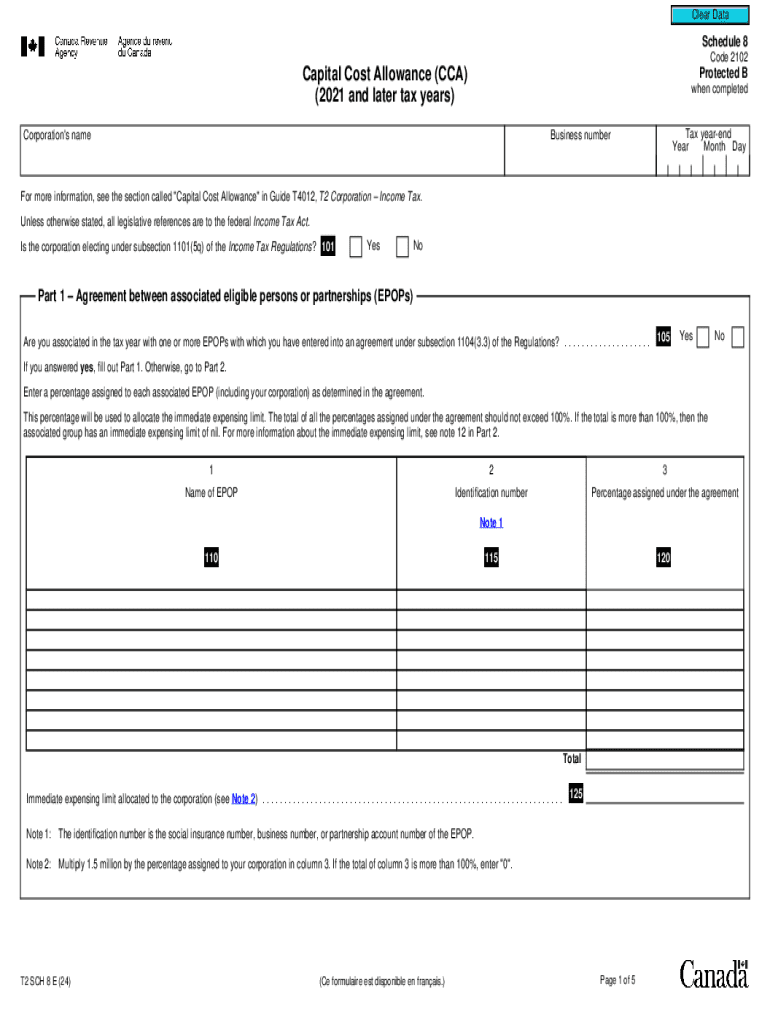

Definition & Meaning

The Schedule 8 Capital Cost Allowance Form is primarily used by businesses and individuals in the United States to claim capital cost allowances. Capital cost allowance (CCA) allows for the depreciation of property that a company or individual uses for business purposes, providing a method to write off the capital cost of a depreciable asset over time. This process is aligned with tax regulations to ensure that tangible asset depreciation is accurately accounted for within U.S. tax filings.

Key Concepts

- Depreciable Property: Assets like machinery, vehicles, equipment, and buildings used in the business context are considered depreciable property. The form allows for these assets' cost to be deducted over their useful life.

- Tax Write-off: By using Schedule 8, taxpayers can systematically spread out deductions over several years, reducing taxable income.

Examples

- A construction company using heavy machinery will utilize Schedule 8 to calculate annual depreciation and lower taxable income.

- A small firm that buys new office furniture may use this form to claim a portion of its cost each year over the asset's life span.

How to Use the Schedule 8 Capital Cost Allowance Form

Filing the Schedule 8 form involves several steps to accurately report depreciation for tax purposes.

Step-by-Step Process

- Identify Assets: List all assets acquired for business use during the tax year that qualify for depreciation.

- Determine the Class of Assets: Assets are divided into classes, each with a specified rate of depreciation. The IRS provides guidelines for these classes.

- Calculate Depreciation: Use the set depreciation rate to calculate the depreciation expense for the tax year.

- Complete the Form: Enter the necessary information, ensuring all calculations follow IRS guidelines.

- Submit with Tax Filing: The completed Schedule 8 form must be submitted along with your annual tax return.

Common Pitfalls

- Overvaluing Assets: Misclassifying an asset or overvaluing it can lead to incorrect depreciation calculations.

- Missing Deadlines: Ensure timely submission to avoid penalties.

Steps to Complete the Schedule 8 Capital Cost Allowance Form

Completing the form requires attention to detail and adherence to IRS instructions.

Detailed Instructions

- Gather Documentation: Collect purchase receipts, asset descriptions, and any previous depreciation details.

- Assign Asset Classification: Refer to IRS publications to ensure correct classification.

- Enter Asset Details: On the form, fill out each asset's purchase cost and date.

- Apply Depreciation Rate: Calculate the annual depreciation for each asset.

- Review for Accuracy: Check all entries for computational and clerical errors.

- Attach to Main Return: Include the form with your tax return.

Practical Tips

- Use Software Tools: Tax preparation software can simplify calculations and reduce errors.

- Consult with Professionals: In case of complex situations, discussing with a tax professional can be beneficial.

Who Typically Uses the Schedule 8 Capital Cost Allowance Form

The form is commonly used by various entities that need to account for the depreciation of business assets.

Key Users

- Business Owners: Small businesses, corporations, partnerships, and self-employed individuals frequently use Schedule 8.

- Tax Preparers: Professionals handling complex asset portfolios find this form essential.

- Accountants: Ensuring that business clients properly account for asset depreciation is crucial for compliance.

Important Terms Related to Schedule 8 Capital Cost Allowance Form

Understanding key terms is vital for correctly utilizing the form.

Essential Terminology

- Depreciable Property: Tangible assets with a determinable useful life.

- Depreciation Basis: Starting value used to compute depreciation, usually the original cost minus salvage value.

- Accumulated Depreciation: Total depreciation expense charged against an asset over time.

Contextual Examples

- Understanding whether an asset is a “depreciable property” aids in determining its eligibility for the capital cost allowance.

- "Depreciation Basis" affects how much expense can be allocated annually, influencing financial planning.

IRS Guidelines

Following IRS guidelines ensures that depreciation claims align with legal tax deductions.

Notable Points

- Publication Reference: IRS Publication 946 provides detailed instructions on asset depreciation.

- Methodology Options: Different methods of depreciation—such as straight line or declining balance—can be applied depending on the asset class.

Examples in Practice

- Opting for the declining balance method maximizes deductions in the early years of an asset's life.

- Cross-referencing the relevant IRS publications guarantees that depreciation methods follow current regulations.

Filing Deadlines / Important Dates

Being aware of deadlines is crucial to avoid penalties and ensure compliance.

Key Dates

- Annual Tax Filing Deadline: Typically due April 15; ensure Schedule 8 is prepared in time.

- Asset Purchase Deadlines: Assets acquired after December 31 of the tax year cannot be depreciated that year.

Strategies to Avoid Missed Deadlines

- Implement Calendar Alerts: Use electronic reminders for critical tax-related deadlines.

- Early Preparation: Begin organizing documents and calculating depreciation well before tax season.

Required Documents

Accurate reporting requires assembling the right documentation.

Necessary Documents

- Purchase Invoices: Proof of asset purchase costs.

- Depreciation Schedules: Past schedules showing previous years' depreciation.

- Property Records: Details of asset types and their classifications.

Document Management Tips

Organizing and maintaining documents digitally can streamline the filing process and ensure easy retrieval.