Definition and Purpose of Form 1120-L

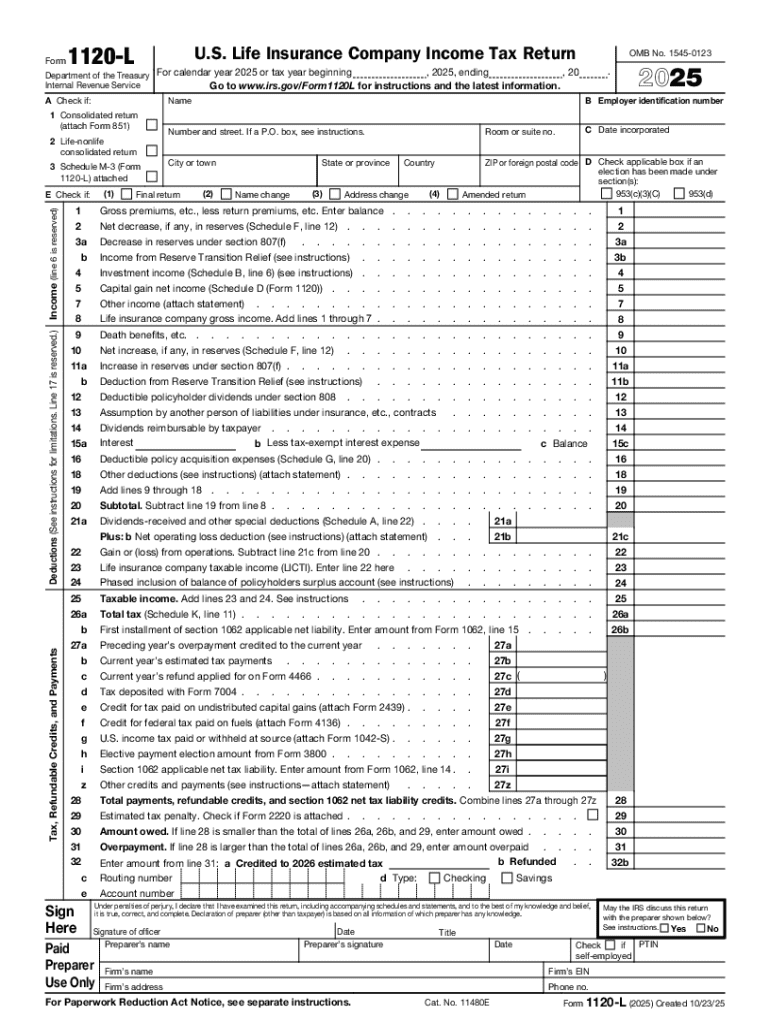

Form 1120-L, also known as the U.S. Life Insurance Company Income Tax Return, is a specialized tax form utilized by life insurance companies in the United States to report their income, gains, losses, deductions, and credits. This form enables such companies to calculate their federal tax liabilities accurately. Since the financial operations of life insurance entities have unique characteristics compared to other businesses, this form addresses those specific reporting requirements. By accommodating the nuances of income types and deductions inherent to the life insurance industry, Form 1120-L ensures that these companies meet their tax obligations correctly and efficiently.

Key Elements of Form 1120-L Instructions

Understanding the instructions for Form 1120-L is critical to completing the form accurately. Key elements include:

- Income and Deductions: Guidance on reporting various types of income such as premiums and investment earnings.

- Adjustments and Credits: Instructions for accounting adjustments and eligible tax credits.

- Special Provisions: Details on provisions specific to life insurance companies, including loss reserves and policyholder dividends.

- Compliance Requirements: Steps to ensure compliance with IRS regulations and to avoid penalties.

These instructions are essential for accurately reflecting the financial activities of a life insurance company and ensuring they adhere to federal tax regulations.

Steps to Complete Form 1120-L

-

Gather Financial Data: Start by collecting detailed financial statements and relevant documentation.

-

Follow the Income Reporting Guidelines: Accurately enter all income types as instructed, ensuring correct categorization of premiums and investment returns.

-

Deductions and Losses: Methodically apply deductions, understanding the specific limits and conditions expressed in the instructions.

-

Utilize Tax Credits: Identify and apply any eligible tax credits to reduce the company’s tax liability.

-

Review for Accuracy: Cross-check all entries against the instructions to ensure compliance with IRS standards.

-

Submit the Form: Decide between electronic submission or mailing, adhering to IRS deadlines to avoid penalties.

Completing Form 1120-L involves meticulous attention to detail, guided by the comprehensive instructions designed to reflect a life insurance company’s tax responsibilities.

IRS Guidelines and Compliance

The IRS provides specific guidelines that must be adhered to when completing Form 1120-L. These guidelines ensure the correct reporting of income, deductions, and credits. Compliance includes:

- Timely Submission: Respecting submission deadlines and using approved submission channels to avoid penalties.

- Accurate Reporting: Ensuring all entries comply with IRS definitions and reporting standards for life insurance companies.

- Record Keeping: Maintaining detailed records for verification purposes in case of an audit.

Understanding and applying these guidelines is critical for maintaining good standing with the IRS and avoiding potential legal and financial penalties.

Filing Deadlines and Important Dates

Form 1120-L must typically be filed by March 15th following the end of the tax year. For companies using a fiscal year-end, the form is due by the 15th day of the third month following the close of their tax year. If these dates fall on a weekend or holiday, the deadline shifts to the next business day. Extensions may be requested, but they must be submitted before the original filing deadline. Keeping track of these dates is crucial for ensuring full compliance with IRS requirements and preventing late filing penalties.

Required Documents for Form 1120-L

A complete submission of Form 1120-L requires various documents, including:

- Balance Sheets and Income Statements: Detailed financial documents covering the entire tax period.

- Premium Reports: Documentation of all received premiums.

- Investment Income Details: Records of income derived from investments.

- Expense Reports: Itemized list of expenses, including dividends, benefits, and commissions paid.

Having these documents organized and accessible is vital for accurate tax reporting and facilitating the process of form completion.

Penalties for Non-Compliance

Non-compliance with Form 1120-L filing requirements can result in significant penalties, including:

- Late Filing Penalties: Fines for submitting the form past the due date without an approved extension.

- Accuracy Penalties: Penalties for misreporting or omitting income, deductions, or credits.

- Interest Charges: Additional costs charged on overdue taxes as a result of incorrect or late submissions.

Adhering strictly to the filing instructions and deadlines is essential for avoiding such penalties and maintaining financial integrity.

Software Compatibility for Form Completion

Several software solutions support the completion and submission of Form 1120-L, offering compatibility and integration for tax professionals and insurance companies:

- TurboTax: Designed for businesses, although customized versions may be necessary.

- QuickBooks: Provides integrated support for managing financial data used in tax reporting.

- Specialized Tax Software: Solutions specifically tailored for corporate tax returns, often with comprehensive support features.

Selecting the right software can significantly streamline the tax filing process, reduce errors, and ensure that life insurance companies efficiently meet their tax obligations.