Understanding Form 1041 Schedule D for Estates and Trusts

Form 1041 Schedule D is a critical tax document used by estates and trusts to report capital gains and losses. This form is part of the income tax return for estates and trusts, commonly referred to as Form 1041. Properly completing Schedule D is crucial for accurately calculating the taxable income as it pertains to capital transactions.

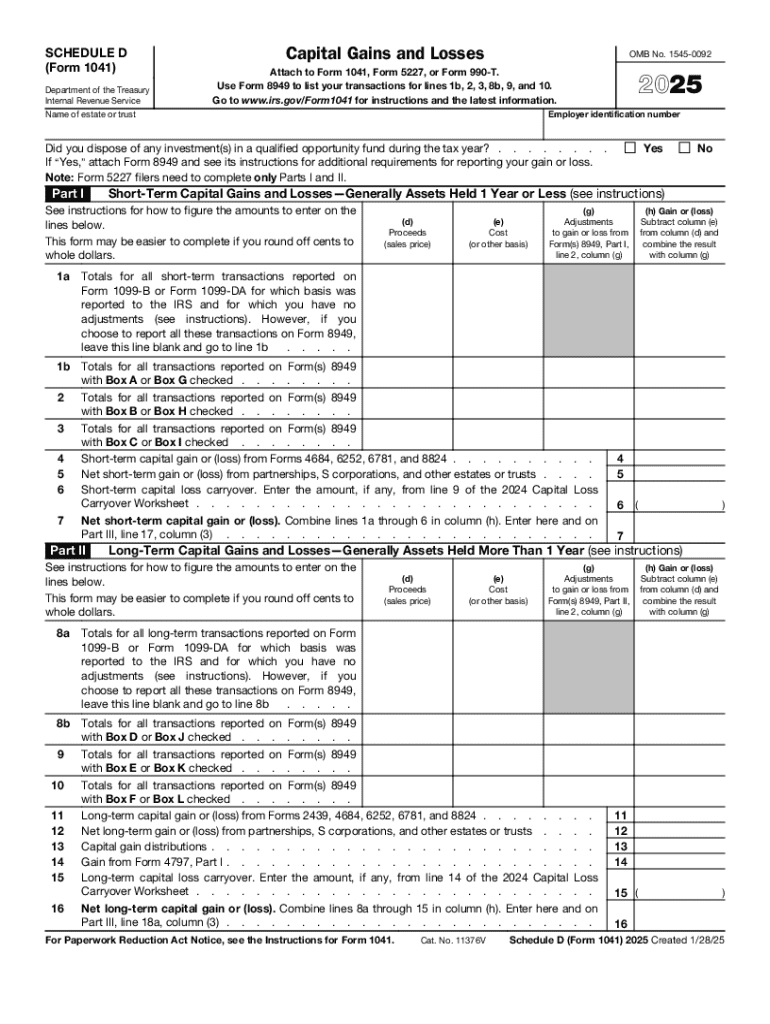

Key Elements of Form 1041 Schedule D

-

Capital Gains and Losses: The primary function of Schedule D is to report the capital gains and losses incurred by the estate or trust during the tax year. These include transactions involving stocks, bonds, mutual funds, and real estate.

-

Short-Term and Long-Term Transactions: Schedule D distinguishes between short-term and long-term transactions. Short-term relates to assets held for one year or less, while long-term applies to those held for more than one year.

-

Net Gain or Loss Calculation: The form guides the process of summing up gains and losses, offsetting them against each other, and arriving at a net capital gain or loss. This net figure is then reported on Form 1041.

Steps to Complete Form 1041 Schedule D

-

Gather Required Information: Collect all documentation related to capital transactions, such as purchase and sale records, dates, and amounts. This includes brokerage statements and transaction receipts.

-

Enter Transaction Details: Populate Part I of Schedule D with short-term capital transactions and Part II with long-term transactions. Include details such as description, date acquired, date sold, sales price, and cost basis.

-

Calculate Gains and Losses: Within each section, calculate the gain or loss for each transaction by subtracting the cost basis from the sales price.

-

Summarize Totals: Total the gains and losses separately for short-term and long-term transactions. Enter these in the appropriate sections of the form.

-

Determine Net Gain or Loss: Combine the short-term and long-term figures to determine the net capital gain or loss, which will be reported on Form 1041.

IRS Guidelines for Schedule D

The IRS provides detailed instructions for completing Schedule D, emphasizing the importance of accuracy in reporting capital transactions. Incorrect reporting can lead to penalties. It's essential to review IRS instructions, which include defining which transactions are reportable and clarifying calculation methods.

-

Form 8949 Attachment: If specific types of transactions require additional detail, use Form 8949 to provide a comprehensive list, which then feeds into Schedule D.

-

Guidelines on Holding Periods: IRS rules specify the criteria for short-term vs. long-term classifications, essential for correct tax computation.

Penalties for Non-Compliance

Failing to accurately complete and submit Schedule D with Form 1041 can result in severe penalties, including fines and interest on unpaid taxes. Misreporting capital gains can trigger IRS audits, extending financial and legal scrutiny on the estate or trust.

Taxpayer Scenarios and Examples

Scenario 1: Estate Liquidating Stock Holdings

An estate sells a portfolio of stocks inherited from the decedent. Schedule D will report these sales, factoring in the step-up in basis common for inherited assets, potentially minimizing taxation.

Scenario 2: Trust with Real Estate Earnings

A trust sells a rental property. Schedule D would reflect the gain or loss, after adjusting for improvements and depreciation, contributing to the trust's annual tax liability calculation.

State-Specific Rules

While Schedule D pertains to federal tax reporting, it's essential to consult state tax laws, as they may impose additional requirements or variations in treatment of capital gains.

Software Compatibility

Filing tools such as TurboTax and QuickBooks are compatible with Form 1041 Schedule D, streamlining the process by automating calculations and ensuring compliance through up-to-date tax law integration.

Filing Deadlines

Form 1041 and the associated Schedule D must be filed by the 15th day of the fourth month following the close of the estate or trust's tax year, typically April 15 for calendar year filers. Extensions may be requested if additional time is needed to gather information or prepare the return.