Definition & Meaning

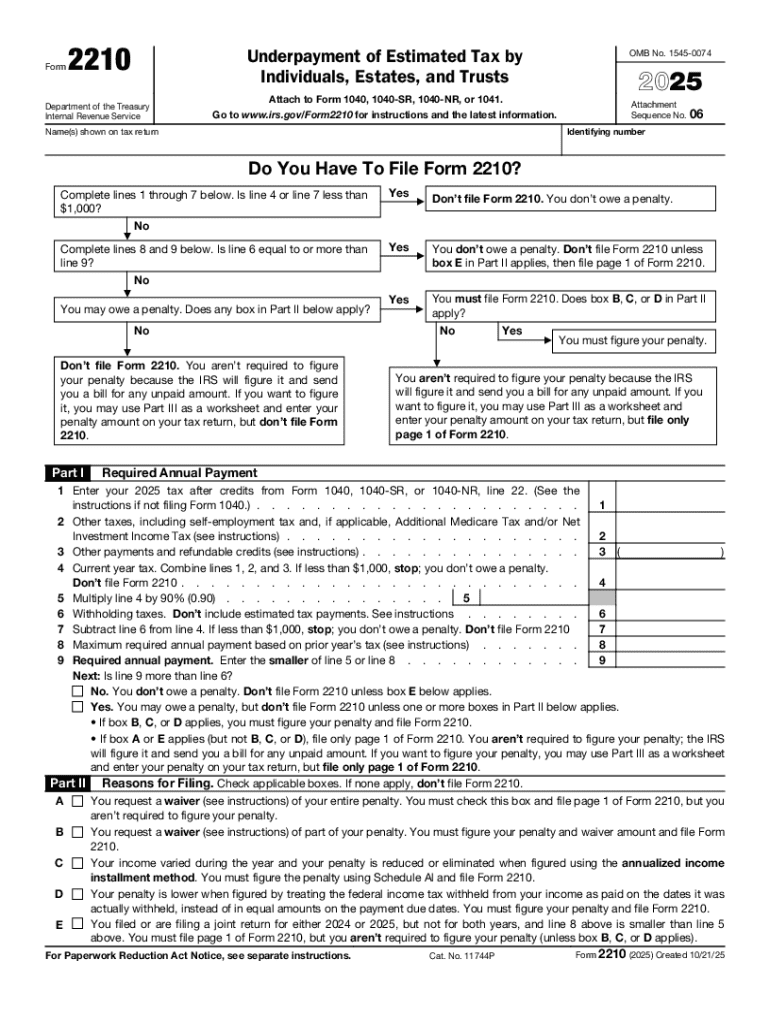

The "2025 Form 2210," officially titled "Underpayment of Estimated Tax by Individuals, Estates, and Trusts," is issued by the IRS. It helps taxpayers determine whether they owe a penalty for underpaying estimated taxes throughout the year. The form is essential for those whose income is not subject to withholding, such as self-employed individuals or investors with substantial income from dividends, capital gains, or other sources.

How to Use the 2025 Form 2210

To use Form 2210 effectively, taxpayers should start by gathering all their relevant income documentation for 2025. This includes W-2s, 1099s, and any other records of income received throughout the year. Using this form, taxpayers can calculate their total estimated tax liability and compare it with actual payments made. The form guides users through various mathematical computations to determine if there is an underpayment and, if so, the amount of penalty owed.

Steps to Complete the 2025 Form 2210

- Collect Necessary Documents: Ensure all sources of income and prior estimated tax payments are documented.

- Calculate Annualized Income: Use available worksheets to determine income at various points during the year.

- Compute Penalty: Follow the instructions provided to calculate any potential underpayment penalty.

- Attach to Tax Return: Complete the form and attach it to your 1040, 1040-SR, or other appropriate tax return forms before submission.

Key Elements of the 2025 Form 2210

- General Information: Basic taxpayer details such as name, Social Security Number, and filing status.

- Underpayment Penalty Calculation: Step-by-step instructions to compute the penalty owed if payments fall short.

- Annualized Income Worksheet: Allows adjustments based on varying income levels throughout the fiscal year.

- Exceptions and Waivers: Situations where penalties might be reduced or waived entirely based on taxpayer circumstances.

Important Terms Related to 2025 Form 2210

- Estimated Tax: Advance payments made to the IRS on income that is not subject to withholding.

- Safe Harbor Rule: A condition that can protect taxpayers from penalties if they pay a certain percentage of the previous year's tax liability.

- Underpayment: Occurs when the taxes paid through estimated payments fall short of the actual tax liability.

Penalties for Non-Compliance

Failing to calculate and pay the appropriate estimated tax can result in penalties. The IRS sets penalties based on the federal short-term interest rate plus a specific percentage. Penalties are calculated for each period of underpayment, and failing to pay on time can result in additional interest accruals, thereby increasing the total liability.

IRS Guidelines

The IRS provides comprehensive guidelines on completing Form 2210. These guidelines include examples of computation, exceptions, and different scenarios under which certain penalties might be waived. Taxpayers should consult the official IRS instructions alongside the form to ensure accurate completion.

Filing Deadlines / Important Dates

The typical deadlines for estimated tax payments are April 15, June 15, September 15, and January 15 of the following year. Marking these dates is crucial, as they are the times when taxpayers need to assess their estimated payments for the current fiscal quarter. Adhering to these deadlines minimizes potential penalty amounts and aligns taxpayer actions with official IRS schedules.