Definition & Meaning

The Claim for Credit for Employment of Persons with Disabilities is a tax incentive provided by the Internal Revenue Service (IRS) to encourage businesses to hire individuals with disabilities. This credit aims to support the integration of disabled persons into the workforce by offsetting a portion of the costs employers incur when hiring them. By reducing tax liabilities, the credit provides financial relief to businesses, encouraging them to offer employment opportunities to a wider, more inclusive range of candidates.

Core Objectives

- Promote workforce diversity by encouraging the hiring of disabled individuals.

- Support businesses economically by reducing tax burdens.

- Foster an inclusive working environment that adheres to federal employment standards.

Significance

Integrating disabled individuals into the workforce not only supports them financially but also enriches the workplace culture with diverse perspectives and skills.

Who Typically Uses the Claim for Credit

Businesses across various sectors are eligible to use this credit, particularly those committed to inclusive hiring practices. While any employer hiring individuals with disabilities might qualify, there are specific types of organizations that often utilize this form:

- Small to medium enterprises (SMEs) looking to broaden their recruitment strategies while managing costs.

- Non-profit organizations dedicated to social inclusion and community development.

Common User Profiles

- Retailers: Often hiring diverse staff to reflect a broad customer base and community values.

- Service Industries: Including hospitality and healthcare sectors that focus on comprehensive care and support.

- Manufacturing and Production: Industries where diverse capabilities among staff can drive innovation and efficiency.

Eligibility Criteria

To claim this credit, employers need to meet specific criteria set forth by the IRS:

- Employment Status: The employee must be a new hire, classified as a person with a disability under the guidelines provided by the Americans with Disabilities Act (ADA).

- Verification: Employers must keep records or certifications attesting to the employee's disability status if required.

- Duration of Employment: The individual must have been employed during the tax year for which the credit is being claimed.

Covered Disabilities

- Physical impairments that substantially limit one or more major life activities.

- Mental health conditions recognized under the ADA.

- Other conditions as defined by IRS guidelines and federal law.

How to Obtain the Claim Form

Employers interested in this credit can acquire the necessary form through these methods:

Online Access

- Access the IRS website for downloadable forms and instructions.

- Utilize tax software platforms like TurboTax or QuickBooks that incorporate these forms during tax preparation processes.

Physical Copies

Employers can request paper forms from IRS offices or professional tax services, where these are available for public use.

Steps to Complete the Claim for Credit

Following the correct procedural steps ensures accurate and timely submission:

- Collection of Employee Documentation: Gather necessary documentation that proves the eligibility of the employed person with a disability.

- Form Download and Preparation: Obtain the official form from the IRS, ensuring you have the latest version.

- Accurate Information Entry: Detail information about the business and qualifying employee within the form fields.

- Review and Verification: Double-check all entered data for accuracy, validating against employee records and tax documentation.

- Submission: Submit the finished claim form with your annual tax return to ensure proper credit application.

Common Mistakes

- Incomplete employee documentation can hinder processing.

- Misreporting of employee eligibility or business identity leading to denials.

State-Specific Rules for the Claim

While the credit is federally regulated, some states may have additional rules or benefits:

- California: Offers additional credits for in-state businesses hiring disabled workers, enhancing federal benefits.

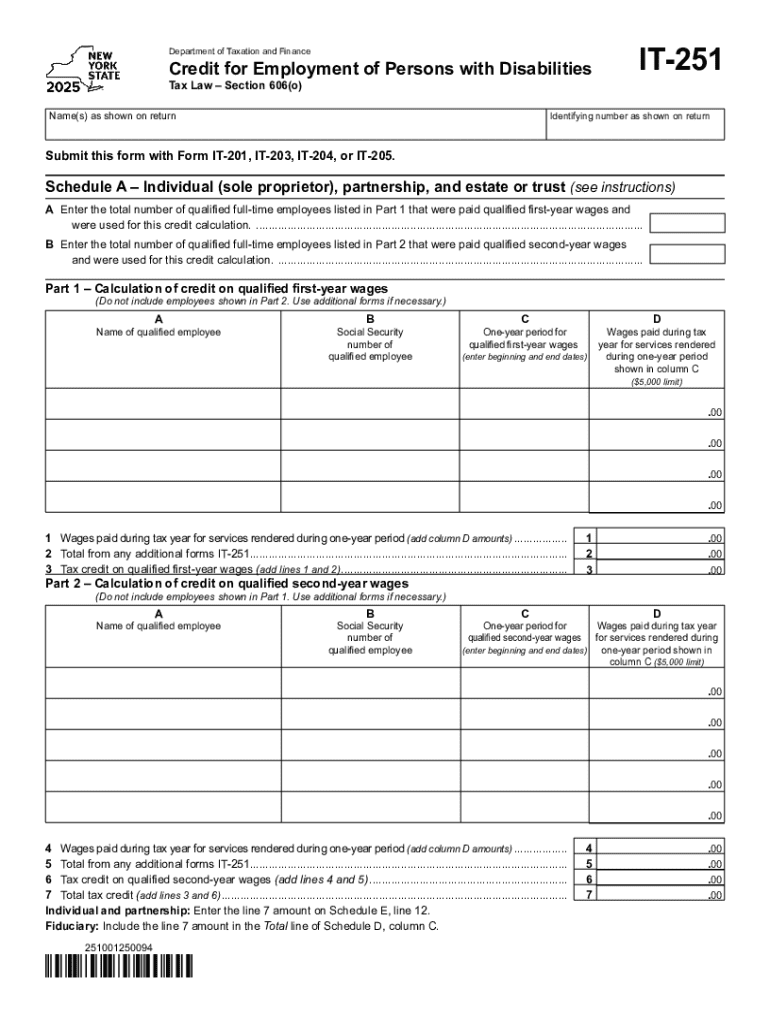

- New York: Provides state-specific forms that must be submitted alongside the federal claim.

Compliance and Differences

- Each state may define disability criteria slightly differently, reflecting local employment laws.

- Certain states may require separate or additional documentation to prove eligibility.

Key Elements of the Claim Form

Understanding each section of the form is critical for correct completion:

- Business Information: Includes company name, tax identification number, and contact information.

- Employee Details: Requires detailed information about the hired individual, including disability certification.

- Credit Calculation: Sections where the employer calculates the potential credit based on qualifying wages paid.

Supporting Sections

- Certification Statement: Signing party certifies that the information provided is accurate and complete.

- Reviewer Comments: Spaces for IRS use during review.

Legal Use of the Credit

The credit must be used in compliance with federal and state tax laws, ensuring that all claims are legitimate and verifiable:

- Documentation Retention: Employers must keep employee and tax records for a specified period to validate credits if audited by the IRS.

- Tax Compliance: Improper use of credits could result in penalties, including tax audits and fines.

Consequences of Misuse

- Revocation of claimed credits.

- Potential penalties or legal action under federal law.

Employers must stay informed of any changes to IRS regulations or eligibility criteria that might affect future claims.