Overview of CG 20 10 07 04 Form

The CG 20 10 07 04 form, also known as the additional insured endorsement, is critical for businesses seeking to provide additional insurance coverage to other parties. It is commonly utilized in construction and service contracts, where different entities are involved in a project. Understanding the specifics of this form helps companies manage liabilities effectively, thus safeguarding their operations and finances.

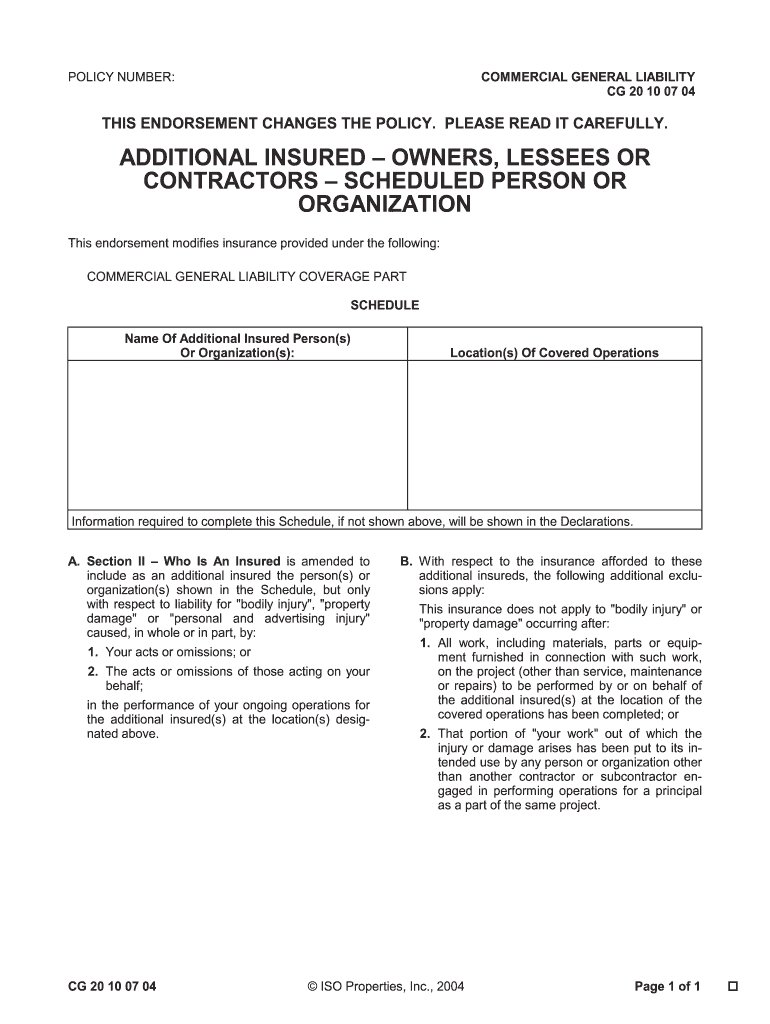

Definition and Purpose of the CG 20 10 07 04

The CG 20 10 07 04 form serves as an endorsement to a commercial general liability (CGL) policy. This endorsement allows named entities—often clients, contractors, or subcontractors—to be added as additional insureds under the primary insured's liability coverage. The primary intention of this form includes:

- Risk Mitigation: By adding additional insured parties, the primary insured helps protect them against liabilities stemming from their business activities.

- Liability Coverage: The coverage applies to various forms of liability, including bodily injury or property damage that may arise during the project's execution.

- Contractual Compliance: Many contracts require specific parties to be named as additional insureds to meet legal and regulatory obligations.

Key Elements of the Form

Understanding the critical components of the CG 20 10 07 04 is essential for effective utilization. Some notable elements include:

- Named Additional Insured Parties: Explicit identification of who qualifies for coverage under this endorsement.

- Scope of Coverage: Details the extent of liability coverage provided, which may include physical injury, property damage, and certain defense costs.

- Conditions and Exclusions: States specific conditions under which the coverage is applicable and defines exclusions that restrict coverage post-project completion.

How to Complete the CG 20 10 07 04 Form

Properly completing the CG 20 10 07 04 form is crucial to ensure all parties receive the required protection. The following steps outline the completion process:

- Identify the Insured: Provide the name and contact information of the primary insured party.

- List Additional Insured Parties: Clearly specify all additional insured individuals or entities covered under the endorsement.

- Specify Coverage Details: Define the nature of the coverage, including any limitations and specific risks covered.

- Include Effective Dates: Indicate when the coverage begins and ends to avoid lapses in protection.

- Obtain Signatures: Secure signatures from both the primary insured and the insurer to validate the endorsement.

Examples of Use Cases for CG 20 10 07 04

The CG 20 10 07 04 form is widely applicable across various industries. Here are common scenarios illustrating its practical use:

- Construction Projects: A general contractor adds subcontractors as additional insureds to cover potential liabilities arising from their work.

- Service Providers: A cleaning company adds its clients as additional insureds to ensure coverage against any accidental damages that may occur during service.

- Event Venues: An event planner lists the venue as an additional insured party during the rental agreement to protect against liability claims from attendees.

Legal Implications of the CG 20 10 07 04

The legal enforceability of the CG 20 10 07 04 form is firmly established under the federal ESIGN Act, which confirms the legitimacy of electronic signatures and documents in commercial transactions. Maintaining compliance with state laws is critical, as certain jurisdictions might have additional requirements or limitations regarding additional insured endorsements. It is also important to regularly review the legal implications and ensure that contracts align with current regulations to avoid potential disputes.

The CG 20 10 07 04 form is an invaluable tool for risk management in various business dealings. Its use helps solidify partnerships, exceed legal insurance requirements, and provide comprehensive protection against unforeseen liabilities, benefiting both the primary insured and additional parties named within the policy. Proper understanding and execution of this endorsement can lead to smoother operations and enhanced legal compliance in dynamic business environments.