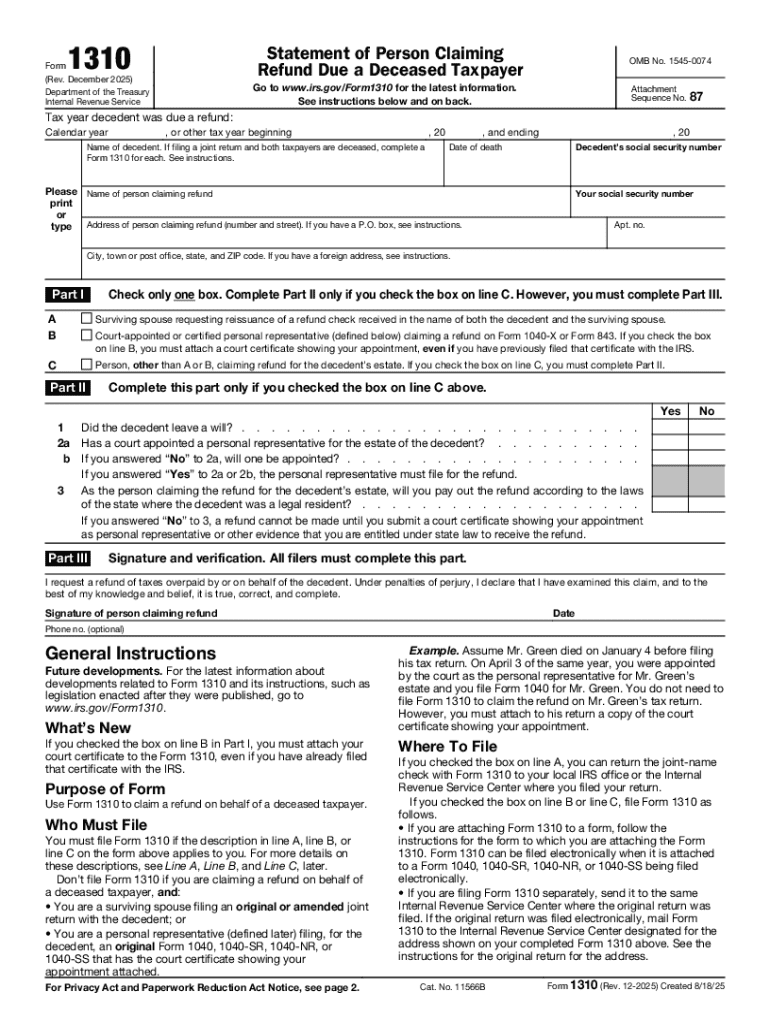

Definition and Purpose of Form 1310 (Rev December 2025)

Form 1310, formally known as the "Statement of Person Claiming Refund Due a Deceased Taxpayer," is a document used in the United States for tax filing purposes by individuals who are claiming a tax refund on behalf of a deceased taxpayer. Its primary purpose is to ensure that the rightful person receives the deceased individual's tax refund and that the IRS has a record of this transaction. This form is essential for maintaining the integrity and correctness of tax returns and refunds involving deceased taxpayers.

How to Use Form 1310 (Rev December 2025)

To utilize Form 1310 effectively, follow these steps:

-

Determine Eligibility: Ensure that you are the legitimate party eligible to file Form 1310. Generally, this includes executors, administrators, or personal representatives of the deceased's estate.

-

Collect Necessary Documents: Have essential documents ready, such as the death certificate and any legal documentation proving your relationship to the deceased or your authority to file on their behalf.

-

Complete the Form: Fill out all required sections, including personal information about the deceased taxpayer and your own details. Ensure accuracy to prevent delays or rejection.

-

Attach Supporting Documents: Depending on your relationship to the deceased, you may need to attach additional substantiating documents.

-

Submission: Submit Form 1310 along with the deceased taxpayer's final tax return. This can be done electronically or via mail, depending on your preference and the IRS’s requirements.

