Definition & Meaning

Instructions for Form IT-2658-E, known as the New York State Form IT-2658-E, is specifically designed for nonresident individuals who are involved in partnerships, limited liability companies (LLCs), and S corporations operating within New York State. This form outlines the estimated personal income tax requirements and details the process by which individuals should report their tax liabilities tied to their specific business activities. Understanding the meaning of this form involves recognizing its unique role in facilitating compliance with New York State's tax laws for nonresident individuals.

Importance of Understanding the Form

- It ensures compliance with New York State tax obligations.

- It helps in accurately determining the estimated personal income tax liabilities.

- It aids in avoiding penalties associated with underpayment of taxes.

Key Elements of the Instructions for Form IT-2658-E

The form contains several critical sections that guide users through the process of determining and reporting their estimated tax liabilities. The key elements include:

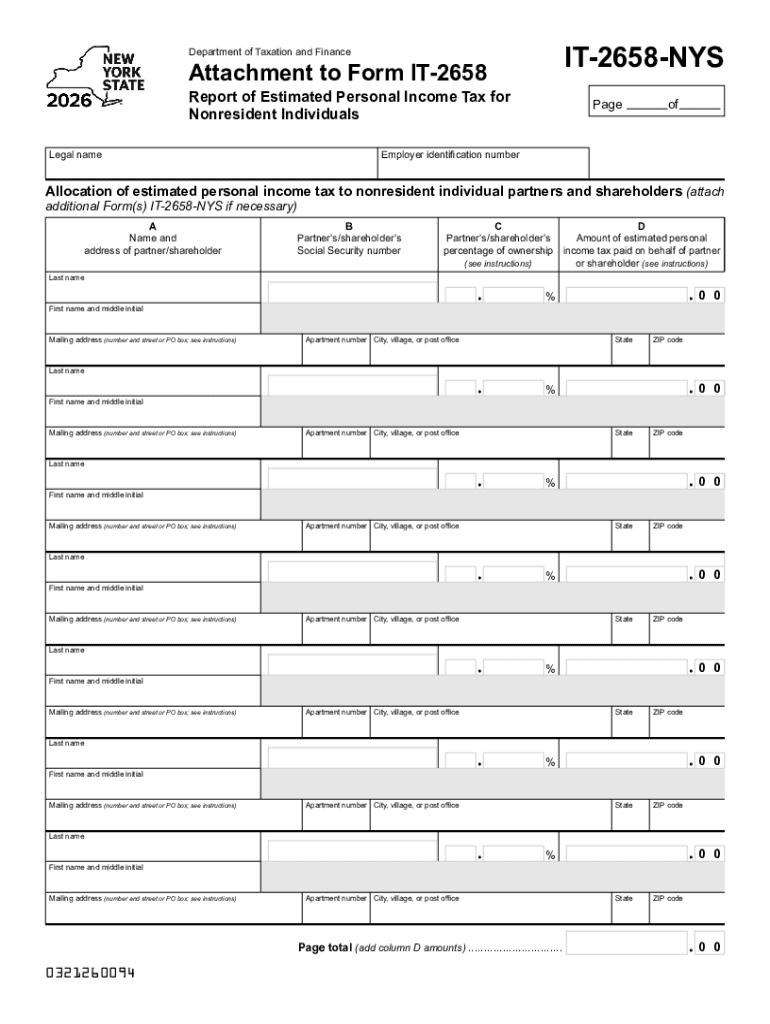

- Identification Section: This part requires users to input their legal name, address, and Employer Identification Number (EIN). Accurate entry of this information is essential to ensure correct processing.

- Allocation of Income: Users must provide details of income allocation to accurately calculate the portion of their income subject to New York State tax.

- Estimated Tax Worksheet: This section includes a step-by-step worksheet that helps in computing the estimated taxes based on various income sources and deductions.

Steps to Complete the Instructions for Form IT-2658-E - Tax NY

- Gather Required Documents: Before beginning, collect all relevant financial documents, including previous tax returns and income statements, which will aid in accurately completing the form.

- Fill Out the Identification Section: Enter your legal name, address, and EIN in the designated fields. Ensure this information matches official records.

