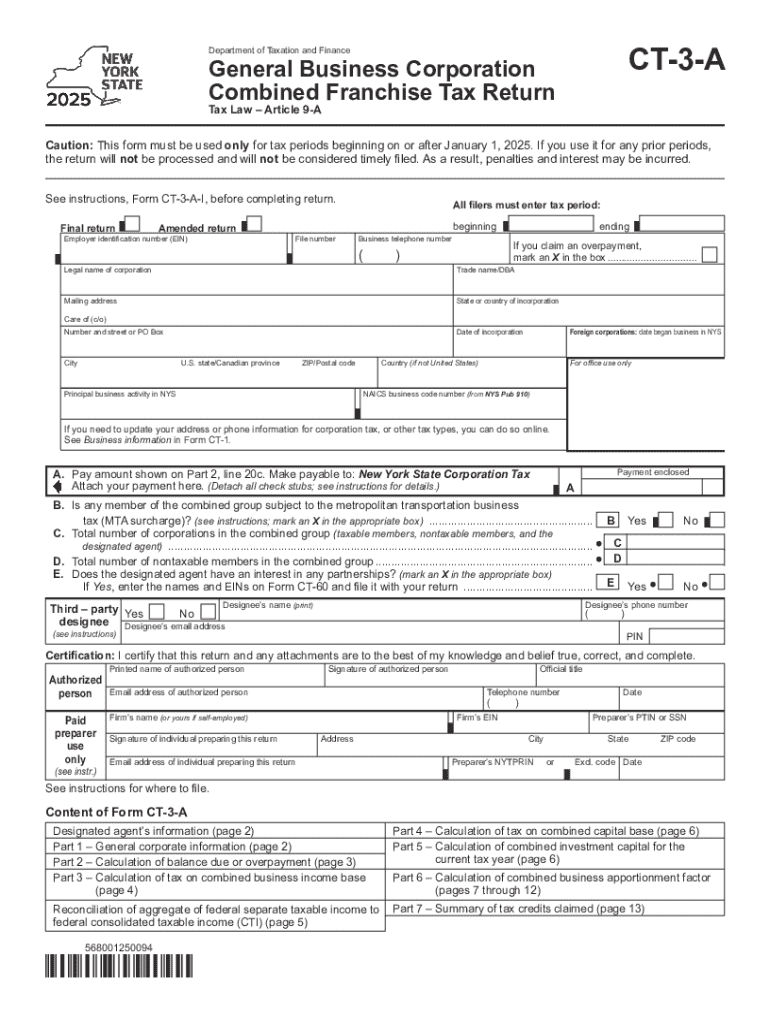

Definition & Meaning of the New York State CT-3-A Combined Franchise Tax Return

The New York State CT-3-A Combined Franchise Tax Return is a tax form used by certain corporations operating in New York State. It is designed for business corporations that are part of a combined group, meaning they are owned or controlled by other businesses that also operate in New York. This form allows these corporations to report and pay their franchise tax as a group, instead of individually. The franchise tax is essentially a fee charged to corporations for the privilege of doing business in New York and is calculated based on various factors such as capital, income, and employee payroll within the state.

Corporations required to file this form generally are those with complex business structures and significant presence in New York. Filing the CT-3-A ensures compliance with New York’s tax regulations, facilitating proper revenue collection for the state.

How to Use the New York State CT-3-A Combined Franchise Tax Return

When using the CT-3-A form, businesses must compile financial data from all constituent members of their corporate group. Details on each company's assets, liabilities, income, and deductions should be prepared in advance for accurate reporting. The form requires a breakdown of combined group activities, adjustments, and allocations among affiliated companies.

To accurately complete the CT-3-A, businesses should:

- Gather comprehensive financial records.

- Ensure all subsidiaries are accounted for in the combined return.

- Use the provided instructions to calculate the appropriate tax due.

- Check compliance with specific New York State tax laws that may affect calculations.

Filing accurately can ensure fair valuation of liabilities and prevent discrepancies that could lead to audits or penalties.

Steps to Complete the New York State CT-3-A Combined Franchise Tax Return

-

Assemble Financial Documentation: Collect year-end financial statements, prior tax returns, and details on each company’s New York receipts, property, and payroll.

-

Identify Combined Group Members: List all affiliated corporations involved in the combined return, ensuring no omissions.

-

Calculate Allocated Income: Use the form’s instructions to compute allocated and apportioned income among group members.

-

Complete Required Schedules: Certain schedules like the income and capital tax bases, and the tax due or refund, require separate calculations.

-

Finalize Tax Liability or Refund: Sum up total tax liabilities, considering any credits applicable to the group.

-

Review & Sign: Double-check calculations for accuracy and compliance. The form must be signed by an authorized officer.

Required Documents for the New York State CT-3-A Combined Franchise Tax Return

To successfully complete the form, the following documents are typically required:

- Official financial statements for the taxable year.

- Prior year's tax returns to verify any carry-forwards or credits.

- Current and previous year’s payroll and property records.

- Documentation that confirms the relationship between the corporations in the combined group.

Having these documents at hand ensures accuracy and efficiency during the filing process.

Who Typically Uses the New York State CT-3-A Combined Franchise Tax Return

The CT-3-A form is specifically used by corporations that are part of a combined group under common ownership or control. This includes, but is not limited to:

- Holding companies with operational subsidiaries in New York.

- Multinational corporations with branches in numerous locations including New York.

- Franchise groups with multiple corporations reporting collective income.

These users must navigate the complexities of combined reporting to align with state requirements and optimize their tax obligations.

Key Elements of the New York State CT-3-A Combined Franchise Tax Return

- Combined Group Reporting: The form captures comprehensive financial activity across corporations in the group.

- Apportionment Details: Ensures income and activities are correctly distributed for New York State tax purposes.

- Tax Computation Schedules: Sections include calculations for tax bases and possible credits.

Understanding each component is vital for meeting accuracy standards and adhering to state tax legislation.

Legal Use of the New York State CT-3-A Combined Franchise Tax Return

Filing this form is legally mandated for qualifying corporations within New York. Non-compliance or incorrect filing can result in significant penalties, interest on unpaid taxes, or worse, legal proceedings. The form aligns with New York State Tax Law, which requires transparent reporting of corporate income and business activities within the state. Businesses should maintain meticulous records and consult tax professionals to avert legal challenges and optimize tax strategy.

Penalties for Non-Compliance

Corporations failing to file, underreporting income, or misreporting combined activities on the CT-3-A may face:

- Financial penalties that increase with the duration of non-compliance.

- Accrued interest on unpaid taxes.

- Audits from the New York State Department of Taxation and Finance leading to further adjustments and penalties.

Avoiding these penalties involves consistent accuracy and adherence to filing deadlines, supported by detailed, well-organized tax records.