Definition & Meaning

Form W-7-COA (Rev 8-2025) is a Certificate of Accuracy used by the IRS to ensure the accuracy of information provided for obtaining an Individual Taxpayer Identification Number (ITIN). This form is a critical part of the tax process for those who require an ITIN but are not eligible for a Social Security Number (SSN). It verifies that the information submitted is true and accurate, helping to maintain the integrity of tax records.

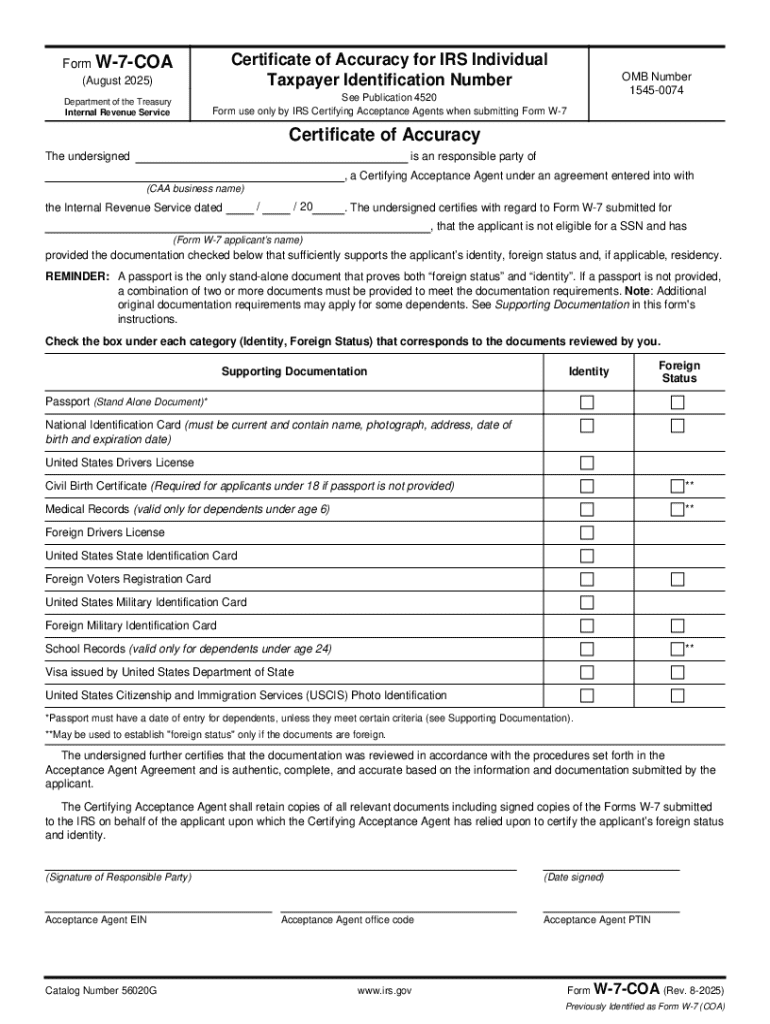

Key Elements of the Form

- Personal Information: Requires the applicant's name, address, and other identifying details.

- Document Verification: Includes verification from a Certifying Acceptance Agent or IRS official to affirm the validity of the applicant's documentation.

- Signature Requirements: Provides sections for signatures from both the applicant and the certifying professional, ensuring accountability and responsibility.

How to Obtain the Form W-7-COA (Rev 8-2025)

The form can be obtained directly from the IRS website or by visiting local IRS offices. It's important for applicants to use the latest version to ensure compliance with current IRS regulations. Additionally, those working with a Certifying Acceptance Agent can receive guidance and assistance in obtaining and completing the form.

Steps to Complete the Form

- Gather Required Documentation: Collect all necessary documents, including identification and proof of foreign status.

- Complete Personal Information Sections: Accurately fill out name, address, and other basic information.

- Coordination with Acceptance Agent: Work with a Certifying Acceptance Agent to fill out the verification section.

- Review and Sign: Check the form for any discrepancies before signing and having the acceptance agent complete their portion.

Importance of Form W-7-COA (Rev 8-2025)

Using the Form W-7-COA is crucial for anyone needing an ITIN, as it ensures that their application is based on accurate and verified information. It helps prevent fraudulent use of taxpayer identification numbers and facilitates proper tax processing for individuals without an SSN. This form maintains the credibility and security of the taxpayer identification system.

Examples of Using the Form

- Foreign Nationals: Individuals working in the U.S. under a visa who are required to file taxes but do not qualify for an SSN.

- Dependents: Non-U.S. resident spouses and dependents who need an ITIN for tax return purposes.

- Students: International students in the U.S. who need to report taxable income.

Legal Use of the Form W-7-COA (Rev 8-2025)

The legal framework mandates that the Form W-7-COA is used to certify the accuracy and validity of documents when applying for an ITIN. The IRS requires that applicants provide a certified true copy of original documents to ensure that their tax identification is processed correctly. Using this form improperly can lead to denied applications or penalties for fraudulent submissions.

Penalties for Non-Compliance

Non-compliance with the submission of accurate and verified forms may result in the rejection of the ITIN application, penalties, or further investigation by the IRS.

IRS Guidelines

The IRS provides detailed guidelines on the acceptable forms of identification and documentation needed to process an ITIN application. They define the role of Certifying Acceptance Agents and outline the necessary steps applicants must follow to ensure compliance with federal tax laws.

Required Documents

- Valid Passport: Often suffices on its own for proof of identity and foreign status.

- Other Identifications: May include a national identification card, military ID, or U.S. visa.

Form Submission Methods (Online / Mail / In-Person)

Form W-7-COA can be submitted along with Form W-7 application through various channels:

- Mail: Sending the form and supporting documents to the IRS ITIN Operation Center.

- In-Person: Submission through an Acceptance Agent or IRS Taxpayer Assistance Center.

- Online Platforms: Some IRS-certified agents might offer digital submission processes for convenience.

Digital vs. Paper Version

While the primary method for handling sensitive identification documentation remains paper-based due to the need for certified copies, digital platforms may offer initial application submission, with follow-up paper documentation.

Examples of Specific Use-Case Scenarios

Taxpayer Scenarios

- Self-Employed Individuals: Self-employed non-residents receiving income from U.S.-based clients.

- Retired Individuals: Receiving pension or social security benefits requiring taxation but without SSN eligibility.

- Students and Academics: Required to file tax returns on stipends or scholarships received.

State-by-State Differences

Though Form W-7-COA is a federal form, some states may have additional requirements or acceptance processes, particularly in cases where state tax implications are involved for non-residents working within the U.S. It's advisable to consult state resources to ensure compliance with local tax laws.

Who Issues the Form

The IRS is the issuing body for Form W-7-COA. Certifying Acceptance Agents, who are approved by the IRS, can verify supporting documents and help applicants complete the form as part of the ITIN application process.

Ensuring that this form is completed accurately and in a timely manner is vital for individuals needing to secure a taxpayer identification number without qualifying for an SSN. The process involves careful attention to detail and compliance with IRS protocols to avoid rejections or delays.