Definition & Purpose of Form 709

Form 709, known formally as the United States Gift (and Generation-Skipping Transfer) Tax Return, is a crucial document used by U.S. taxpayers to report gifts and generation-skipping transfers. This form is used to disclose to the Internal Revenue Service (IRS) the transfer of monetary or tangible assets to another person, in certain circumstances. It applies when a gift exceeds the annual exclusion limit, defined by the IRS annually, or involves a generation-skipping transfer – essentially a transfer or gift to a grandchild or someone of an equivalent generational status that may incur additional tax implications.

How to Use Form 709

Understanding how to use Form 709 effectively is essential for accurate tax reporting.

- Identify Taxable Gifts: Begin by determining which gifts are taxable. Not all gifts need to be reported—identify those exceeding the annual exclusion limit.

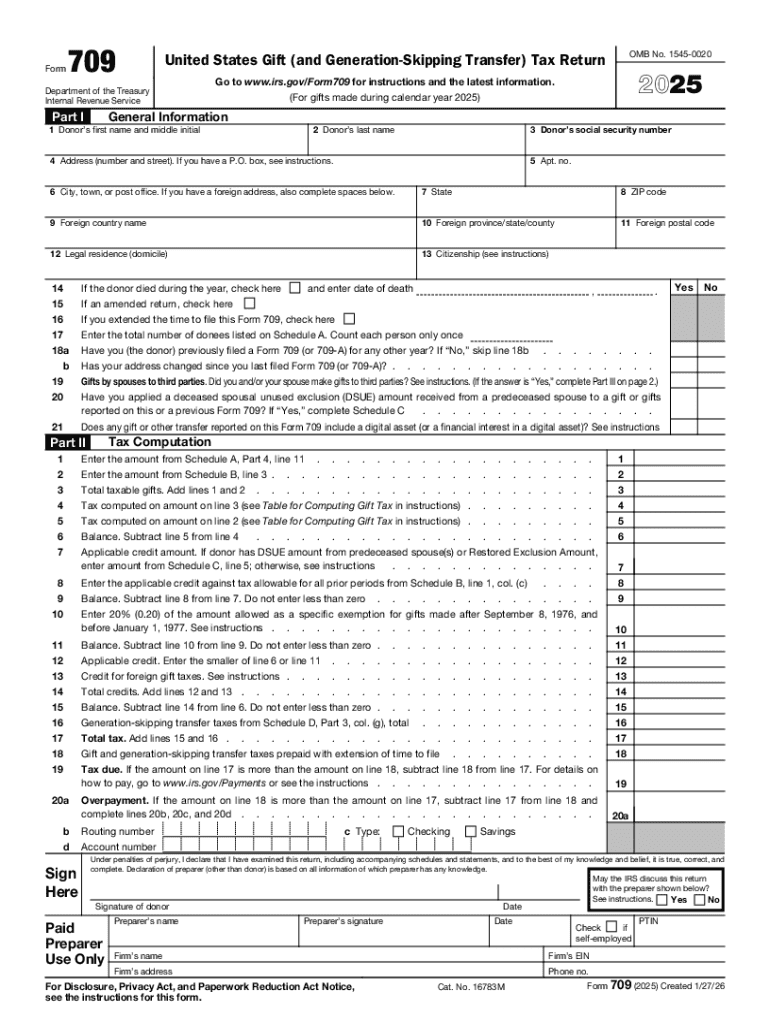

- Complete Required Sections: Ensure all required sections are completed, capturing donor and donee details, description, and fair market value of exchanged gifts.

- Report Generation-Skipping Transfers: Use Part II of Form 709 to report these types of transfers specifically.

- Calculate Gift Tax: Make use of the tax computation section to determine any tax due.

- Filing: File the form as part of your annual tax filings if required, ensuring all calculations and disclosures are accurate.

Steps to Complete Form 709

Following a detailed step-by-step procedure can enhance accuracy and compliance:

- Gather Information: Prerequisites include the donor and donee’s personal information, and details around the gift, including its fair market value.

- Fill Identification Information: Start with basic information including taxpayer identification numbers for all parties involved.

- Calculate Total Gifts: Use the worksheet to total all gifts given during the tax year.

- Apply Exclusions and Deductions: Apply any allowed exclusions, deductions, and prior year credits to offset amounts owed.

- Complete Generation-Skipping Transfer Calculations: If applicable, fill in the necessary sections for transfers that might fall into this category.

- Sign and Date: Ensure the form is signed and dated; missing this step can result in delays in processing.

- Submit Form: Submit to the IRS through acceptable formats, ensuring compliance with submission deadlines.

Who Typically Uses Form 709

Form 709 is generally used by individuals who have made substantial gifts that exceed non-taxable limits.

- High Net-Worth Individuals: Those who provide large monetary gifts or transfer significant assets often use this form to ensure compliance.

- Individuals Engaging in Estate Planning: People seeking to lower estate tax liabilities through gifting strategies use Form 709 to report and manage legal tax obligations.

- Trustees & Executives Receiving Substantial Gifts: These individuals must also consider using Form 709 for any significant asset transfers they receive.

Key Elements of Form 709

Form 709 comprises several sections, each with unique requirements to ensure proper reporting:

- Donor Information: Completes the necessary background information on the person or entity making the gift.

- Gifts Details: Provides clear identification, valuation, and description of gifts.

- Computation of Tax: Establishes the total gift tax and any previously applied credits or deductions.

- Election Statements: Offers checkboxes or spaces for specific decisions about gift splitting or tax election considerations.

IRS Guidelines

The IRS provides comprehensive guidelines surrounding Form 709:

- Record Keeping: Maintain records of all gifts and transfers, along with valuations and supporting documents, which may be required in event of an audit.

- Annual Limits and Exclusions: Adhere to annual guidelines on exclusions and taxable limits, updated by the IRS annually.

- Compliance Protocol: Ensure identification of all financial transactions comprehensively match IRS reporting requirements.

Filing Deadlines and Important Dates

Being aware of deadlines ensures timely filing and compliance:

- Annual Filing Date: Typically, Form 709 must be filed by April 15, coinciding with the annual individual tax return deadline.

- Extensions: File for an extension through IRS Form 4868 if additional time is needed to gather information or prepare the form.

Penalties for Non-Compliance

Failure to comply with Form 709 requirements can lead to penalties:

- Monetary Fines: Inaccurate or non-disclosure can result in monetary penalties, calculated as a percentage of delayed or unpaid taxes.

- Interest on Unpaid Taxes: Any taxable amount not reported will also accrue interest until paid.

- Legal Repercussions: Severe cases of non-compliance might lead to legal scrutiny or action by the IRS.

Meticulous reporting and a clear understanding of Form 709's requirements are vital for individuals with significant gifting activities or those managing estate planning, ensuring they remain in compliance with IRS tax obligations.