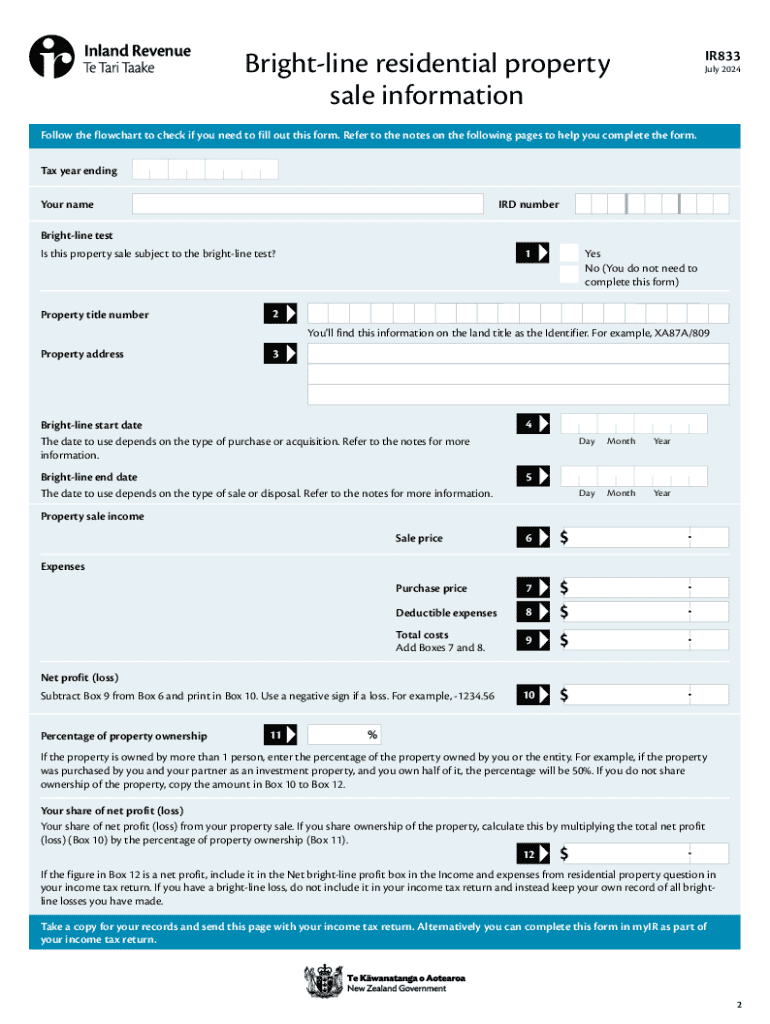

Definition & Meaning of the Bright-line Residential Property Sale Form IR833

The Bright-line Residential Property Sale Form IR833 is a critical document used for tax purposes in the United States, particularly when dealing with the sale of residential properties. It is primarily designed to record and report any financial gains or losses incurred from such sales. This form is essential for individuals who have sold residential property within a specific timeline and need to declare the income or loss from the transaction. The term "Bright-line" refers to the clear guidelines set by tax authorities to distinguish short-term property transactions that are subject to specific tax obligations.

Key Features and Purpose

- Reporting Financial Outcomes: Captures income or loss related to property sales.

- Regulatory Compliance: Ensures adherence to the IRS's tax regulations.

- Clarity in Property Sales: Helps taxpayers understand their obligations under the bright-line test.

Importance for Taxpayers

Engaging with this form ensures that individuals comply with federal tax laws and avoid potential penalties. The form serves as a transparent record in an individual’s tax filings, reflecting accurate financial outcomes from property sales.

How to Use the Bright-line Residential Property Sale Form IR833

Step-by-Step Instructions

- Identify Transaction: Gather all relevant financial documents related to the property sale.

- Complete Personal Information: Fill out the taxpayer’s name, Social Security Number, and contact details in the designated sections.

- Enter Property Details: Record the address of the sold property and the sale date.

- Calculate Gain or Loss: Use the provided sections to calculate the difference between the sale price and the purchase price, accounting for additional expenses or improvements.

- Complete the Declaration: Ensure all required fields contain accurate and complete information.

Common Mistakes to Avoid

- Missing Information: Double-check for all details before submission.

