Definition and Meaning

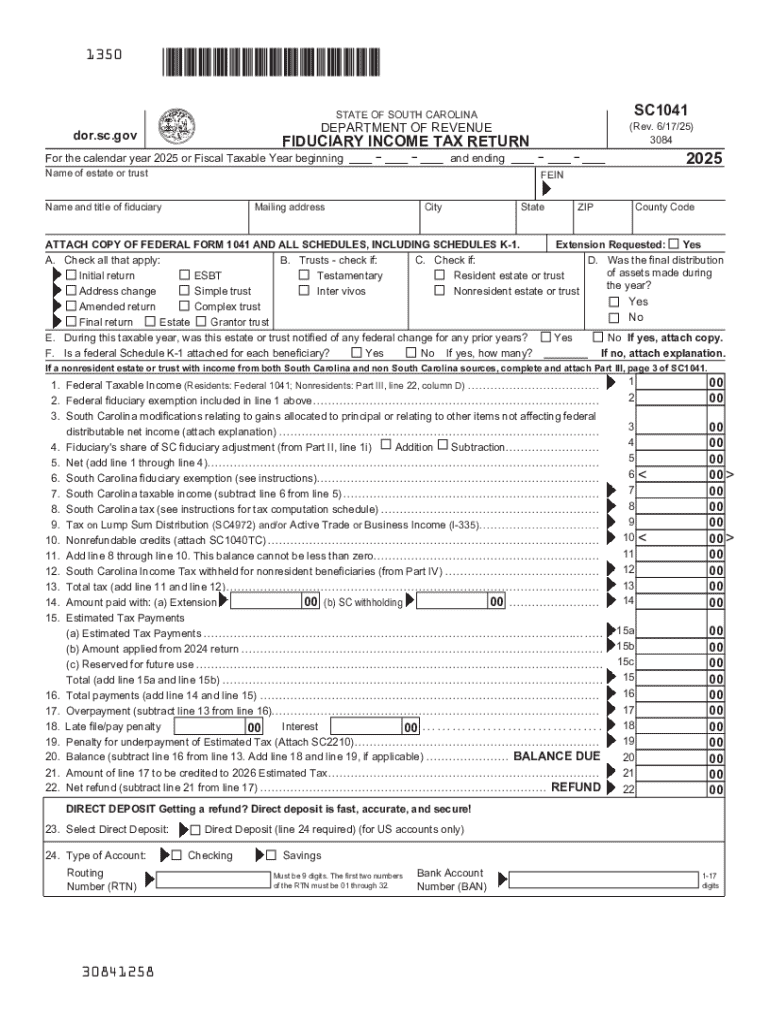

"For the calendar year 2025 or Fiscal Taxable Year beginning" refers to the fiscal year parameters used when filing certain tax forms in the United States. This phrase indicates whether the taxpayer is using the standard calendar year (January 1 to December 31) or a specific fiscal year that begins at any point during 2025 other than January 1. Understanding this terminology is crucial for accurately reporting income, expenses, and compliance with tax regulations. Fiscal years may align differently depending on the specific needs of a business or individual, providing flexibility in tax reporting.

Examples of Fiscal Year Use

- Corporations: Some corporations may choose a fiscal year that aligns with the natural flow of their business, such as a retailer using a fiscal year ending in January after the holiday season to better match revenue and expenses.

- Non-profit Organizations: Often have fiscal years that align with grant cycles or funding patterns.

How to Use the Form

To use the "For the calendar year 2025 or Fiscal Taxable Year beginning," one should first determine the relevant period for financial reporting. Most individuals default to calendar year reporting for simplicity, while businesses might select fiscal years for strategic financial planning. The form should explicitly indicate which type of year is being used, as this will affect the tax calculations and deadlines.

Steps to Determine Your Fiscal Year

- Assess Business Cycle: Consider your business cycle and identify the most effective end date to capture a complete fiscal period.

- Consult Financial Advisors: Engaging with a certified public accountant (CPA) can provide tailored advice ensuring that your fiscal year optimizes financial reporting.

- File Appropriate Forms: When establishing or changing fiscal years, ensure that all required forms are submitted to the IRS in compliance with regulations.

Steps to Complete the Form

Completing the form for tax purposes involves a meticulous process to ensure all income, deductions, and credits are accurately reported.

