Definition & Meaning

Form 8606, also known as the "Nondeductible IRAs" form, is used by individuals in the U.S. to report certain types of IRA contributions, conversions, and distributions. Specifically, it addresses nondeductible contributions to traditional IRAs, Roth IRA conversions, and distributions from IRAs when nondeductible contributions have been made. It ensures that individuals do not pay taxes twice on the same income when they eventually take distributions from their IRAs.

Why Should You File Two Separate Form 8606, One for You and One for Your Spouse?

If you and your spouse both have IRAs that include nondeductible contributions or have been involved in Roth conversions, you will need to file separate Form 8606 for each of you. The IRS requires this separation to maintain individual accounting for each taxpayer's IRA contributions and conversions to accurately track their individual tax obligations. Filing separately ensures clarity and compliance with IRS guidelines and prevents any tax discrepancies.

Steps to Complete Form 8606

-

Gather Your Documents: Ensure you have all relevant financial documents, including your IRA contribution records, Form 1099-R for distributions, and records of any conversions made.

-

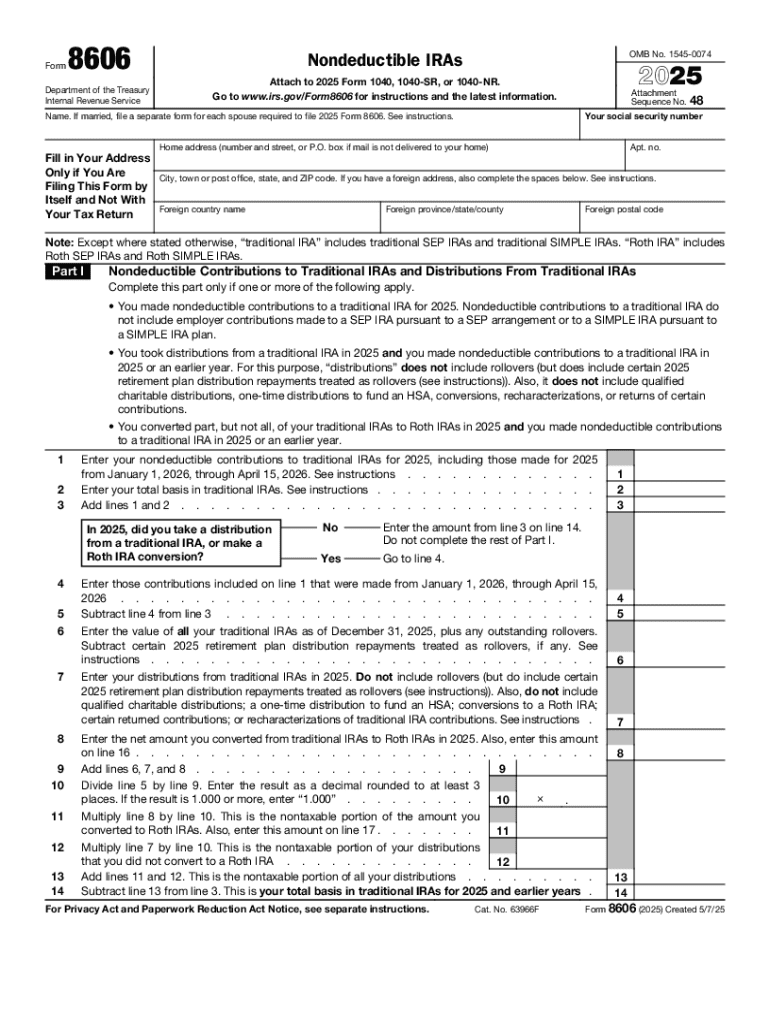

Section I: Begin by filling out the personal information section. This includes your name and social security number. Ensure all information matches your other tax documents to avoid processing issues.

-

Section II - Nondeductible Contributions: Complete this section if you made any nondeductible contributions to your IRA. Input the total of nondeductible contributions made for the tax year and carry the cumulative total from previous years.

-

Section III - Roth IRA Conversions: If applicable, report any conversions to a Roth IRA here. Specify the amount converted and calculate the taxable portion, if any.

-

Section IV - Distributions: If you took any distributions, complete this part. Specify the total distributions and calculate the taxable amount based on the nondeductible portion of your contributions.

-

Review & Submit: Double-check your calculations and information for errors. Attach Form 8606 to your tax return and submit it by the IRS filing deadline.

IRS Guidelines

The IRS provides specific instructions for completing Form 8606, which outlines who must file and which portions of the form apply to different scenarios. Ensure you have the updated guidelines for the current tax year, as rules regarding IRAs and contributions can change.

Filing Deadlines / Important Dates

Form 8606 should be filed along with your individual tax return, typically by the April 15 deadline. If you file for an extension on your tax return, Form 8606 should be filed by the extended deadline, often October 15. Timeliness ensures compliance and helps avoid penalties.

Penalties for Non-Compliance

Failing to file Form 8606 when required can result in penalties. The IRS imposes a $50 fine for not filing the form, and additional penalties can apply if understated taxes result from unreported nondeductible contributions. Always ensure accurate and timely filing to avoid any fines.

Digital vs. Paper Version

Both digital and paper versions of Form 8606 are accepted by the IRS. Tax software like TurboTax and QuickBooks provides digital submission options, which streamline the process and reduce manual errors. Opt for digital filing if possible, for easier record-keeping and processing.

Eligibility Criteria

You must file Form 8606 if you have made nondeductible contributions to a traditional IRA, converted traditional, SEP, or SIMPLE IRAs to Roth IRAs, or have taken distributions from a traditional, SEP, or SIMPLE IRA when nondeductible contributions exist. Understanding these criteria helps determine when filing is necessary.

Software Compatibility (TurboTax, QuickBooks, etc.)

Common tax software platforms, such as TurboTax and QuickBooks, support Form 8606. These tools guide users through the form's completion with built-in calculations and error checks, reducing the risk of mistakes. Ensure your software is updated for the current tax year to utilize the latest tax laws.