Definition and Meaning

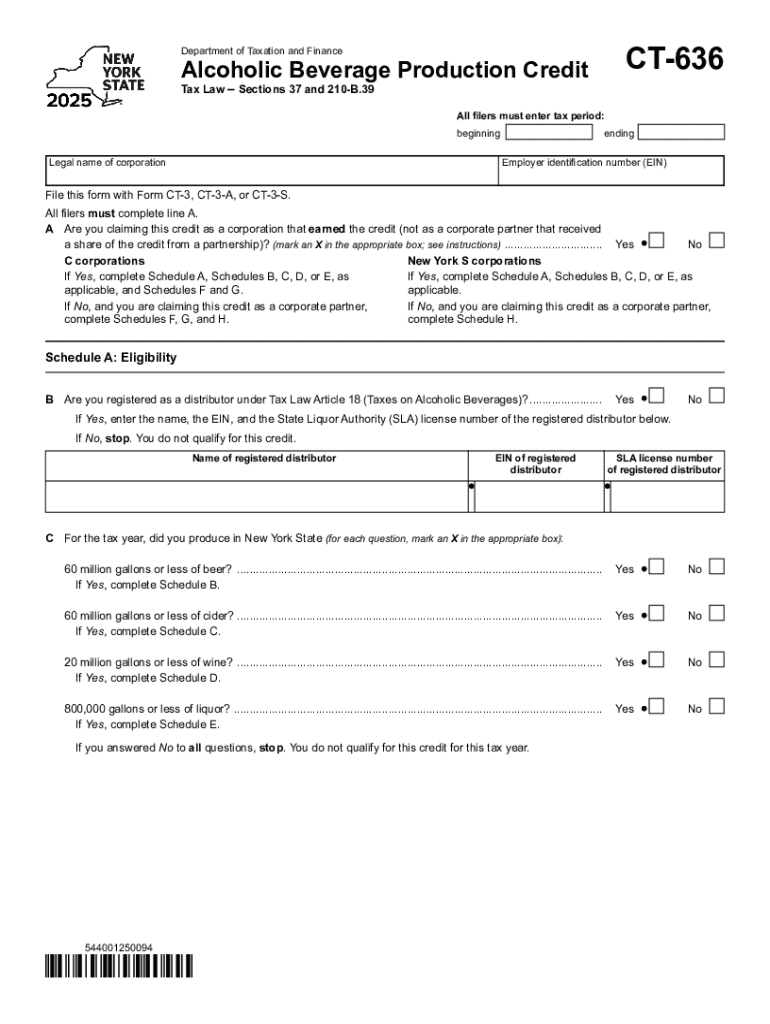

The Form CT-636 Alcoholic Beverage Production Credit Tax is designed to provide tax credits to businesses engaged in producing alcoholic beverages in the United States. This form is applicable under Sections 37 and 210B.39 of the Tax Law, and it is aimed at encouraging local production by offsetting certain production costs. Businesses can claim this credit by completing specific sections of the form that detail the eligible production activities and expenses.

Important Terms Related to the Form

- Tax Credit: A reduction of the income tax amount a corporation owes.

- Production Costs: Expenses directly associated with the manufacturing of alcoholic beverages, such as materials and labor.

- Tax Law Sections 37 and 210B.39: Legislative frameworks under which the CT-636 is governed, defining eligibility and applicable credits.

Eligibility Criteria

Businesses must meet specific requirements to qualify for the Form CT-636 Alcoholic Beverage Production Credit Tax. Typically, entities engaged in the manufacturing, refining, or bottling of alcoholic beverages are eligible. This includes:

- Corporations registered under the applicable state laws.

- Businesses that can demonstrate production within the tax period for which the credit is claimed.

Business Types That Benefit Most

- Microbreweries and Craft Distillers: Smaller entities gain significant benefits as the credit helps mitigate high initial production costs.

- Large-scale Producers: While smaller per-unit savings are involved, these can accumulate to substantial sums given higher production volumes.

Steps to Complete the Form CT-636

- Identify the Applicable Tax Period: Clearly state the beginning and ending dates of the tax period for which the credit is claimed.

- Fill Out the Contact Information: Enter the legal name of the corporation and the employer identification number.

- Calculate Production Costs: Aggregate all eligible production expenses occurred during the tax period.

- Compute the Credit: Use the defined percentages in the tax law sections to calculate the allowable credit.

- Attach Supporting Documentation: Include invoices, receipts, or other proof of production expenses, ensuring all filed documents are in compliance.

How to Use the Form

To maximize the benefit from the Form CT-636 Alcoholic Beverage Production Credit Tax, businesses should keep accurate financial records throughout the tax year. Utilize accounting software compatible with tax forms to streamline the calculation and submission process. Understand allowable expenses fully and consult with tax professionals if needed to avoid errors that could delay approval.

Software Compatibility

The use of software like QuickBooks or TurboTax can facilitate accurate and efficient filing. These platforms often offer updates or plugins that specifically cater to state tax forms, including necessary fields for CT-636 data entry.

Important Deadlines and Filing Methods

Filing Deadlines

- Annual Filing: Typically coincides with the traditional corporate tax deadline; however, it is crucial to check state-specific due dates.

Form Submission Methods

- Online: Through designated state tax department portals.

- Mail: Submission via mail should be tracked to ensure receipt by the state authorities.

- In-Person: May be available depending on local state regulations; often less favored due to time delays.

Penalties for Non-Compliance

Failure to file or inaccurately filing the Form CT-636 may result in penalties, including fines and interest on unpaid taxes. Businesses must ensure that all documentation is correct and submitted on time. Repeated or deliberate non-compliance can trigger audits or more severe financial repercussions.

State-Specific Rules

While the federal framework guides Form CT-636, states may impose additional requirements or variations in credit percentages and eligible costs. For instance, some states may offer additional credits for eco-friendly production practices. Businesses should verify state-specific regulations to ensure compliance and maximize benefits.

Who Issues the Form

The form is typically issued by the state's Department of Taxation and Finance. It is essential to use the most current version of the form to ensure compliance with updated tax laws. State tax departments provide access to forms, guidance, and updates regarding any changes to the credit program or applicable tax laws.

Key Takeaways

- Always use the most recent version of Form CT-636.

- Maintain detailed records of all eligible production expenses.

- Understand both federal and state-specific rules to optimize credit claims.

- Consider using software to simplify the calculation and filing process.

These details form a comprehensive guide to understanding, completing, and utilizing the Form CT-636 Alcoholic Beverage Production Credit Tax effectively.