- Gather Documents: Assemble all pertinent financial documents, including income statements, receipts, and previous tax returns.

- Confirm Reporting Period: Verify whether using the calendar year or a fiscal year, which will guide the reporting and calculations.

- Fill in Basic Information: Complete sections on personal or business details, including names, addresses, and tax identification numbers.

- List Income and Deductions: Document all sources of income and applicable deductions to ensure a comprehensive filing.

- Calculate Tax Liability: Using either a tax preparation software or manual calculations, determine the total amount of tax due.

- Review for Accuracy: Double-check all entries for accuracy to avoid errors that might lead to penalties or audit flags.

- Submit Form: File the completed form with the IRS by the applicable deadline, either electronically or via mail.

Practical Example

- Small Business Owner: A sole proprietor using a calendar year would report all income and expenses from January 1 to December 31, ensuring alignment with personal tax obligations.

Important Terms Related to the Form

Familiarity with key terms associated with the "For the calendar year 2025 or Fiscal Taxable Year beginning" is essential for accurate form completion.

- Tax Year: The accounting period for which tax returns are prepared, either fiscal or calendar.

- Fiscal Year: A 12-month period used for accounting that does not start on January 1; can be any period as long as it is consistently applied.

- Standard Deduction: A portion of income not subject to tax, reducing overall liability.

- Itemized Deductions: Specific expenses allowed to be deducted from gross income to reduce taxable income.

- Adjusted Gross Income (AGI): An individual's total gross income minus specific deductions.

IRS Guidelines

The IRS provides specific guidelines to ensure compliance when using "For the calendar year 2025 or Fiscal Taxable Year beginning."

- Declaration Requirements: Mandates businesses declare their chosen fiscal or calendar year upon formation and maintain consistent use.

- Change of Accounting Period: To change a fiscal year once established, approval from the IRS via Form 1128 or other specified forms is typically required.

- Record Retention: Maintain financial records for at least three to seven years depending on the nature of the tax components being reported.

Considerations for Compliance

- Regular Updates: Regular consultations with IRS announcements and tax law changes can prevent non-compliance.

- Professional Assistance: Utilizing services such as those offered by tax professionals or software (TurboTax, QuickBooks) ensures precision and adherence to IRS regulations.

Filing Deadlines and Important Dates

Understanding critical dates ensures the timely submission of tax forms and avoids penalties.

- Standard Calendar Year Deadline: Typically April 15 following the calendar year unless extensions are granted.

- Fiscal Year Deadline: The fifteenth day of the fourth month following the end of the fiscal year.

- Extended Deadlines: Extensions may be requested, offering an additional six months for both fiscal and calendar year taxpayers under specific circumstances.

Business Entity Types Relevant to the Form

Different entities have diverse requirements and benefits associated with their choice of fiscal year.

- Limited Liability Companies (LLC): Can elect fiscal years based on member needs, subject to IRS approval.

- Corporations: Commonly adopt fiscal years that optimize business cycle reporting.

- Partnerships: Typically align with the fiscal year of majority partners or partners with the largest share of profits.

State-Specific Rules

While federal guidelines provide a framework for using the calendar or fiscal year, each state may have unique requirements affecting the use of this designation in tax filing.

- State Income Tax: Some states have specific forms based on either calendar or fiscal years, necessitating separate submissions.

- Filing Requirements: Requirements for fiscal year reporting can vary, requiring attention to detail in multi-state operations.

State Variations

- California: May have different definition and treatment for certain deductions or credits; understanding state-specific requirements essential.

- New York: Often mirror federal mandates but with specific state-level forms and processes.

Key Takeaways

Understanding and applying the correct use of "For the calendar year 2025 or Fiscal Taxable Year beginning" is crucial to ensure compliance and efficient tax planning. By aligning your tax reporting with the appropriate year, utilizing all available deductions, and adhering to federal and state guidelines, you can effectively manage your tax obligations.

Summary of Essential Points

- Determine whether to use calendar or fiscal year based on strategic financial planning.

- Follow detailed IRS rules and state-specific regulations.

- Ensure timely filing and accurate reporting to prevent penalties or adjustments.

- Leverage professional resources and software for optimal compliance and accuracy.