Definition & Meaning

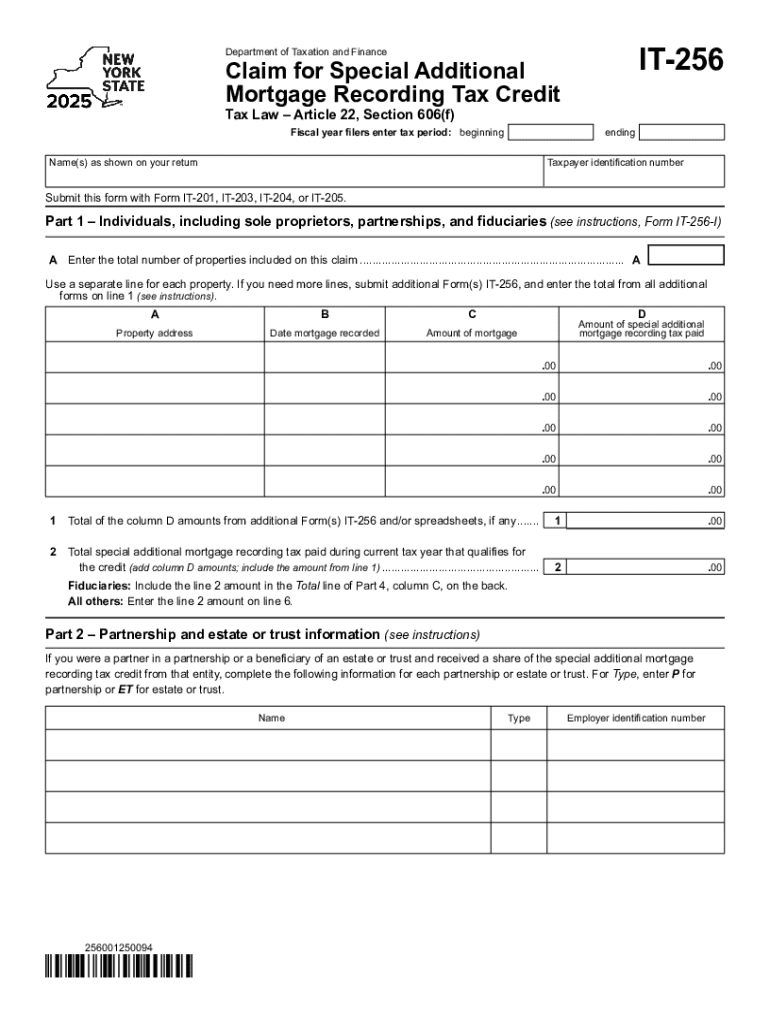

The "Form IT-256 Claim for Special Additional Mortgage Recording Tax Credit Tax Year 2025" is used by taxpayers to claim a tax credit for the special additional mortgage recording tax paid on recorded mortgages in New York. This form allows individuals and entities to offset their New York State taxes by the amount of special additional mortgage recording tax they have paid, making it an important tool for reducing tax liability.

Importance of the Form

- Helps reduce overall tax liability.

- Applicable for taxpayers who have paid the special additional mortgage recording tax in New York.

- Provides financial relief for property-related tax expenses.

How to Obtain the Form IT-256

The IT-256 form can be acquired through several avenues, such as:

- Online Download: New York Department of Taxation and Finance website allows you to download the form directly.

- Tax Preparation Software: Many tax software solutions, such as TurboTax or QuickBooks, include the form in their templates.

- Tax Professionals: Tax advisors or accountants often have the latest forms accessible for their clients.

Download Steps

- Visit the New York Department of Taxation and Finance website.

- Navigate to the forms section and search for "IT-256."

- Download and print the form for physical filing, or save it for digital submission.

Steps to Complete the Form IT-256

The completion process involves several key steps, which are critical for accurate filing and ensuring eligibility for the credit:

- Fill Out Personal Information: Include your or your entity's name as shown on your tax return, Social Security or Employer ID number, and filing status.

- Mortgage Details: Provide detailed information about the mortgage, such as property location and the date the mortgage was recorded.

- Tax Credit Calculation: Input the amount of special additional mortgage recording tax paid. Follow the instructions on the form for calculating the credit.

- Attach Required Documentation: Include proof of payment and any supporting documents that indicate the taxes paid.

- Final Review: Double-check form entries for accuracy before submission.

Key Elements of the Form IT-256

Understanding the main components of the form enhances accuracy and compliance when filing:

- Taxpayer Identification: Ensures the correct taxpayer is claiming the credit.

- Mortgage Information: Details on the recorded mortgage.

- Credit Calculation Table: A section that helps in computing the correct tax credit.

- Signature and Date: The taxpayer's declaration, affirming the information's accuracy.

Detailed Components

- Line Items: Each entry corresponds to specific taxpayer data and tax credit calculations.

- Instructions: Located with the form or as a separate booklet, providing valuable guidance.

Eligibility Criteria

To qualify for the tax credit via the IT-256 form, applicants must meet several eligibility criteria:

- Location Constraint: The property must be located in New York, where the mortgage recording tax applies.

- Tax Payment Record: Proof of the special additional mortgage recording tax paid is mandatory.

- Filing Status: Must align with the taxpayer’s state tax return information.

Situational Examples

- Homeowners: Individuals who purchased a home and recorded a mortgage in New York.

- Business Entities: Companies that own and mortgage real estate within the state.

Filing Deadlines / Important Dates

Timely submission of the IT-256 form is crucial:

- Filing Concurrently: This form should generally accompany the taxpayer's New York State income tax return.

- Annual Deadlines: Align with state tax return due dates, typically around mid-April for individual filers.

Extensions and Late Filings

- Extensions Available: Taxpayers may file for extensions if they require more time.

- Penalties: Late submission could result in penalties or loss of credit eligibility.

IRS Guidelines

Although the IT-256 is specific to New York state taxes, it needs to be correctly coordinated with IRS filings:

- Income Reporting: Ensure that any credits claimed reflect accurately on federal tax returns where relevant.

- Documentation: Maintain clear records that can substantiate claims in cases of an audit.

Additional Resources

- IRS Publications: Consult IRS guidelines on related federal deductions or credits that might interact with the state credit.

Digital vs. Paper Version

Filing can be done either through electronic or physical forms, each having its own benefits:

- Digital Submission: Provides convenience and faster processing times.

- Paper Filing: Traditional method, recommended if electronic means are unavailable.

Considerations

- Software Compatibility: Ensure that digital submission software aligns with the IT-256 format.

- Confirmation of Receipt: Important for tracking the submission and ensuring timely filing.

Balancing between comprehensive details and structured instructions, this guide aims to provide a thorough yet accessible approach to understanding and utilizing Form IT-256 effectively.