Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send 1033 tax form via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out form 1033 nc irs with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

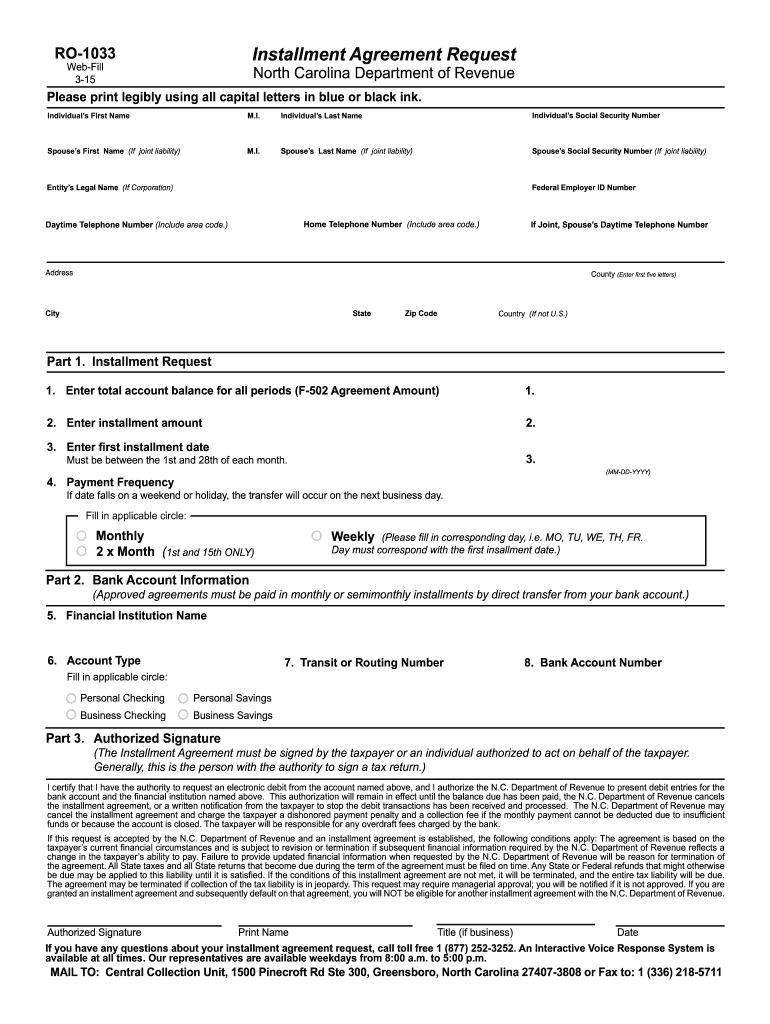

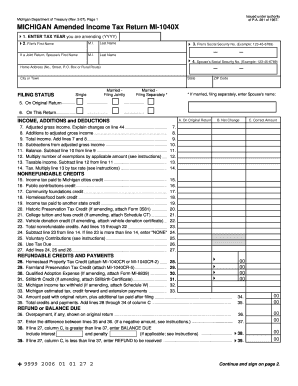

Begin by filling in your personal information, including your first name, middle initial, last name, and Social Security number. If applicable, include your spouse's details.

In Part 1, enter the total account balance for all periods and specify the installment amount you wish to pay. Choose a first installment date that falls between the 1st and 28th of the month.

Select your payment frequency by filling in the appropriate circle: Monthly, Twice a Month (1st and 15th), or Weekly. Ensure that your selected day corresponds with your first installment date.

In Part 2, provide your bank account information including financial institution name, account type, routing number, and account number. Choose whether it's a personal or business account.

Finally, in Part 3, sign the form to authorize electronic debits from your bank account. Print your name and title if applicable before submitting.

Start using our platform today to easily complete and submit your form for free!

Printable form 1033 nc irsForm 1033 nc irs pdfHow to fill out form 1033 nc irsForm RO 1033Form 1033 nc irs instructionsForm 1033 nc irs downloadNCDOR payment onlineNCDOR payment history

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Feb 28, 2026 Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No.Read more

Form 1023-EZ is used to apply for recognition as a tax-exempt organization under Section 501(c)(3). Applicants can learn more about the requirements,Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.