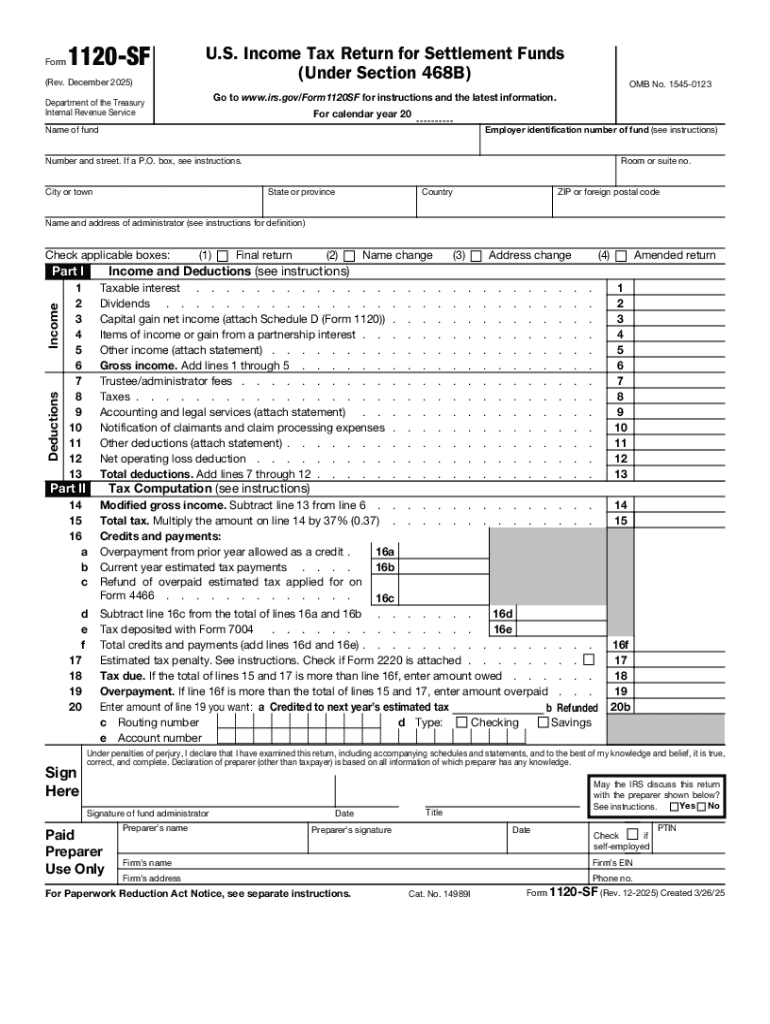

Definition & Purpose of Form 1120-SF

Form 1120-SF is the U.S. Income Tax Return for Settlement Funds, specifically used for qualified settlement funds (QSFs) and disputed ownership funds (DOFs) under Section 468B of the Internal Revenue Code. The form is designed to report the income, gains, and losses of settlement funds. It ensures compliance with tax obligations related to these funds, which are often established to resolve legal claims. Key features include reporting income from investments and distributions to claimants.

How to Obtain Form 1120-SF

Form 1120-SF can be accessed and downloaded directly from the IRS website. The form is available in PDF format and can be printed for manual completion. For those using tax preparation software, the form is typically integrated within these systems and can be filled out and filed electronically. Furthermore, if additional assistance is needed, tax professionals can provide the form or guide taxpayers in accessing it.

Steps to Complete Form 1120-SF

Completing Form 1120-SF involves several steps:

- Identify Basic Information:

- Fill out the name, address, and employer identification number (EIN) of the settlement fund.

- Report Income and Deductions:

- Include all income sources such as interest, dividends, and capital gains. Deductions for administrative expenses and distributions to claimants should also be detailed.

- Tax Calculation:

- Calculate tax due based on the fund’s taxable income using the tax rates provided in the form’s instructions.

- Sign the Form:

- An authorized trustee or administrator must sign the completed form to certify accuracy and compliance.

Who Typically Uses Form 1120-SF

Legal entities that use Form 1120-SF often include trustees or administrators overseeing settlement funds established from lawsuits or legal settlements. These might involve class-action lawsuits, mass tort claims, or disputed ownership situations where funds are held until a resolution is reached. Financial and legal advisors involved with fund administration or management may also play a role in the form’s preparation and filing.

Key Elements of Form 1120-SF

Several crucial elements make up Form 1120-SF:

- Identification Information: Details about the fund itself, such as name and EIN.

- Gross Income Summary: A report of all income generated by the fund, including investment returns.

- Deduction and Distribution Details: Itemized deductions and distributions to recipients of the fund.

- Tax Computation: Specific sections which guide on calculating the tax liability.

- Signature and Date: Certification requirement by authorized personnel.

IRS Guidelines for Form 1120-SF

The IRS provides comprehensive instructions for filling out Form 1120-SF, which outline proper reporting practices and compliance requirements. These guidelines cover scenarios such as identifying taxable income, allowable deductions, and the correct application of tax rates. They also detail filing deadlines and procedures for payment, extensions, and amendments.

Filing Deadlines and Important Dates

Form 1120-SF must be filed annually. The typical deadline for filing is the 15th day of the third month following the end of the fund’s tax year. For example, a fund that follows the calendar year must file by March 15. Extensions of time to file can be requested, usually by submitting IRS Form 7004 before the original due date.

Penalties for Non-Compliance

Failure to submit Form 1120-SF on time or inaccurately can result in penalties. Common penalties include:

- Late Filing Penalty: Charged when the form is not filed by the due date.

- Accuracy-Related Penalty: Applied if there are substantial understatements of tax due to negligence or disregard of rules.

- Failure to Pay Penalty: Imposed on taxable amounts not paid by the due date.

Eligibility Criteria for Using Form 1120-SF

Eligibility to file Form 1120-SF generally applies to qualified settlement funds that satisfy specific criteria under Section 468B of the Internal Revenue Code. These include funds established by court order to address large settlement claims, typically involving multiple claimants or complex legal disputes. Criteria for disputed ownership funds require cases where ownership of assets or funds is contested.