Definition & Meaning

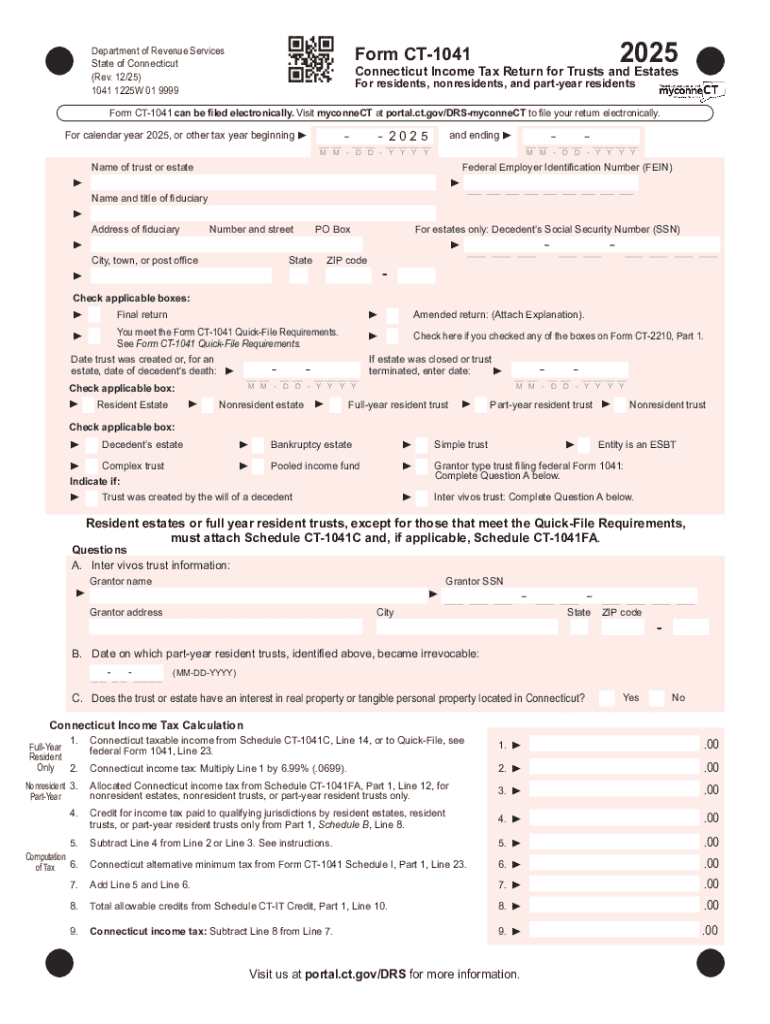

The Connecticut Income Tax Return for Trusts and Estates, often referenced as Form CT-1041, is a crucial document required by the state of Connecticut for reporting income, deductions, and other tax-related information for trusts and estates. This form is essential for ensuring compliance with state tax laws regarding the fiduciary responsibilities of trusts and estates. It captures vital details such as income distributions to beneficiaries and the calculation of fiduciary tax liabilities, playing a critical role in the annual tax filing process for these entities.

How to Use the Connecticut Income Tax Return for Trusts and Estates

Using the Connecticut Income Tax Return for Trusts and Estates involves several key steps, beginning with accurately completing the form based on detailed financial records.

-

Preparation: Gather all income statements, including interest, dividends, and capital gains, from both domestic and international sources.

-

Completing the Form: Fill out the form with precise numbers, ensuring that all income categories are appropriately classified. Pay special attention to the section concerning distributions to beneficiaries, as these figures affect individual tax obligations.

-

Submitting the Form: Depending on your preference and situation, submit the completed form electronically through the Connecticut Department of Revenue Services' online portal or via mail, ensuring it meets the filing deadline to avoid penalties.

Steps to Complete the Connecticut Income Tax Return for Trusts and Estates

To effectively complete the CT-1041 form, follow this detailed guide:

-

Identify the Trust or Estate: Start by listing the name, address, and federal Employer Identification Number (EIN) of the trust or estate.

-

Report Income: Carefully document all sources of income, including wages, dividends, abatements, and other financial returns related to the trust or estate.

-

Deductions and Credits: Fill in allowable deductions such as administrative expenses, charitable contributions, and taxes paid to other states.

-

Calculate Tax Liability: Using the provided tax tables, determine the total tax liability before adjustments and payments.

-

Sign and Date: Ensure that the fiduciary or authorized representative signs and dates the form, verifying the accuracy of information provided.

Important Terms Related to Connecticut Income Tax Return for Trusts and Estates

Understanding the language used in CT-1041 is crucial for accurate completion:

- Fiduciary: An individual or organization responsible for managing another’s assets for their benefit. This can apply to individuals overseeing an estate or trustees managing a trust.

- Beneficiary: A person or entity entitled to receive benefits from a trust or estate.

- Distributable Net Income (DNI): The income available to be distributed to beneficiaries, affecting their personal tax liabilities.

Filing Deadlines / Important Dates

Form CT-1041 must be filed annually, with the due date typically falling on the 15th day of the fourth month following the close of the tax year (mid-April for calendar-year filers). Extensions may be requested, but any taxes owed must be paid by the original filing deadline to avoid interest and penalties.

Required Documents

To accurately complete and file the Connecticut Income Tax Return for Trusts and Estates, gather the following:

- Annual Financial Statements: Detailing income and expenditures.

- Previous Year’s Tax Return: Provides a baseline for current-year comparisons.

- Statements of Deductions and Credits: Documentation supporting any claimed reductions in tax liability.

State-specific Rules for the Connecticut Income Tax Return for Trusts and Estates

Connecticut has unique rules for trusts and estates that may not apply in other states:

- Connecticut-specific Deductions: These might include particular credits for income distributed to beneficiaries who are Connecticut residents.

- Nonresident Beneficiaries: There are specific guidelines for handling income distributed to nonresidents.

Penalties for Non-Compliance

Failure to comply with filing requirements for the Connecticut Income Tax Return for Trusts and Estates can result in significant penalties:

- Late Filing Penalty: A percentage of the tax due for each month or part of a month the return is late.

- Underpayment of Tax Penalty: Additional charges for failing to pay tax owed by the due date.

Comprehending these elements ensures thorough and compliant filing, leveraging tools like DocHub to streamline document handling and reduce paperwork burdens efficiently.