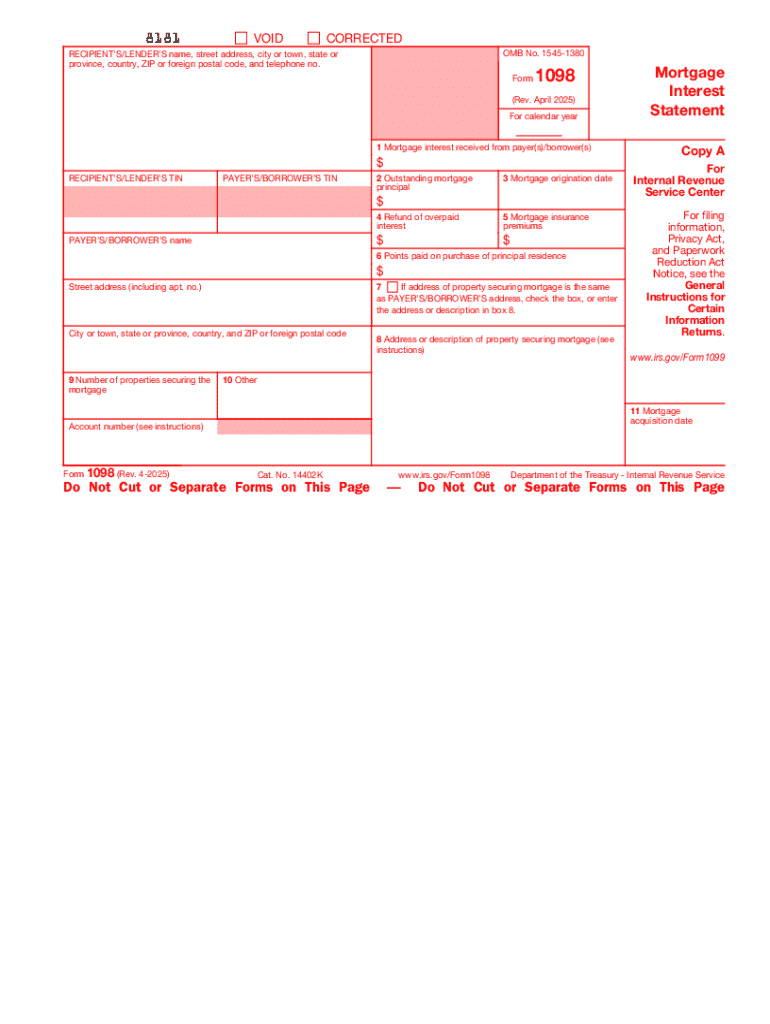

Definition and Meaning of Form 1098

Form 1098, commonly referred to as the Mortgage Interest Statement, is used by mortgage lenders to report the amount of mortgage interest and related expenses paid by a borrower during the tax year. This form is critical for taxpayers, as it helps them claim deductions on their federal income tax returns. Typically, entities that receive at least $600 in mortgage interest from a borrower during the year issue this form.

Key Components of Form 1098:

- Mortgage Interest Paid: The primary component documented on Form 1098.

- Outstanding Mortgage Principal: Reflects the remaining balance on the loan.

- Mortgage Insurance Premiums: If applicable, these premiums are also reported.

Understanding these components is crucial for homeowners looking to maximize their tax deductions.

How to Use Form 1098

Mortgage interest payments reported on Form 1098 can be used to claim deductions on your individual federal tax return, providing a potential tax benefit. Borrowers typically incorporate the reported amount from Form 1098 when filing their Schedule A form if they choose to itemize deductions.

Steps for Using Form 1098 on Your Tax Return:

- Review the Form: Ensure all information, including interest paid, is accurate.

- Determine Eligibility: Decide whether to itemize deductions or take the standard deduction.

- Report on Schedule A: Include the mortgage interest in line with IRS guidelines for Schedule A.

- Retain Copies: Keep the original Form 1098 for your records along with your tax return copy.

Steps to Complete Form 1098

Though the mortgage lender completes Form 1098, understanding the completion process can aid borrowers in verifying its accuracy.

Completion Process by Lenders:

- Collection of Data: Lenders gather all pertinent mortgage information from their records.

- Accurate Reporting: Ensure all amounts, especially mortgage interest paid, are accurate.

- Form Submission: Provide copies to both the borrower and the IRS.

Who Issues Form 1098

Entities providing mortgage loans or receiving mortgage interest payments throughout the tax year are responsible for issuing Form 1098. This typically involves banks, credit unions, and other professional lenders.

Responsibilities of Issuers:

- Accurate Documentation: Ensure all figures are correct. Errors can lead to discrepancies during tax filing.

- Timely Distribution: Forms should be sent to borrowers by January 31 and submitted to the IRS by February 28 if filing on paper or March 31 if filing electronically.

IRS Guidelines for Form 1098

The IRS provides specific instructions concerning the requirements for filing Form 1098. These guidelines dictate what constitutes reportable interest payments and outline compliance requirements.

Important Considerations:

- Eligibility: Lenders meeting the $600 threshold for interest paid must issue the form.

- Electronic Filing: Encouraged by the IRS for faster processing.

Penalties for Non-Compliance

Failing to issue or properly file Form 1098 can result in penalties levied against the mortgage lender.

Potential Risks:

- Monetary Penalties: Fines for failing to file or late submissions.

- Increased Scrutiny: Non-compliance may lead to enhanced audits or reviews from the IRS.

Filing Deadlines and Important Dates

Timely submission of Form 1098 is critical to ensure compliance with IRS regulations.

General Timeline:

- January 31: Due date for lenders to furnish Form 1098 to borrowers.

- February 28: Deadline for submission to the IRS if filing in paper format.

- March 31: Deadline for electronic submissions to the IRS.

Examples of Using Form 1098

Understanding how Form 1098 applies in real-world situations can help borrowers accurately utilize the form on their tax returns.

Practical Scenarios:

- Homeowners: Claim mortgage interest deductions by utilizing information from Form 1098.

- Investors: Use Form 1098 to track mortgage expenses on investment properties for potential tax benefits.

By thoroughly understanding the components and processes related to Form 1098, taxpayers can ensure accuracy in their filings and potentially benefit from applicable deductions.