Definition and Purpose of the 2025 Form 709

The 2025 Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, is a tax form used to report gifts made during the calendar year by individuals in the United States. This form serves multiple functions, primarily documenting the transfer of property without compensation, which may include real estate, physical items, or monetary gifts. It is crucial for individuals who exceed the annual exclusion amount to report these transactions to the IRS. Furthermore, the form ensures transparency and proper computation of applicable taxes related to these gifts, including any generation-skipping transfer taxes when property is transferred to beneficiaries who are two or more generations below the donor.

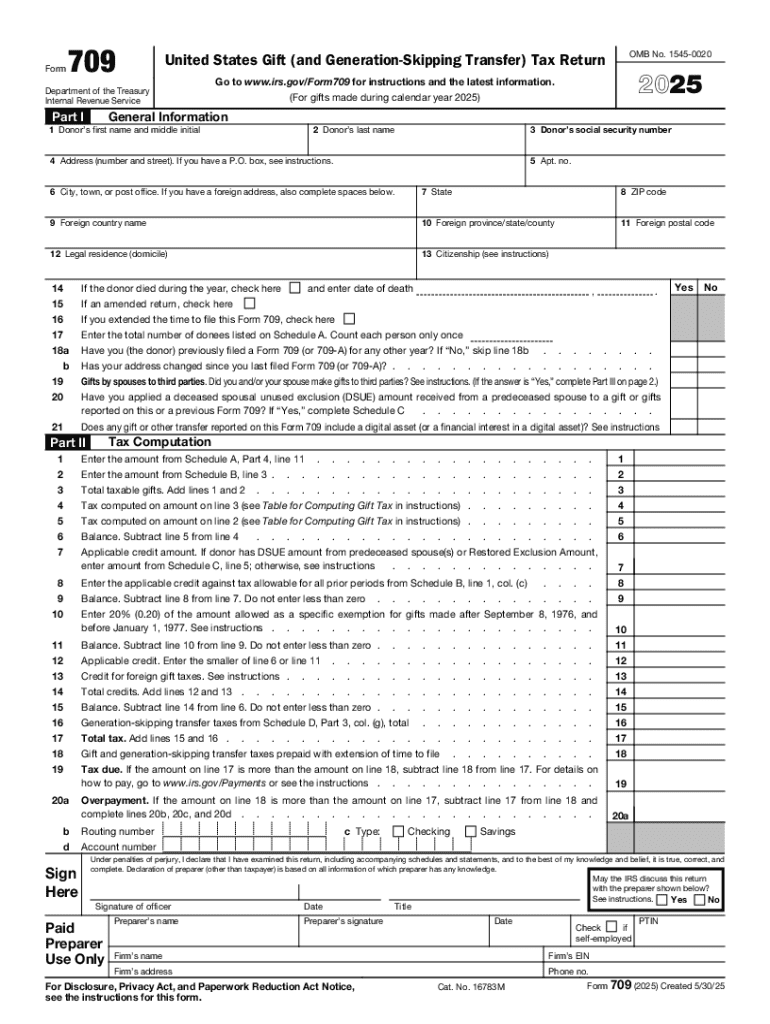

Key Sections of the Form

- Donor Information: This section collects personal details about the individual making the gifts, such as their full name, Social Security number, and contact information.

- Tax Computation: Details how to calculate the total gift tax owed, accounting for any applicable deductions or exclusions.

- Schedules for Gift Details: Provides space to itemize the gifts, their fair market value, and any charitable deductions or credits applied.

- Generation-Skipping Transfers: Addresses transfers subject to additional tax due to the significant generational gap between the donor and recipient.

How to Use the 2025 Form 709

Filling out the 2025 Form 709 requires meticulous attention to detail to ensure compliance with IRS regulations. The process involves assessing all gifts made throughout the year and determining which exceed the annual exclusion limit. Essential steps include gathering supporting documentation for each gift, including appraisals or receipts to substantiate their declared values. Furthermore, it’s important to understand the nuances of generation-skipping transfer taxes and how they may affect the total tax liability.

Step-by-Step Instructions

- Collect Donor Information: Start by filling out the personal details in Part 1 of the form.

- Calculate Gift Tax: Use Part 2 to compute the gift tax, subtracting any applicable exclusions.

- Detail Each Gift: In the schedules, itemize each gift given, including values and recipient information.

