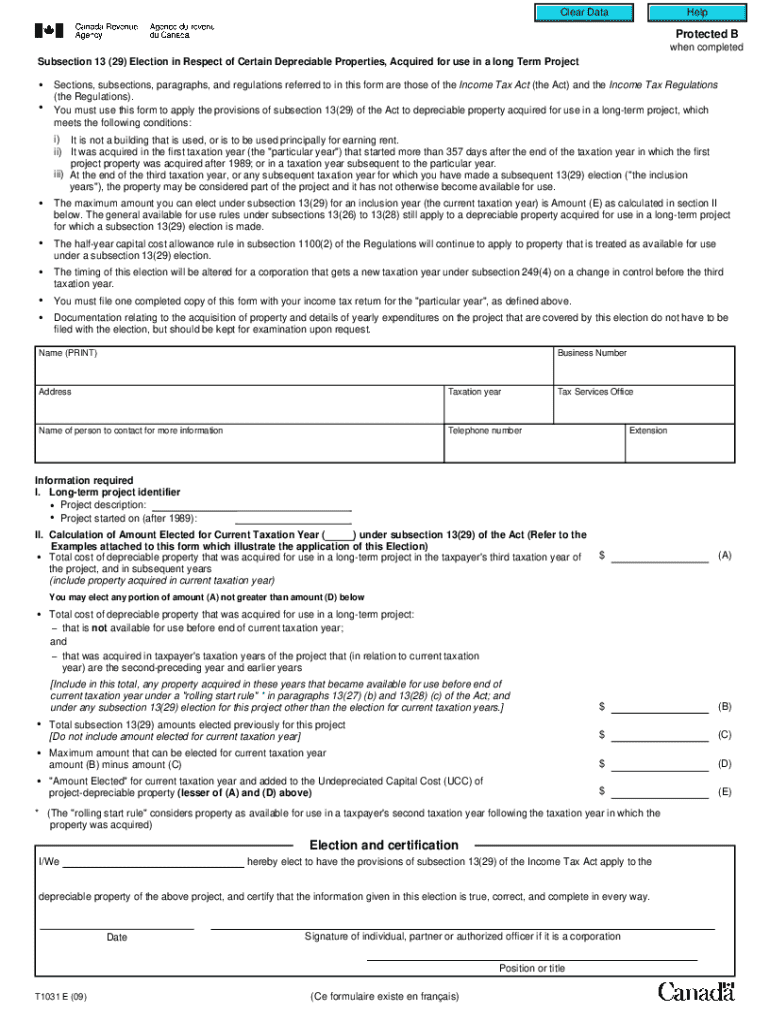

Definition and Meaning of Canada Subsection 13(29) Election Form

The Canada Subsection 13(29) Election Form, often referred to as the 13(29) Election, is a specific tax-related document used under Canadian tax law. This form is relevant for taxpayers involved in long-term projects where certain depreciable properties have been acquired. Under subsection 13(29), taxpayers can elect to apply distinct tax treatment to these properties. This results in specific depreciation allowances, impacting taxable income calculations and potentially offering tax advantages for the entities that qualify.

How to Use the Canada Subsection 13(29) Election Form

Using this form requires understanding its specific application within your tax scenario. The form is used to notify tax authorities of your election under subsection 13(29) for particular depreciable properties in long-term projects. It fundamentally outlines which assets are affected and specifies the depreciation methods applied. Entities eligible for using this form must ensure that all necessary fields, such as project details, type of property, and fiscal periods, are accurately filled out to reflect compliance with tax guidelines.

Practical Examples

- Construction Company: A construction firm working on a multi-year infrastructure project may use the form to declare specific machinery acquired for the project.

- Manufacturing: A manufacturer setting up new long-term production lines can detail the capital equipment on this form for optimized depreciation.

Steps to Complete the Canada Subsection 13(29) Election Form

- Gather Necessary Information: Compile detailed records of all depreciable properties intended for inclusion under the election.

- Identify Eligible Properties: Only assets meeting the criteria set under subsection 13(29) should be listed.

- Document Asset Details: Provide specifics about each asset, including acquisition date, cost, and intended use.

- Determine Depreciation Method: Choose and apply the appropriate depreciation method that aligns with tax regulations and project requirements.

- Complete Form Fields Accurately: Ensure that every section of the form is filled out without errors to avoid compliance issues.

- Submit to Tax Authorities: File the form within stipulated deadlines to benefit from the election.

Why Should You Use the Canada Subsection 13(29) Election Form

Utilizing this form can lead to significant tax savings and better cash flow management for eligible businesses. By electing to apply extended depreciation periods to certain assets, businesses can optimize their taxable income over time. This can be especially beneficial for projects with significant upfront capital expenditures, providing a financial cushioning effect.

Key Elements of the Canada Subsection 13(29) Election Form

- Depreciable Property List: Enumerates all assets affected by the election.

- Project Description: Highlights the nature and duration of the long-term project.

- Depreciation Strategy: Details the specific methods used for tax reporting purposes.

- Fiscal Period Information: Includes start and end dates of the fiscal periods implicated in the election.

Penalties for Non-Compliance

Failure to properly complete or submit the 13(29) Election Form can result in penalties. Non-compliance might include incorrect asset listings, failure to adhere to time frames, or misapplication of depreciation methods. Penalties may consist of fines or the loss of potential tax benefits associated with the election.

Legal Use of the Canada Subsection 13(29) Election Form

The form must be used in accordance with Canadian tax laws, ensuring that all information provided is truthful and accurate. Entities must maintain detailed records as proof of compliance for a minimum period as defined by the tax authorities to back up the election should any audit occur.

Examples of Using the Canada Subsection 13(29) Election Form

- Real Estate Development: Developers can elect particular fixtures as depreciable within their new building projects, spreading costs over time.

- Agriculture: Farm operators engaging in large-scale equipment upgrades might choose to file this election to manage depreciation better.

Scenarios

- Multi-year Mining Projects: Utilize the form for heavy machinery, aligning assets' amortization with project duration.

- Technological Expansion: Tech companies installing infrastructure for a new generation of services may find this form advantageous to manage asset depreciation over the useful life of the project.