- Incorrect Calculations: Verify figures with appropriate financial records to ensure accuracy.

Practical Tips

- Consult with a Tax Professional: For complex situations or when in doubt, seek professional advice to guarantee compliance and accuracy.

Steps to Complete the Bright-line Residential Property Sale Form IR833

Detailed Guide

Step 1: Gather Required Documents

- Sale and Purchase Agreements: Essential for determining sale and purchase prices.

- Receipts for Improvements: Include any documentation of property improvements.

- Closing Statements: Necessary for final transaction details.

Step 2: Fill Out the Form

- Section A: Fill in the taxpayer’s personal and property details.

- Section B: Use this section for financial calculations, including any losses or gains.

- Verification: Review the form for errors or omissions before submitting.

Example Scenario

John sold his residential property in 2023. He collected all the relevant documents, such as the sale agreement and receipts for improvements. By meticulously completing each section of Form IR833, John ensured an accurate representation of his transaction, thereby complying with tax regulations.

Key Elements of the Bright-line Residential Property Sale Form IR833

Main Components

- Personal Information Section: Captures essential taxpayer identity details.

- Property Transaction Details: Provides specifics about the property involved in the transaction.

- Calculation of Gain or Loss: Integral for determining tax obligations.

Special Considerations

- Time-Sensitive Submissions: Ensure that the form is filed within deadlines to avoid penalties.

- Multiple Property Transactions: Separate forms may be necessary for each property sale.

Final Checks

- Verify all entries against original documents.

- Ensure alignment with personal tax reporting to the IRS.

Legal Use of the Bright-line Residential Property Sale Form IR833

Regulatory Compliance

Understanding and utilizing this form is crucial for meeting U.S. tax requirements. It offers individuals a standardized method to report gains or losses, crucial for calculating potential taxes owed under the bright-line rules.

Legal Framework

- Adheres to IRS Guidelines: Ensures compliance with specific U.S. federal tax laws associated with property sales.

- Documentation for Audits: Serves as supporting evidence if audited by tax authorities.

Why Legal Compliance Matters

Successfully navigating the legal requirements surrounding property sales can shield taxpayers from fines, penalties, or additional scrutiny from tax authorities.

Important Terms Related to Bright-line Residential Property Sale Form IR833

Glossary of Key Terms

Bright-line Test

A threshold set by tax authorities to determine tax obligations based on the duration a property is held before being sold.

Capital Gains

The profit derived from the sale of property or any other significant asset.

Taxable Income

The portion of an individual’s or entity’s income subject to taxation, which, in relation to property sales, depends on the calculated gain or loss.

Clarifying Misunderstandings

- Capital vs. Ordinary Income: Distinguish between gains that are capital in nature versus those considered ordinary income for tax purposes.

Penalties for Non-Compliance with the Bright-line Residential Property Sale Form IR833

Potential Consequences

Fines and Penalties

- Monetary: Financial penalties may apply for late submission or inaccurate filings.

- Legal Action: Continuous non-compliance can lead to more severe legal consequences.

Preventive Measures

- Timely Filings: Regularly update tax records and meet all filing deadlines.

- Accurate Reporting: Ensure all information submitted is correct and verifiable to avoid financial and legal repercussions.

Learning from Mistakes

Examining case studies of past compliance failures helps in understanding common pitfalls and how to avoid them proactively.

Software Compatibility and Form Submission Methods for the Bright-line Residential Property Sale Form IR833

Digital vs. Paper Version

Software Compatibility

- Supported Platforms: Compatible with mainstream tax preparation software like TurboTax and QuickBooks, which can streamline the completion process.

- Integration Benefits: Easily integrates with online platforms for automated calculations and submissions.

Submission Methods

- Online Filing: Submit the form electronically for faster processing.

- Mailing Option: For those preferring traditional methods, the form can also be mailed directly to the IRS.

- In-Person Submissions: Certain situations may allow for physical submissions at IRS offices, although this is less common.

Advantages of Electronic Submission

The electronic filing process minimizes errors and provides immediate confirmation of receipt, significantly reducing potential delays and complications.

By adhering to these guidelines and procedures, individuals can efficiently manage their tax obligations related to property sales, ensuring compliance and accuracy in their filings.