Definition & Meaning of TC-20 Form

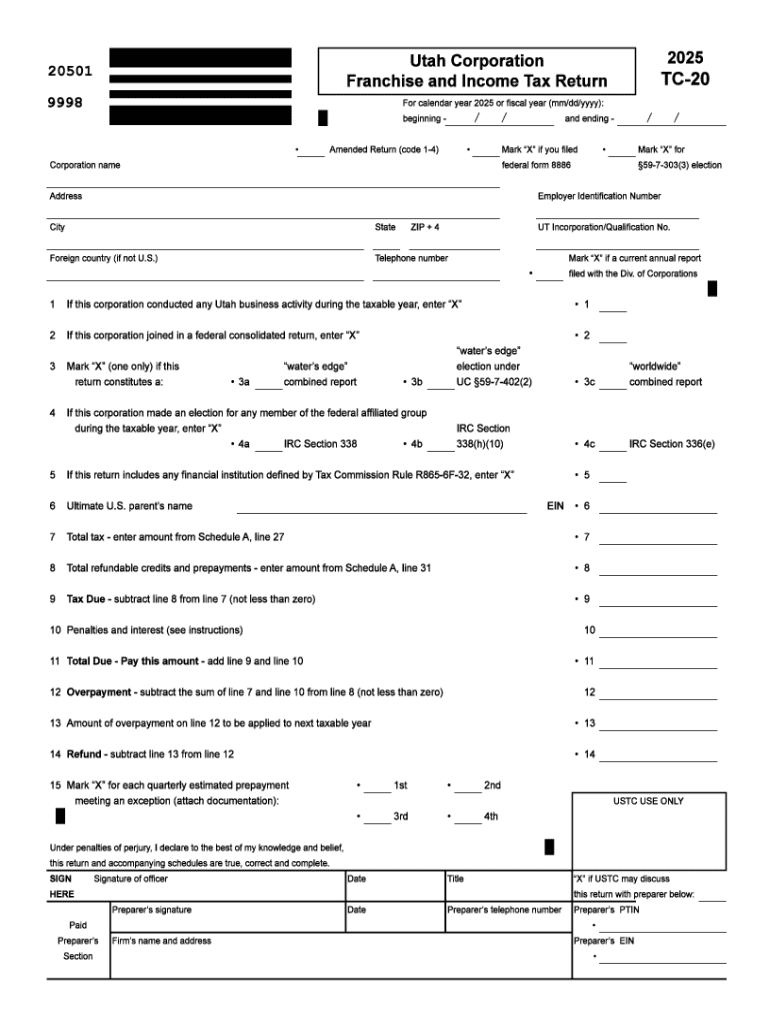

The TC-20 Form is used by businesses in Utah to report their corporation franchise or income tax. It's essential for corporations conducting business within Utah, enabling them to accurately declare their taxable income and compute the amount owed to the state's tax authority. The form serves both as a declaration and a calculation tool for corporate taxes. Understanding its components and purpose is crucial for compliance with Utah's tax regulations.

- Franchise Tax: Imposed on businesses for the privilege of operating in Utah.

- Income Tax: Based on the net income of the corporation, relevant to those with a taxable income derived from Utah sources.

Steps to Complete the TC-20 Form

Completing the TC-20 Form requires careful attention to detail and thorough documentation. Here are the general steps one needs to follow:

- Basic Information: Provide the corporation's name, address, and federal employer identification number (EIN).

- Income Declaration: Report gross income from all sources.

- Deductions and Credits: Include allowable deductions and credits to determine taxable income.

- Tax Calculation: Compute the tax owed based on Utah's tax rates.

- Payment: Arrange for payment if taxes are owed after computations and credits.

Each section of the form is connected, ensuring all relevant income and expenses are accurately recorded. Careful completion is necessary to avoid penalties for underpayment.

How to Obtain the TC-20 Form

Acquiring the TC-20 Form is a straightforward process. Businesses can download it from the Utah State Tax Commission's official website. This ensures all instructions and updates to the form are accessible and correct:

- Online Access: Visit the Utah State Tax Commission website to download a PDF version of the TC-20 Form.

- Physical Copies: Request a paper version by contacting the Tax Commission, although online access is quicker.

Important Terms Related to TC-20 Form

Understanding key terms ensures the correct completion of the TC-20 Form:

- Taxable Year: The financial period for which the tax is calculated, typically coinciding with the fiscal year.

- Apportionment: The method used to determine the portion of a corporation's income subject to Utah tax.

- Tax Credits: Reductions in tax owed, including specific credits that apply under Utah tax law.

Legal Use of the TC-20 Form

The TC-20 Form is a legal requirement for corporations operating in Utah. Non-compliance may result in penalties. It's crucial that corporations use the form to meet:

- State Tax Obligations: Ensuring that all income derived from Utah sources is taxed appropriately.

- Legal Compliance: Prevent penalties by adhering to submission deadlines and accuracy requirements.

State-Specific Rules for the TC-20 Form

Utah-specific regulations govern the TC-20 Form, reflecting local tax law nuances:

- Utah Tax Credits: Various credits available to offset tax liability, such as renewable energy credits.

- Filing Requirements: Corporations, including C-Corporations and S-Corporations, must follow distinct rules under Utah law.

Filing Deadlines / Important Dates

Timely submission of the TC-20 Form is crucial for avoiding penalties:

- Filing Deadline: Generally April 15th, aligning with the federal income tax due date, unless an extension is granted.

- Extension Requests: Corporations can file for an extension but must pay an estimated amount by the original due date.

Penalties for Non-Compliance

Failure to properly complete and submit the TC-20 Form can result in significant consequences:

- Late Filing: Penalties accrue for each month or part of a month a return is late.

- Underpayment: Additional fees apply for not paying the full amount of tax owed by the due date.

Form Submission Methods

The TC-20 Form can be submitted through various channels:

- Online Filing: Preferred for speed and efficiency, the form can be submitted electronically through the state’s e-file system.

- Mail: Paper forms can be mailed to the Utah State Tax Commission, but allow extra time for processing.

- In-Person: Submission at local Tax Commission offices for those who prefer direct interactions.

Each method has its protocols, and electronic submission is often recommended for accuracy and convenience.