- Calculate Income Allocation: Use the provided guidelines to allocate income that is subject to New York State taxation.

- Estimate Your Tax Liability: Use the Estimated Tax Worksheet section to calculate your estimated tax due. This involves applying the appropriate rates to your allocated income.

- Review and Sign: Double-check all entries for accuracy, then sign and date the form before submission.

Common Pitfalls to Avoid

- Failing to accurately allocate income based on New York State guidelines.

- Overlooking the importance of the Estimated Tax Worksheet.

- Missing deadlines, which could lead to penalties.

Important Terms Related to Instructions for Form IT-2658-E - Tax NY

Understanding the terminology used within the form is crucial for accurate completion. Some important terms include:

- Nonresident: An individual who does not reside in New York State but earns income from New York sources.

- Allocation: The process of determining the amount of income subject to state tax.

- Estimated Tax: The projected amount of tax payable based on income forecasts for the year.

Examples in Context

- A nonresident investor in an LLC must allocate their share of the business's income to New York and compute the tax owed.

- Estimated tax payments are based on projections and must be adjusted if there are changes in income levels throughout the year.

Who Typically Uses the Instructions for Form IT-2658-E - Tax NY

These instructions are mainly utilized by nonresident individuals who have a financial stake in New York-based partnerships or S corporations, requiring them to report and pay estimated taxes to the state. Common users include:

- Partners in LLCs: Those involved in multi-state business entities who need to allocate New York income.

- Shareholders in S Corporations: Individuals holding shares in corporations operating across state lines.

- Estate Beneficiaries: Beneficiaries of estates that earn income from New York-based operations.

Filing Deadlines / Important Dates

Adhering to the filing deadlines is critical to avoid penalties and interest charges. The primary deadlines are:

- Quarterly Payments: Estimated tax payments are typically due on April 15, June 15, September 15, and January 15 of the following year.

- Annual Reconciliation: Final reconciliation of estimated taxes should be done when filing the annual state tax return.

Late Filing Penalties

- Underpayment of Estimated Tax: Can result in interest charges on overdue taxes.

- Failure to File: May incur penalties, emphasizing the importance of adhering to deadlines.

Form Submission Methods (Online / Mail / In-Person)

Nonresident taxpayers have various options for submitting Form IT-2658-E:

- Online Submission: Fast and convenient, often preferred by taxpayers who prefer digital processes and require immediate confirmation.

- Mail: Traditional option for those who favor paper filings.

- In-Person at NY Tax Office: Possible for those who wish to submit in person due to unique circumstances.

Guidelines for Each Method

- Online: Ensure digital documents are correctly formatted and submitted through the official New York State Department of Taxation and Finance portal.

- Mail: Use certified mail to ensure tracking and confirmation of receipt.

- In-Person: Schedule an appointment to ensure your visit is efficient and solution-focused.

Penalties for Non-Compliance

Non-compliance with the Form IT-2658-E requirements can lead to several repercussions, such as:

- Monetary Penalties: Typically arise from underpayments or failure to meet deadlines.

- Interest Charges: Calculated on unpaid tax balance, encouraging timely payment.

- Legal Ramifications: Persistent non-compliance can result in more serious legal proceedings.

Avoidance Strategies

- Maintain accurate records of all income and deductions.

- Set reminders for filing deadlines.

- Regularly review estimated tax calculations to avoid discrepancies.

State-Specific Rules for the Instructions for Form IT-2658-E - Tax NY

Each state may have unique rules applicable to nonresident taxation. For New York:

- Allocation of Income: Strict rules demand precise accounting of income originating within the state.

- Rate Differences: New York may apply different rates to specific income classes, affecting overall tax responsibilities.

- Local Jurisdiction Requirements: Some localities may impose additional tax obligations on nonresidents, requiring further diligence in tax preparation.

Examples of State-Specific Scenarios

- An individual with rental properties in New York must comply with state-specific income allocation rules.

- Partnerships must account for portions of income derived from New York operations, separated from other activities.

By adhering to the comprehensive instructions provided above, you can effectively manage your New York State tax obligations as a nonresident taxpayer, ensuring thorough and accurate reporting.