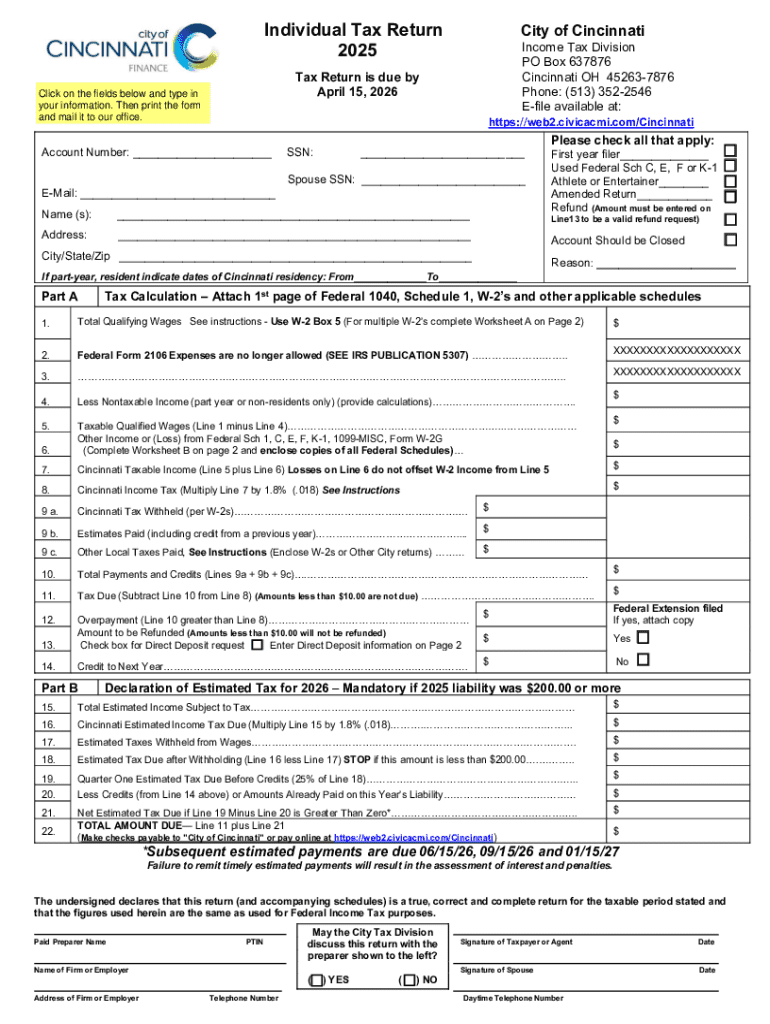

Definition and Meaning

The "Tax Return and Instructions - Finance" form is a comprehensive document required for individuals and businesses to report their income, calculate their tax liability, and specify financial transactions during a fiscal year. This form serves as a critical tool for tax compliance, enabling taxpayers to fulfill their financial obligations to federal and state governments. In the United States, these tax returns can differ based on the taxpayer's specific circumstances, such as income level, deductions, and credits available. Each component of the form is designed to provide a detailed snapshot of an individual's or entity's financial activity.

Taxes levied by the IRS help fund various public services and infrastructure. Thus, accuracy in reporting is emphasized to ensure each taxpayer contributes their fair share. The form may include sections for reporting income types, deductions, exemptions, and credits, all of which can significantly alter the amount of tax owed or refunded.

Steps to Complete the Tax Return and Instructions - Finance

Completing the "Tax Return and Instructions - Finance" form requires a methodical approach to ensure all relevant income and deductions are accurately reported. Here's a detailed breakdown of the process:

-

Gather Required Documents: Collect all necessary financial documents, such as W-2s for employment income, 1099s for independent contractor work, mortgage interest statements, and previous year's tax returns, as these form the foundation for accurate reporting.

-

Choose the Correct Form: Identify the specific tax return form that matches your filing status and income type. For instance, individual taxpayers often file a Form 1040, while businesses might use varying forms based on their structure.

-

Report Income: Enter all sources of income, including wages, dividends, rental income, and any other taxable revenue streams. All income must be accurately recorded to prevent discrepancies with IRS records.

-

Calculate Deductions and Credits: Utilize eligible deductions such as student loan interest, medical expenses, and retirement contributions. Tax credits significantly impact the bottom line, reducing the total tax payable directly. Common credits include the Earned Income Tax Credit (EITC) and the Child Tax Credit.

-

Determine Tax Liability or Refund: Using the IRS tax tables and your calculated deductions and credits, determine your total tax liability. If the withheld tax exceeds liability, a refund is due. Otherwise, the balance must be paid to the IRS.

-

Submit the Form: Decide on a submission method: electronically via certified software or by mail. Filing online is encouraged as it speeds up processing times and reduces errors.

Important Terms Related to Tax Return and Instructions - Finance

Understanding key terminology is essential when navigating the tax return process:

-

Adjusted Gross Income (AGI): This is your gross income minus specific adjustments, serving as the pivotal benchmark in determining eligibility for deductions and credits.

-

Tax Deduction: These reduce the total taxable income, which might include items like mortgage interest or charitable contributions.

-

Tax Credit: Unlike deductions that lower taxable income, credits directly reduce the amount of tax owed, offering potentially significant savings.

-

Exemption: Specific allowances that reduce taxable income, although recent tax reforms have altered their application.

Required Documents

Having the right documents is critical for completing the tax form accurately. Here’s what you need:

-

Income Statements: W-2s for wage income, 1099s for contract or miscellaneous income, and other proof of income, such as bank interest statements.

-

Deduction Documentation: Receipts for itemized deductions, such as charitable donations, medical expenses over the allowable limits, and student loan interest.

-

Prior Year Tax Return: Useful for reference, especially for carryover credits or deductions.

Legal Use of the Tax Return and Instructions - Finance

The "Tax Return and Instructions - Finance" form must be used in accordance with U.S. tax regulations. Filers must provide true and accurate information, ensuring compliance with the IRS standards. Misrepresentations can result in penalties or legal action, underscoring the importance of transparency and accuracy.

For those unsure about the complexity of their finances, professional tax filing assistance is recommended. Services from a certified accountant can help navigate complicated scenarios, ensuring compliance with ever-evolving tax laws and leveraging available tax strategies.

IRS Guidelines

The IRS provides detailed guidelines to facilitate the completion of tax returns. Key guidelines include understanding allowable deductions, determining which income classifications apply to you, and keeping abreast of annual changes in tax regulations. Taxpayers are prompted to stay informed about updates that might affect their filing status, exemptions, and credits.

IRS guidelines also provide clarity on electronic filing, simplifying the process through step-by-step instructions and frequently asked questions. These resources are invaluable for ensuring that taxpayers file accurate and timely returns.

Filing Deadlines and Important Dates

Filing deadlines are vital to ensuring compliance and avoiding late fees or penalties. For most individuals, tax returns are due by April 15 of each year. However, if this date falls on a weekend or holiday, the deadline extends to the next business day. Extensions can be requested, offering additional time to file, though any taxes owed must still be paid by the April deadline to avoid interest and penalties.

Taxpayer Scenarios: Self-Employed and Retired Individuals

Different taxpayer scenarios necessitate tailored approaches to filing:

-

Self-Employed Individuals: Must report all self-generated income, pay estimated taxes quarterly, and maintain meticulous records of business expenses and related deductions.

-

Retired Individuals: Should report income from pensions, social security, and retirement accounts. Certain withdrawals might have specific tax implications, requiring careful management.

Understanding these variations helps ensure that all taxpayers, regardless of their financial situation, meet their obligations accurately and efficiently.