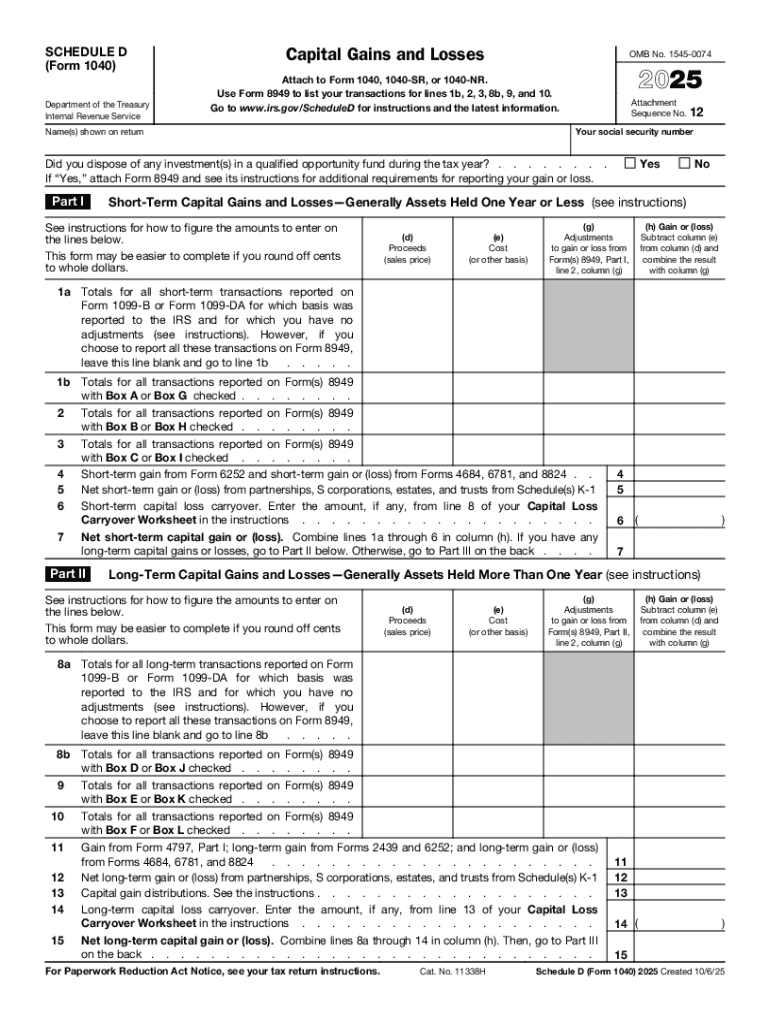

Definition and Purpose of Schedule D Form 1040

Schedule D is an integral component of the Form 1040 and focuses on reporting capital gains and losses. It is used by U.S. taxpayers to detail the total capital gains and losses realized from the sale or exchange of capital assets. By using Schedule D, individuals can demonstrate investment and asset disposition results while potentially minimizing tax liability through loss deductions.

Capital assets include stocks, bonds, and real estate, excluding a taxpayer's principal residence. Proper understanding and completion of Schedule D are crucial because capital gains can impact overall tax obligations. The form aids in calculating the net capital gain or loss, which subsequently affects the tax on other forms of income and assists in optimizing overall taxation strategy.

Steps to Complete Schedule D Form 1040

-

Gather Necessary Documents: Start by collecting all relevant documents, such as Form 1099-B, which provides details of transactions made over the year.

-

Fill Out Form 8949: Individual transactions should first be listed on Form 8949, detailing information such as description, date acquired, date sold, and resulting gain or loss for each asset.

-

Summarize Short-Term Transactions: Enter total short-term gains or losses from Form 8949 onto Part I of Schedule D. Remember, short-term gains are from assets held for less than one year.

-

Summarize Long-Term Transactions: Similarly, apply for long-term capital gains or losses from assets held for over a year onto Part II of Schedule D.

