Definition and Meaning

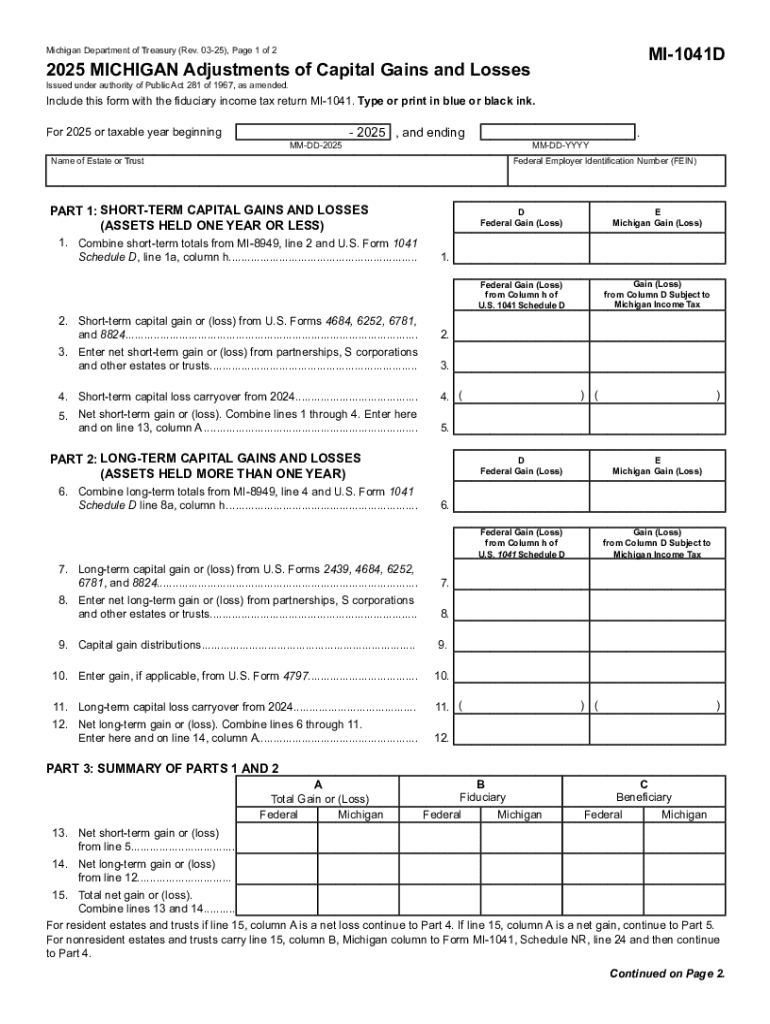

The MI-1041D, 2025 Michigan Adjustments of Capital Gains and Losses, is a state-specific tax form used primarily to report any adjustments to capital gains and losses for Michigan residents. This form aligns with Michigan's tax regulations and provides a structured way to report financial changes that result from the selling or appreciation of assets. Whether you’ve sold property, stocks, or any other asset, understanding this form is crucial for ensuring accurate tax filings in the state of Michigan.

Purpose and Scope

The primary purpose of the MI-1041D is to reconcile differences between Michigan's tax laws and federal regulations regarding capital gains and losses. It outlines specific state-level adjustments needed when federal income calculations differ from those recognized by Michigan's tax system. The form ensures taxpayers comply with both state and federal tax obligations, avoiding financial discrepancies and potential audits.

How to Use the MI-1041D

Preparing Necessary Information

Before using the MI-1041D, ensure you gather all relevant financial documentation. This includes records of asset sales, purchase prices, improvement costs, and previous depreciation. Collecting these records helps in accurately determining your gains or losses and assists in eliminating errors during form completion.

Completing the Form

-

Identify Adjustments: Start by identifying the specific adjustments needed to align your federal gains and losses with Michigan tax requirements. This involves section analysis and precise calculations to determine discrepancies.

-

Enter Adjustments: Populate the form with adjustments identified in the previous step. Make sure to follow instructions to accurately reflect differences.

-

Verification: Double-check entries for accuracy, ensuring that all figures correspond with supporting documents. Accurate data entry is critical for tax compliance and reducing the risk of penalties.

Steps to Complete the MI-1041D

Detailed Instructions

-

Read the Instructions: Begin by reviewing the form instructions provided by the Michigan Department of Treasury. Understanding these guidelines is essential for accurate form completion.

-

Calculate Adjustments: Carefully calculate any necessary adjustments. This involves totaling your Michigan-specific capital gain or loss by applying state adjustments to your federal amounts.

-

Documenting Entries: Methodically complete each line item according to the instructions. Ensure each calculation correlates correctly with your records and the adjustments are supported.

-

Review and Submit: Review the form for completeness and accuracy before submission. Submit through the preferred method – mail, electronic filing, or through a tax professional.

Important Terms Related to MI-1041D

Definitions

- Capital Gain: Profit from the sale of a property or investment over its purchase cost.

- Capital Loss: Loss from the sale of a property or investment below its purchase cost.

- Adjusted Basis: The net cost of an asset after accounting for improvements, depreciation, and other adjustments.

- Short-Term vs Long-Term Gains: Distinguish gains based on the holding period of the asset, affecting tax rates.

Who Typically Uses the MI-1041D

Applicable Taxpayers

This form is predominantly used by Michigan residents who have engaged in sale transactions involving capital assets during the tax year. These include:

- Individuals: Those who have sold properties, stocks, or investments need to report capital events.

- Estates and Trusts: Entities involved in managing deceased persons' financial obligations frequently use this form to comply with tax regulations.

- Business Owners: Certain business structures, when disposing of assets, require adjustments reported via MI-1041D.

Business Entity Types

- LLCs and Corporations: Such entities need to reconcile their federal returns with state obligations.

- Partnerships: Partners who sell partnership interests may find themselves using the MI-1041D to report state-specific adjustments.

State-Specific Rules for MI-1041D

Michigan Tax Regulations

Michigan imposes distinct rules differing from federal guidelines, making this form necessary for addressing adjustments. Understand Michigan's criteria for capital gains and losses, such as:

- Differing Deduction Limits: Michigan may have varying limits or conditions for deductions compared to federal standards.

- Unique Taxable Items: Certain gains or losses may be exclusively recognized under Michigan law, necessitating detailed reporting for compliance.

IRS Guidelines and Compliance

Relevance to Federal Tax Code

While the MI-1041D addresses Michigan-specific issues, familiarity with the Internal Revenue Code is indispensable. Harmonizing state-specific filings with federal requirements ensures smoother tax processes and reduces legal risks with the IRS.

Penalties for Non-Compliance

Failure to accurately complete and file the MI-1041D may lead to penalties, interest charges, or audits. Adherence to both state and IRS guidelines is crucial for maintaining tax compliance and safeguarding financial interests.

Examples of Using the MI-1041D

Practical Scenarios

- Sale of Primary Residence: A Michigan resident sells their home but experiences a divergence in federal and state gain calculations due to Michigan-specific exclusions or inclusions.

- Investment Divestitures: An individual cashing in stock options must adjust for Michigan’s differing tax treatment of the gains.

Hypothetical Case Studies

- Retiree Scenario: A retiree’s portfolio reallocation necessitates reporting Michigan-based capital transactions adjustments on gains.

- Small Business Liquidation: An LLC liquidating its asset inventory must address state-specific capital adjustments with the MI-1041D.

Filing Deadlines and Important Dates

Submission Timing

Ensure the MI-1041D is filed in concert with Michigan income tax returns. Adhering to state deadlines, often paralleling federal deadlines, secures timely submission and avoids incurring late fees or penalties.