to the intended users of the financial statement, also to make them understand the matters which in the auditors judgment were of most significance for the audit of current period.

What is a key audit matter as per SA 701?

Key audit matters Those matters that, in the auditors professional judgment, were of most significance in the audit of the financial statements of the current period. Key audit matters are selected from matters communicated with those charged with governance.

Related links

Procedure Approval Processing an Agreement - SA-700

A. Section 274 of the Atomic Energy Act of 1954, as amended, (AEA) Act provides a statutory basis under which the NRC relinquishes to the States portions of

All downloadable National Academies titles are free to be used for personal and/or non-commercial academic use. Users may also freely post links to ourRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.