Definition & Meaning

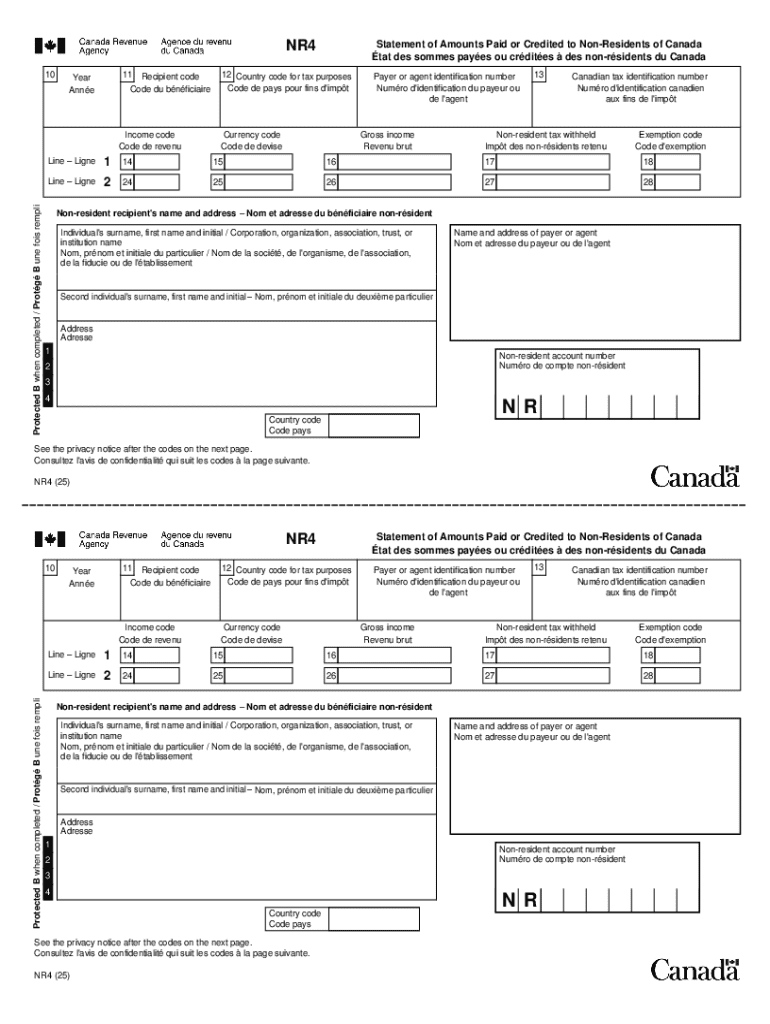

The "NR4 Statement of Amounts Paid to Non-Residents of Canada" is a document used by Canadian payers to report income paid or credited to non-residents of Canada. This income may include interest, dividends, rents, royalties, and pensions. The NR4 form communicates to both the Canada Revenue Agency (CRA) and the non-resident recipient about the income earned and any Canadian tax withheld. Understanding the form's purpose helps non-residents manage their Canadian tax obligations and ensures compliance with Canadian tax laws.

Importance of the Form

- Tax Compliance: Ensures accurate reporting of income by non-residents to the CRA.

- Verification for Tax Authorities: Helps Canadian and foreign tax authorities verify reported income.

- Income Record: Acts as a formal statement of income for non-residents.

How to Use the NR4 Statement of Amounts Paid to Non-Residents of Canada

To effectively use the NR4 form, recipients should first understand the types of income reported and verify this information matches their records. Non-residents must then use the NR4 to fulfill any tax filing requirements in their home country. Additionally, the form serves as documentation for any Canadian taxes withheld, which may be claimed as foreign tax credits in the recipient's jurisdiction.

Practical Steps

- Review the income and tax withheld amounts for accuracy.

- Use the details for tax reporting in your country of residence.

- Keep the form as proof of income and taxes paid in Canada.

Steps to Complete the NR4 Statement of Amounts Paid to Non-Residents of Canada

Completing the NR4 form involves careful attention to detail to ensure all required information is accurately reported. Follow these general steps:

- Identify the Payer and Recipient: Include correct names and addresses for both parties.

- Enter Income Details: Specify amounts paid or credited in Canadian dollars.

- Withholding Tax: Report any withholding tax amounts.

- Income Code: Use appropriate codes from the CRA guide to specify the income type.

- Year of Payment: Indicate the calendar year in which payments were made.

Comprehensive Tips

- Double-check the entries for common errors like incorrect amounts or missing signatures.

- Ensure compliance with CRA codes and requirements specific to income types.

Key Elements of the NR4 Statement of Amounts Paid to Non-Residents of Canada

Understanding the key elements ensures an accurate and compliant submission:

- Income Code: Categorizes the income type (e.g., dividends or royalties).

- Recipient Code: Denotes non-residency status.

- Currency Details: Confirm all amounts are in Canadian currency.

- Protected "B" Information: Ensure sensitive data is handled securely.

Detailed Breakdown

- Income Type: Use the CRA’s code list.

- Calculations: Double-check calculations for accuracy, particularly the withholding tax.

Who Issues the NR4 Form

The NR4 form is typically issued by Canadian payers obligated to report income paid or credited to non-residents. This includes businesses, financial institutions, and government entities. The responsibility lies with the payer to both issue the form to the recipient and submit it to the CRA.

Critical Issuer Responsibilities

- Prepare and file the NR4 accurately and on time.

- Provide copies to both the CRA and the non-resident recipient.

Filing Deadlines / Important Dates

Compliance with deadlines is crucial to avoid penalties. The NR4 form must be filed with the CRA and furnished to the non-resident recipient by the last day of March in the year following the payment.

Deadline Highlights

- Filing Due Date: March 31

- Late Filing Impact: Potential interest charges and penalties

Required Documents

To complete the NR4, gather all relevant documentation, including:

- Payment Records: Verify income paid and tax withheld.

- Residency Proof: Clarify non-resident status.

- Tax Identification: Both Canadian and foreign identifiers.

Documentation Tips

- Retain proof of all submitted forms for record-keeping.

- Confirm identifiers (e.g., SIN or Social Security Number) are correct.

Penalties for Non-Compliance

Failing to comply with NR4 filing requirements can result in severe penalties. Non-compliance includes late filings, inaccuracies, or failure to issue statements. The CRA imposes fines based on the number of failures and the duration of non-compliance.

Penalty Scenarios

- Late Filing: Fees per day until compliant.

- Accuracy Fines: Charges for each inaccuracy or missing form.