Definition & Meaning

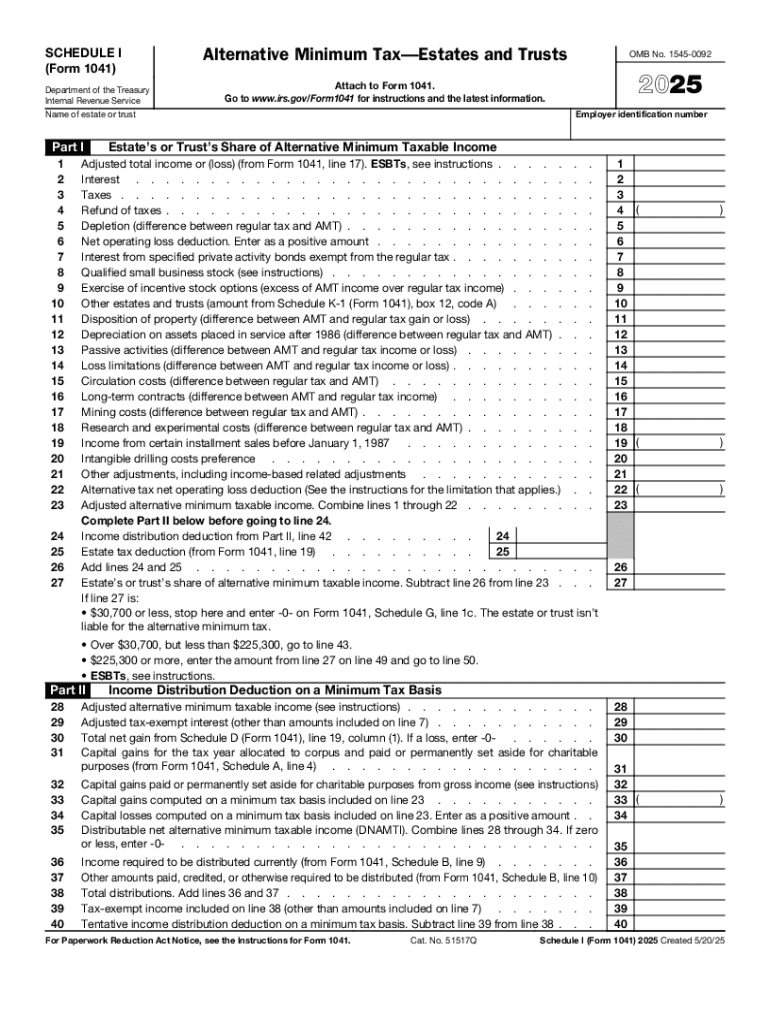

The 2025 Schedule I (Form 1041) Alternative Minimum TaxEstates and Trusts is a specific component of the U.S. tax code used to calculate the alternative minimum tax (AMT) for estates and trusts. AMT ensures that individuals or entities pay at least a minimum amount of tax, regardless of deductions or credits that might otherwise result in little to no tax being owed. For estates and trusts, Schedule I is added to Form 1041 to report adjustments and preferences that do not apply for regular tax purposes. This schedule is crucial for ensuring compliance and thoroughness in the tax reporting process for estates and trusts.

How to use the 2025 Schedule I (Form 1041) Alternative Minimum TaxEstates and Trusts

To effectively use the 2025 Schedule I (Form 1041), it is essential to understand the various adjustments and preferences that are applicable to estates and trusts under the alternative minimum tax rules. The process involves:

-

Gathering financial data: Collect all relevant financial information related to the estate or trust. This includes income, deductions, and credits that pertain to beneficiaries and fiduciaries.

-

Identifying AMT adjustments: Recognize specific income and deduction items that may require adjustment for AMT purposes, such as depreciation and tax-exempt interest.

-

Calculating AMT: Apply the alternative minimum tax rates and thresholds as prescribed in the tax code to determine if the estate or trust is liable for AMT.

-

Completing Schedule I: Enter all pertinent information into the form, making sure to accurately reflect the required adjustments and preferences.

Steps to complete the 2025 Schedule I (Form 1041) Alternative Minimum TaxEstates and Trusts

Filling out Schedule I involves several systematic steps:

-

Review the instructions: Thoroughly read the IRS instructions for Schedule I to understand specific requirements and calculations.

-

Enter basic information: Fill in identifying information such as the name, address, and EIN of the estate or trust.

-

Calculate adjustments: Determine any necessary tax adjustments. This includes adjustments for depreciation on property placed in service after 1986, as well as depletion and intangible drilling costs.

-

Compute AMT items: Calculate other items affecting AMT, such as net operating loss deductions and passive activity loss limitations.

-

Verify calculations: Double-check all computations to ensure accuracy before submission.

-

Integrate with Form 1041: Ensure results from Schedule I are accurately reflected in the broader Form 1041.

Important terms related to 2025 Schedule I (Form 1041) Alternative Minimum TaxEstates and Trusts

Several key terms are essential to understanding the nuances of Schedule I:

-

Alternative Minimum Tax (AMT): A parallel tax system that prevents high-income earners from avoiding tax liability through allowable deductions.

-

Estate: The total property, real and personal, owned by an individual before distribution through a trust or will.

-

Trust: A fiduciary relationship in which one party holds the title to property for the benefit of another.

-

Exemption Amount: An IRS-specified amount subtracted from AMT income when choosing between AMT and regular income tax rates.

-

Adjustments: Modifications required for specific taxpayer deductions or credits when calculating AMT.

IRS Guidelines

The IRS provides specific instructions for completing Schedule I that dictate how and when to file, acceptable deduction methods, and reporting requirements. Mandatory compliance with these guidelines ensures:

-

The proper identification of all income attributable to the estate or trust.

-

Detailed reporting of deductions and adjustments specific to AMT calculations.

-

Accurate submission timelines and the organization of applicable documentation for IRS scrutiny.

Filing Deadlines / Important Dates

Schedule I (Form 1041) must adhere to the specific filing deadlines associated with estate and trust tax returns:

-

Regular Filing Date: Returns, including Schedule I, are generally due by the 15th day of the fourth month following the close of the estate’s or trust’s taxable year.

-

Extension Considerations: Estates and trusts can apply for a six-month extension, shifting the deadline to October 15 by filing Form 7004.

Required Documents

To complete Schedule I accurately, several supportive documents must be prepared and reviewed:

-

Form 1041: The central filing form for estates and trusts, incorporating the AMT reported on Schedule I.

-

Income Statements: Documents detailing income received throughout the fiscal year.

-

Deduction Records: Comprehensive records of allowable deductions relevant to the estate or trust.

-

AMT Calculations: Calculations that reflect adjustments and preferences for AMT purposes.

Penalties for Non-Compliance

Failure to accurately file Schedule I can result in several penalties:

-

Late Filing Penalties: Levied on returns not filed by the due date, including extensions.

-

Accuracy-Related Penalties: Imposed for significant understatement of tax liability or significant errors in AMT calculations.

-

Interest Charges: Applied to any unpaid tax from the original due date of the return until the date of payment.