- Include Necessary Documents: Attach any required documentation such as valuations and prior gift history.

- Review for Accuracy: Double-check all entries to ensure they align with IRS guidelines and definitions.

Obtaining the 2025 Form 709

The 2025 Form 709 is accessible online via the IRS website, where it can be downloaded and printed for manual completion or filled out digitally for submission. Individuals may also receive physical copies from tax preparers or local IRS offices. For those using tax preparation software, these platforms often include the form, simplifying integration into broader tax filings.

Filing Deadlines and Important Dates

For the 2025 tax year, the form is due by April 15, 2026, aligning with the traditional tax filing deadline. Extensions may be requested if additional time is needed to gather required documentation or complete the form accurately. It's imperative to file by this deadline to avoid penalties or interest on any taxes owed, although specific circumstances may warrant exceptions or adjustments by the IRS.

Extensions and Penalties

- Extension Requests: Eligible via Form 8892 if additional filing time is needed.

- Penalties for Late Filing: Can include a percentage of the taxes owed plus interest if the form is not filed by the deadline without an approved extension.

Legal Use and Compliance

The 2025 Form 709 plays a vital role in ensuring legal compliance with the U.S. tax code concerning gifts. Proper use of the form provides a clear record of all significant gift transactions, maintaining transparency with the IRS, which is necessary for accurate tax reporting and audit protection.

IRS Recommendations and Requirements

- Documentation: Maintain copies of all documentation used to complete the form for audit purposes.

- Accuracy: Ensure all reported values and details comply with IRS standards and valuation criteria.

- Generation-Skipping Considerations: Special attention is required for transactions involving younger generations to accurately assess tax liabilities.

Who Typically Uses the 2025 Form 709

The form is primarily utilized by individuals who make substantial gifts above the annual exclusion to family members or friends. This includes high-net-worth individuals, estate planners, and advisors who assist clients in strategizing their gifting and estate transfers to minimize tax liabilities.

Common Users

- Families Planning Estate Transfers: Especially those leveraging lifetime gift exclusions to reduce estate taxes.

- High Net-Worth Individuals: With significant assets, frequently using gifting for wealth distribution.

- Professional Advisors: Assisting clients in financial planning and compliance.

Important Terms and Concepts

Understanding key terms related to this form can aid in accurate completion and compliance. These terms include "annual gift exclusion," which refers to the amount that can be gifted each year to a single recipient without incurring taxes. Another critical term is "generation-skipping transfer," a specific transaction where the gift is given to an individual at least two generations removed from the donor.

Key Definitions

- Annual Exclusion: The maximum value per gift recipient that does not require tax reporting.

- Unified Credit: The cumulative tax exclusion applicable over the donor’s lifetime.

- Fair Market Value: The estimated market price of a gifted property or asset at the time of transfer.

Examples of Using the 2025 Form 709

Real-world applications of the 2025 Form 709 often involve strategizing wealth transfers within families. For example, a grandparent making a sizable financial gift to a grandchild would need to consider both the gift tax implications and potential generation-skipping transfer tax liabilities. Scenarios where the annual exclusion is exceeded for multiple recipients also necessitate meticulous documentation and reporting to ensure IRS compliance.

Case Scenarios

- Educational Gifts: Supporting a grandchild’s tuition, potentially invoking tax considerations if exceeding exclusion limits.

- Year-End Wealth Transfers: Strategic gifting done in December to optimize annual exclusions and plan for subsequent years.

IRS Guidelines

The IRS provides various online resources and publications to assist taxpayers with questions regarding the 2025 Form 709. These resources explain the limits, documentation procedures, and any changes to tax law that may affect fill out the form. Adhering to these guidelines is paramount to ensure correct filing and avoid triggering audits or further inquiries.

Additional Resources

- IRS Publication 559: Offers insight into surviving beneficiaries and life-wealth transfer processes.

- Guidance Documents: Available on the IRS website, offering sector-specific advice and clarifications.

Required Documents

To accurately complete the 2025 Form 709, it is essential to gather all documentation related to the gifts given within the year. This includes appraisals, receipts, and any legal documents that substantiate the gift’s existence and its fair market value.

Key Documentation

- Appraisals for Property Gifts: Ensures valuation compliance.

- Receipts and Transaction Records: Serves as proof of gift transfer and valuation.

- Prior Gift Histories: Documents previous gift filings for cumulative tax purposes.