Definition & Meaning

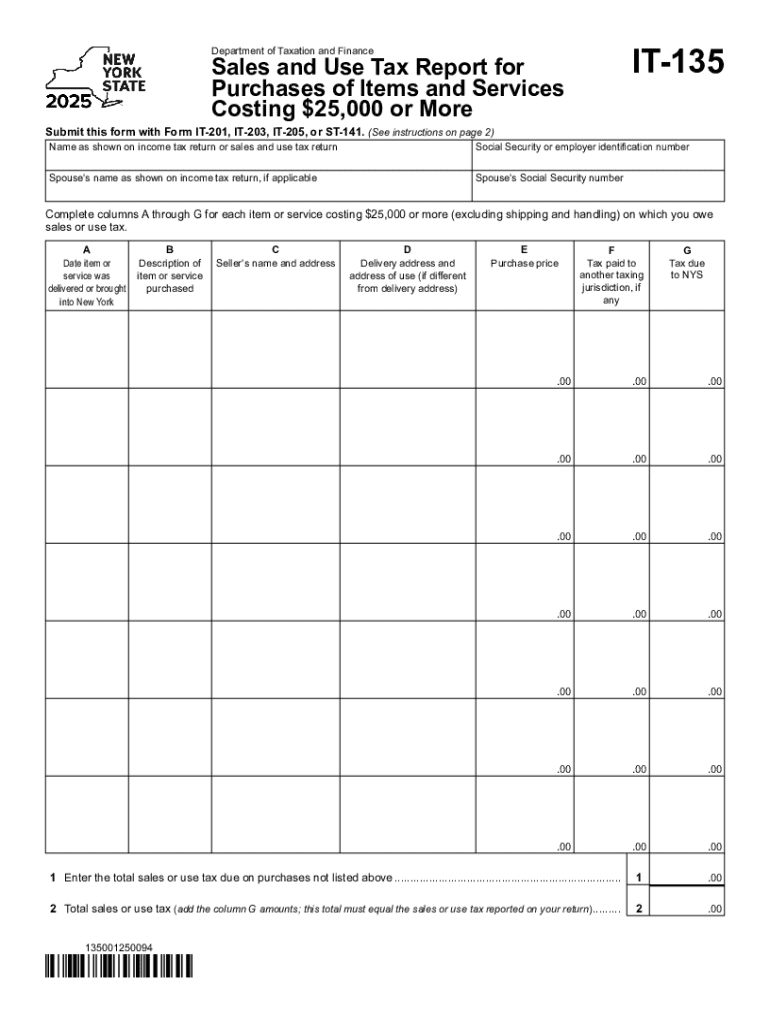

The New York Sales and Use Tax Report IT-135 is a specific form that taxpayers in New York must utilize to report purchases of items and services costing $25,000 or more. This document is essential for ensuring compliance with tax regulations and is typically submitted alongside other forms such as IT-201, IT-203, IT-205, or ST-141. It captures information about large purchases to guarantee proper tax collection and reporting.

Steps to Complete the New York Sales and Use Tax Report IT-135

-

Gather Necessary Information: Before you start filling out Form IT-135, ensure you have all relevant information about your large purchases, including invoices, purchase receipts, and vendor details.

-

Fill Personal and Business Details: Enter your personal or business information accurately, including your name, address, and taxpayer identification number.

-

Report Purchases: Itemize each purchase over $25,000, providing specifics such as the date of acquisition, description of the item or service, and the amount paid.

-

Calculate Tax Owed: Use the purchase details to calculate the use tax owed, considering that sales taxes might have already been accounted for at the point of sale.

-

Attach Required Forms: If applicable, include supplementary forms like IT-201 or IT-203 to give additional context or detail about your purchase.

-

Review and Submit: After completing the form, carefully review it for accuracy, ensuring all necessary fields are filled. Submit it as directed by the New York Department of Taxation and Finance.

Key Elements of the New York Sales and Use Tax Report IT-135

- Purchase Information: Detailed documentation about items and services purchased, including cost, vendor information, and receipt numbers.

- Tax Calculation: A section to compute the appropriate use tax, which must reflect any applicable local tax rates.

- Supporting Documents: Additional attachments may be required, especially in cases involving complex transactions or exemptions.

Filing Deadlines / Important Dates

The New York Sales and Use Tax Report IT-135 must be filed in conjunction with your annual state tax return. Typically, the deadline aligns with the tax filing season, generally on or around April 15, but this may vary. It's essential to verify specific due dates each year as they can change based on legislative updates or calendar shifts.

Penalties for Non-Compliance

Failure to timely file the IT-135 form, or misreporting purchases, can lead to significant penalties. These may include fines, interest on unpaid taxes, and potential audits by the New York Department of Taxation and Finance. It is crucial to maintain accurate records and ensure compliance to avoid these risks.

Form Submission Methods (Online / Mail / In-Person)

-

Online Submission: Filing electronically is recommended as it offers a faster processing time and an immediate confirmation of receipt. New York State provides a secure portal for electronic submissions.

-

Mail: If you prefer, the form can be sent via traditional mail, but ensure the mailing address is current. Note that processing via mail might take longer.

-

In-Person: Although less common, in-person submission at a local tax office is an option if you require immediate assistance or confirmation of submission.

Who Typically Uses the New York Sales and Use Tax Report IT-135

This form is usually utilized by:

- Businesses: Companies making substantial capital investments or large inventory purchases often need to file this report.

- High-Value Purchasers: Individuals making significant personal purchases, such as artwork or specialized equipment, must report these expenditures.

- Non-Resident Entities: Out-of-state entities conducting taxable transactions within New York are also required to complete this form.

State-Specific Rules for the New York Sales and Use Tax Report IT-135

New York has unique regulations concerning sales and use tax reporting. For example, certain localities within the state may have specific rates or exemptions not applicable elsewhere. It's important to understand these nuances, particularly if the purchases span across multiple locations within New York.

Required Documents

To accurately complete the form, you'll need:

- Invoices and Receipts: Details of each qualifying purchase.

- Vendor Information: Names and addresses from whom significant items or services were purchased.

- Proof of Previous Tax Payments: Documentation showing sales tax already paid, if applicable.

Business Types that Benefit Most from New York Sales and Use Tax Report IT-135

Entities that are most impacted by this report include:

- Retail Businesses: Frequently purchasing large quantities of goods.

- Construction Companies: Procuring high-cost materials and equipment.

- Manufacturers: Buying parts and machinery integral for production processes.