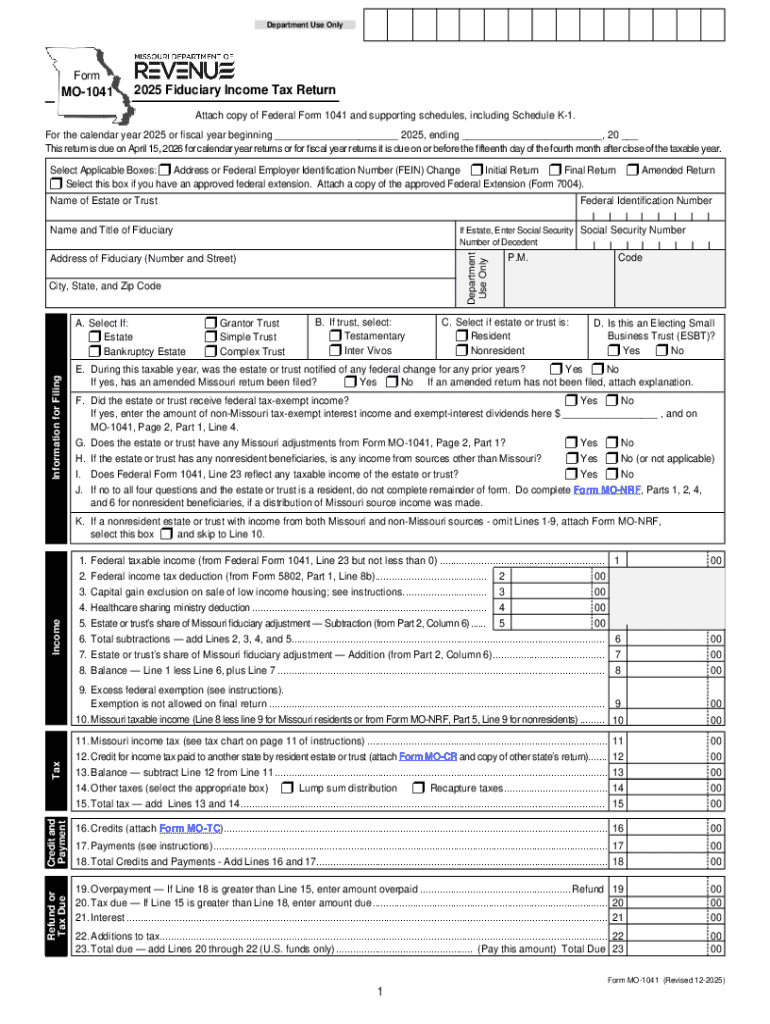

Definition & Meaning

The DOR: Fiduciary Income Tax Forms are designed for fiduciaries, including trustees and estate administrators, responsible for managing income-generating assets for the benefit of a beneficiary. These forms are critical for reporting income, deductions, and tax liabilities for trusts and estates, ensuring compliance with state and federal tax regulations. The use of these forms helps legitimate beneficiaries receive their proper income in accordance with legal guidelines.

Key Elements

- Income Reporting: Fiduciary income from interest, dividends, or capital gains must be accurately reported.

- Deductions: Allowances for trustee fees, legal expenses, and other related costs.

- Beneficiary Distributions: Details on distributions made to beneficiaries.

- Schedule K-1: Attached to report the beneficiary’s share of income.

How to Use the DOR: Fiduciary Income Tax Forms

Using these forms involves gathering necessary financial data related to the trust or estate, such as income, deductions, and distributions. Familiarity with tax codes and regulations specific to fiduciary responsibilities is crucial for accurate completion and submission.

Steps to Use

- Collect Financial Records: Maintain organized documentation regarding income and expenses.

- Fill the Form: Input data accurately reflecting the trust or estate’s financial activities.

- Attach Supporting Documents: Include Schedule K-1 and any federal forms like 1041.

- Review and Verify: Ensure all details are correct and supported by documentation.

- Submission: Submit according to state guidelines, ensuring deadlines are met to avoid penalties.

Steps to Complete the DOR: Fiduciary Income Tax Forms

Completing these forms requires a sequential approach to capture all necessary fiduciary information. Accuracy is crucial to ensure compliance and avoid audits.

Comprehensive Steps

- Download the Form: Access from the Department of Revenue’s website or request a mailed copy.

- Identify Fiduciary: Provide essential details such as the name of the trust or estate and fiduciary contact information.

- Income Entries: Input total income figures derived from all fiduciary activities.

- Deductions and Credits: Accurately report eligible deductions to reduce tax liabilities.

- Complete Schedule K-1: Allocate income to beneficiaries for their individual tax reporting.

- Finalize the Form: Double-check entries and ensure all required attachments are included.

- Sign and Date: The responsible fiduciary must sign to authenticate the submission.

Who Typically Uses the DOR: Fiduciary Income Tax Forms

These forms are primarily used by fiduciaries such as trustees, executors, and administrative professionals managing estate or trust income. The complexity of these roles necessitates a thorough understanding of fiduciary tax obligations.

Common Users

- Trustees: In charge of trusts benefiting family members or charitable causes.

- Estate Administrators: Handling estates post-mortem until asset distribution.

- Legal and Accounting Professionals: Assist fiduciaries in meeting obligations.

IRS Guidelines

The Internal Revenue Service provides specific guidelines for reporting fiduciary income. Understanding these guidelines ensures compliance and accurate tax reporting.

Important IRS Aspects

- Form 1041: Required for U.S. income tax returns of estates and trusts.

- Schedule K-1: Necessary for detailing beneficiaries’ income, deductions, and credits.

- Filing Thresholds: Knowing income levels that require fiduciary return filings.

Filing Deadlines / Important Dates

Adhering to filing deadlines is crucial for avoiding penalties. The deadline for fiduciary income taxes typically aligns with calendar year reporting unless an extension is granted.

Key Deadlines

- Standard Filing Deadline: April 15, or the next business day if this falls on a holiday or weekend.

- Extension Applications: Use Form 7004 to apply for a six-month extension.

- Quarterly Payments: Align with estimated tax payment requirements if applicable.

Form Submission Methods (Online / Mail / In-Person)

Various submission methods are available, facilitating ease of processing and compliance.

Methods of Submission

- Online Filing: Access digital platforms, often integrated with state websites or professional tax software.

- Mail Submission: Send completed forms and attachments to the designated Department of Revenue office.

- In-Person Submission: Visit local tax authority offices, though this method is less common.

Penalties for Non-Compliance

Failing to comply with filing requirements incurs penalties, including both fines and interest charges. Knowledge of these deterrents is crucial for fiduciaries.

Non-Compliance Consequences

- Late Filing Penalties: Charges accrue for each month a return is late.

- Underpayment Penalties: Imposed for underestimating and underpaying required tax.

- Audit Risks: Increased scrutiny from IRS and state revenue entities.