Definition & Meaning

The Missouri Employer Withholding Tax is a state-imposed levy that employers in Missouri are required to withhold from employee wages for state income tax purposes. This tax ensures that employees' state income taxes are collected throughout the year, reducing the likelihood of a large tax bill when individuals file their annual returns. Employers facilitate the collection of these taxes by withholding a specified amount from each employee's paycheck, which is then remitted to the Missouri Department of Revenue. The process is integral to the state's tax collection system and ensures funding for public services.

How to Use the Missouri Employer Withholding Tax

Employers must calculate the appropriate amount to be withheld based on each employee's earnings and submit these withholdings to the Missouri Department of Revenue. Here's how the process typically works:

-

Determine employee exemptions and allowances: Employees submit Form MO W-4 to indicate the number of exemptions they are eligible for, which affects the withholding amount.

-

Use the withholding tables: Use the appropriate withholding tables provided by the Missouri Department of Revenue, which outline how much to withhold based on earnings and exemptions.

-

Regular deposits: Remit withheld taxes to the state on a regular schedule - typically monthly or quarterly based on the total withholding amount.

-

Filing returns: File Form MO-941 quarterly to report withholding amounts.

Employers are recommended to keep accurate records of all withholdings and payments to maintain compliance and facilitate audits if necessary.

Steps to Complete the Missouri Employer Withholding Tax

Completing employer withholding obligations involves a series of steps to ensure accuracy and compliance:

-

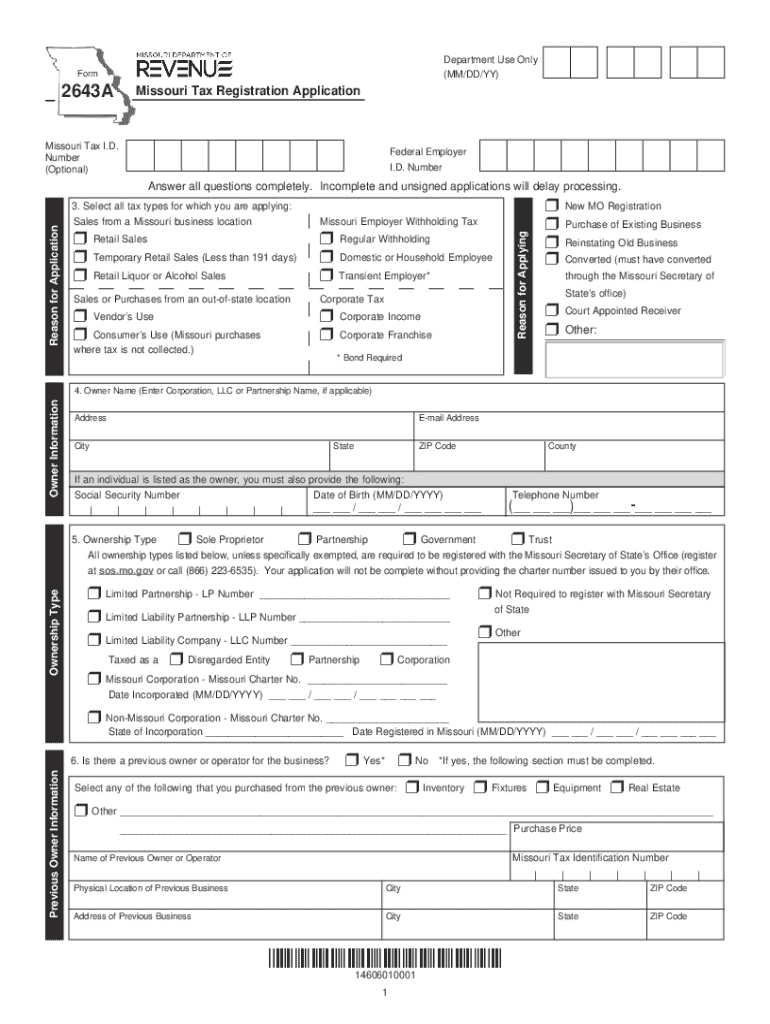

Register with the Department of Revenue: New employers must complete the Missouri Tax Registration Application (Form 2643A) to obtain a withholding tax account.

-

Collect employee information: Securely collect all necessary personal and tax information from employees via Form MO W-4.

-

Calculate withholdings: Determine withholdings using Missouri's current tax tables and calculators.

-

Deposit withheld taxes: Depending on your withholding amounts, make deposits either monthly, quarterly, or annually.

-

File quarterly and annual reports: Submit quarterly reports using Form MO-941 and annual reconciliations via Form MO W-3 with copies of all W-2 forms.

Who Typically Uses the Missouri Employer Withholding Tax

The Missouri Employer Withholding Tax is primarily used by:

- Small and Medium-Sized Business Owners: Businesses employing staff in Missouri must adhere to withholding tax regulations.

- Payroll Departments: Personnel responsible for handling payroll and tax submissions must manage withholding calculations and payments.

- Accountants and Tax Professionals: Experts who advise on and prepare tax-related documents for businesses.

- Non-Profit Organizations: Entities with employees are also liable for employment taxes, including withholding.

This tax applies to entities with employees receiving wage income in Missouri, spanning various industries and organizational structures.

Key Elements of the Missouri Employer Withholding Tax

-

Withholding Calculations: Based on employee income and tax exemptions.

-

Deposit Requirements: Frequency of tax deposits depends on withholding amounts.

-

Reporting: Regular submissions of forms to report and reconcile withholding totals.

-

Compliance: Staying compliant with regulations and maintaining records.

State-Specific Rules for the Missouri Employer Withholding Tax

Missouri has specific guidelines that govern employer withholding obligations:

-

Resident and Non-Resident Rules: Withholding rules apply to both resident and non-resident employees working in Missouri.

-

Tax Table Updates: Employers should be aware of periodic updates to tax tables for accurate withholding.

-

Record-Keeping Requirements: Employers must retain records of all withholding amounts, reported forms, and employee details for a minimum of three years.

-

Penalties for Late Payments: Late deposits may incur penalties and interest charges.

Understanding and adhering to these state-specific rules ensures employers remain compliant with Missouri’s withholding tax requirements.

Filing Deadlines / Important Dates

Employers need to adhere to key deadlines for filing and deposit submission:

-

Monthly depositors: Generally deposit by the 15th of the following month.

-

Quarterly filing for Form MO-941: Due on the 30th day of the month following the end of each quarter.

-

Annual reconciliation for Form MO W-3: Due by January 31, along with W-2 forms to report wages and taxes withheld.

All employers should mark these deadlines on their calendars to avoid late fees and ensure compliance.

Penalties for Non-Compliance

Non-compliance with Missouri's withholding requirements can result in significant penalties:

-

Late Filing Penalties: A percentage of the tax due may be assessed for late filing of returns.

-

Interest on Late Deposits: Unpaid withholdings accrue interest until full payment is made.

-

Fines for Negligence or Fraud: Intentional underreporting or fraud may result in additional fines and legal action.

Adhering to withholding tax obligations reduces risk and ensures sound business practices in Missouri.