-

Calculate Net Gain or Loss: Deduct total losses from total gains, including both short-term and long-term, to compute the net capital gain or loss.

-

Special Considerations: Note any special situations such as gains from collectibles, which might be subject to different tax rates.

-

Transfer Totals to Form 1040: Finally, move the net gain or loss to line 15 of Form 1040, where it influences your total tax computation.

Who Typically Uses the Schedule D Form 1040

Primarily, individuals in the U.S. who have experienced capital gains or losses throughout the tax year utilize Schedule D. This form is essential for those involved in investments, including stocks, bonds, and real estate (other than primary residences). Taxpayers who partake in activities such as selling valuable artworks, collectibles, or other tangible assets should be familiar with completing this form.

Additionally, small business owners and self-employed individuals who derive income through selling shares or other capital assets significantly benefit from Schedule D. Recognizing who uses this form aids in understanding its relevance across various tax-paying scenarios, from the regular investor to business entities managing diverse asset portfolios.

Key Elements of Schedule D Form 1040

- Part I - Short-term Gains and Losses: For assets held for one year or less, listing each transaction and summing up gains and losses.

- Part II - Long-term Gains and Losses: For assets held more than one year, similar procedures apply, yet these often affect tax rates differently.

- Net Capital Gain or Loss: The overall calculation that influences taxation can result in offsetting other forms of income.

- Adjustments and Special Cases: Taxpayers may need to consider nuances such as non-business bad debts and gain on small business stock.

Understanding these segments is imperative for comprehensive reporting, as inaccuracies in any section can result in financial penalties or incorrect tax obligations.

IRS Guidelines for Schedule D

The IRS offers detailed instructions and guidelines for correctly preparing and understanding Schedule D. Compliance with these directions ensures accuracy in reporting capital transactions, ultimately influencing tax liability.

- Documentation: The IRS mandates adequate documentation to support reported figures, primarily ensuring precision on Form 8949 before transference to Schedule D.

- Tax Rates: Be mindful of the tax rates applied to short-term vs. long-term gains, understanding that long-term gains often benefit from reduced rates.

- Loss Caps and Carryovers: The IRS stipulates limits on losses that can be deducted and provides for the carryover of excess losses to subsequent years.

Adhering to IRS regulations, American taxpayers will decrease the risk of audits or fines due to misreporting.

Filing Deadlines and Important Dates

The standard deadline for filing Form 1040, including Schedule D, coincides with America's Tax Day, generally around April 15th each year. Taxpayers should ensure timely submission to evade penalties and interest charges attributed to late filings. If an extension is necessary, the extended deadline usually falls around October 15th, offering more time for detailed reviews and updates on submitted information.

Awareness and adherence to these deadlines are indispensable, as missing them can lead to financial fines and a stressful tax management experience.

Examples of Using Schedule D

- Investor Scenario: John, a portfolio manager, sold several stocks, experiencing both gains and losses. Completing Schedule D accurately allows him to report $5,000 in short-term gains offset by $3,000 in losses.

- Real Estate Disposition: Sarah, a property investor, sold a rental home resulting in substantial long-term capital gains. As these gains qualify for lower tax rates, arranging them on Schedule D effectively reduces her overall tax burden.

- Art Sales: Mark, an artist and collector, sold sculptures gaining $10,000. These gains, noted on Schedule D, are subject to specific collectible tax rates, providing a nuanced tax application on overall earnings.

By leveraging practicality in examples, Schedule D's utility across variances is clear, noting its critical role in financial management for asset buyers and sellers.

Required Documents for Schedule D

- Form 1099-B: For tracking sales of securities and commodities.

- Brokerage Statements: Detailed reports on trades for accuracy.

- Form 8949: To list and classify specific transactions and adjustments appropriately.

Keeping organized records aids in providing accurate, reliable information for each capital transaction inquirers submit to the IRS. With these documents, taxpayers can ensure compliance, reduce discrepancies, and foster accurate financial documentation.