Steps to Complete Form 1310 (Rev December 2025)

Completing Form 1310 requires attention to detail. Follow these detailed steps:

-

Section 1: Personal Information

- Provide the deceased taxpayer’s name as it appears on their tax return.

- Include their Social Security Number (SSN).

- Enter your details, including name, address, and SSN.

-

Section 2: Reason for Claim

- Indicate your relationship to the deceased (e.g., spouse, executor).

-

Section 3: Certification

- Certify that you have provided true and accurate information and that you have the legal right to claim the refund.

-

Attachments

- Include a copy of the death certificate.

- Attach any legal documentation required for verification, such as a court-issued document identifying you as the executor or administrator.

-

Final Review and Submission

- Review for completeness and accuracy.

- Submit alongside the final tax return for the deceased taxpayer.

Key Elements of Form 1310

Form 1310 consists of several critical components:

- Claimant Information: Details about the individual or entity claiming the refund.

- Deceased Taxpayer Information: Data regarding the deceased taxpayer, including name and SSN.

- Claim Type: Specification of the relationship to the deceased and basis for the claim.

- Certification Section: Area where the filer certifies the correctness of the application.

- Attachments: Required documents that substantiate the claim.

Eligibility Criteria for Using Form 1310

To file Form 1310, you must meet specific eligibility guidelines:

- Relationship: You must be related to the deceased taxpayer or hold a legal position that authorizes you to file on their behalf.

- Documentation: You must provide the necessary documentation proving your legal standing.

- Condition of Deceased: Applicable only when claiming a refund for a taxpayer who has passed away before receiving their refund.

- Not Applicable for Joint Filers: When filing jointly and the surviving spouse is claiming the refund, Form 1310 is not needed.

Who Typically Uses Form 1310?

Form 1310 is primarily used by:

- Personal Representatives: Executors, administrators, or individuals assigned by a court to manage the deceased taxpayer’s final financial affairs.

- Surviving Family Members: Often a surviving spouse, child, or other immediate family member, particularly if they are legally entitled to the refund.

- Third Party: Individuals appointed by a legal will or a probate court to oversee estate matters.

IRS Guidelines for Filing Form 1310

The IRS provides specific guidelines for filing Form 1310:

- Filing Timeline: Should be filed as soon as possible after the taxpayer's death to ensure timely processing.

- Instructions Availability: The IRS offers comprehensive instructions accompanying the form to guide filers.

- Post-Submission: Once submitted, the IRS may request additional documents or clarification before issuing the refund.

Filing Deadlines and Important Dates

While there isn’t a strict deadline for Form 1310 itself:

- Adhere to the standard tax filing deadlines to ensure the refund is claimed during the correct tax year.

- Extensions may be applicable, but they should be requested formally, and the reasons should be documented.

Required Documents

When filing Form 1310, ensure that you include:

- Death Certificate: To validate the taxpayer’s status.

- Legal Proof of Role: Court documents or letters testamentary indicating your authority.

- Final Tax Return of Deceased: Also required along with Form 1310.

Form Submission Methods

Various methods exist for submitting Form 1310:

- Mail: Traditional submission by mailing paper forms to the IRS.

- Electronic Submission: When filed with the final tax return through electronic tax filing services.

- In-Person: Direct submission at an IRS office, though verification and acceptance will depend on local office policies.

Penalties for Non-Compliance

Failure to properly file Form 1310 can lead to:

- Delayed Refunds: Incorrect or incomplete filings may delay processing.

- Legal Repercussions: Filing falsely or providing incorrect information can lead to legal consequences.

- Denial of Claim: The IRS may reject the claim if required documentation is missing.

This comprehensive coverage of Form 1310 (Rev December 2025) offers insight into its usage, necessary documentation, and filing procedures, highlighting its importance for those handling the financial affairs of deceased taxpayers.