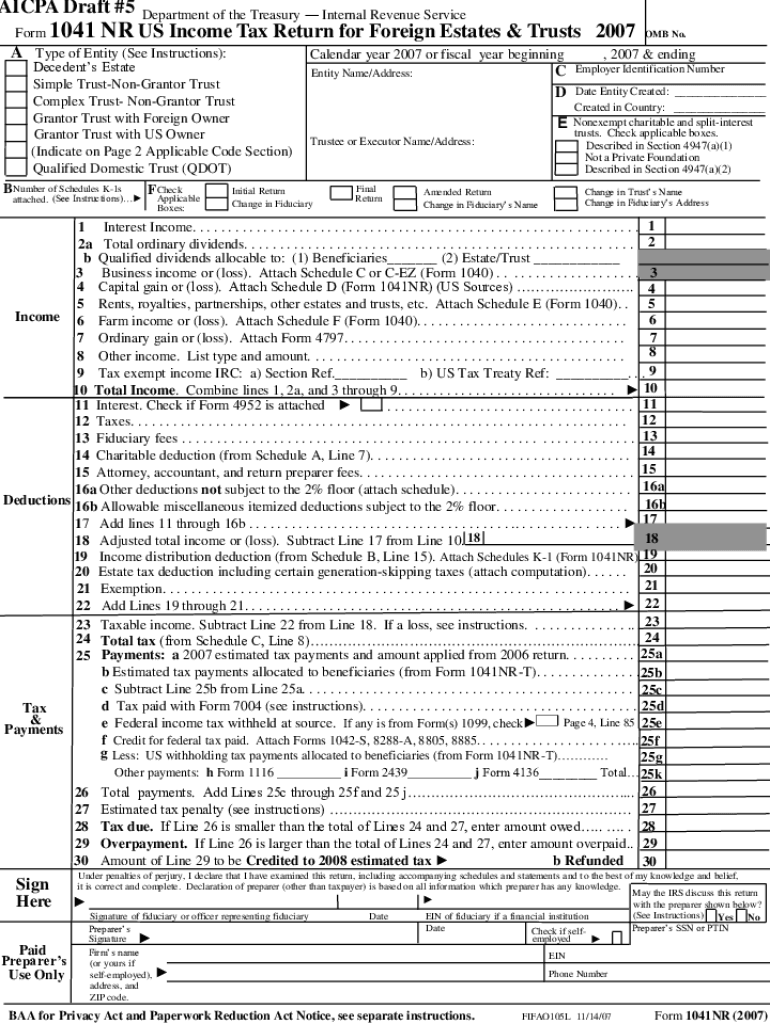

Definition and Meaning

The Form 1041-NR Draft #5 US Income Tax Return for Foreign Estates - AICPA refers to a draft version specifically designed for foreign estates and trusts operating under US tax jurisdiction. Unlike domestic estates, foreign estates are defined as entities not primarily managed or controlled in the United States. This form is crucial for such entities to comply with US tax obligations, documenting income and tax responsibilities accurately. The term "AICPA" in the form indicates its alignment with the standards set by the American Institute of Certified Public Accountants, ensuring adherence to the accounting industry's best practices.

- Specifically targets foreign estates and trusts.

- Aligns with AICPA guidelines for accounting accuracy and transparency.

- Essential for compliance with US tax regulations.

How to Use Form 1041-NR Draft #5

To correctly utilize Form 1041-NR, foreign estates must follow a series of detailed steps. Understanding this process ensures accurate tax filing and minimizes errors.

- Obtain the Draft Form: Access the form through trusted sources ensuring it reflects the latest version.

- Gather Necessary Information: Include details such as the estate's gross income, deductions, and credits.

- Complete Each Section: Follow instructions for each part, ensuring accurate calculations.

- Verification and Review: Cross-check all entries for correctness before submission.

- Consult a Tax Professional: If needed, consult with a CPA familiar with foreign estates and trust taxation.

Steps to Complete Form 1041-NR Draft #5

Completing Form 1041-NR requires meticulous attention to detail. Below are outlined steps to help guide through this process efficiently:

- Identify Filing Status: Determine the estate's status as foreign to ascertain the correct form usage.

- Report Income: Accurately report all income attributed to the estate, using the form's designated sections.

- Determine Deductions: Carefully compute eligible deductions that the estate may claim, such as administrative expenses.

- Calculate Taxable Income: Subtract allowable deductions from gross income to find taxable income.

- Compute Tax Liability: Use appropriate tax rates for foreign entities to compute total tax liability.

- Review and Finalize: Ensure the form is entirely filled without errors, authorized signatures are present, and all necessary forms are attached.

Essential Sections in Form

- Part I - Income: Records gross income from various sources.

- Part II - Deductions: Lists allowable deductions.

- Part III - Tax and Payments: Calculates the tax due or any payments made.

Important Terms Related to Form 1041-NR Draft #5

Understanding the terminology related to Form 1041-NR is imperative for accurate completion and compliance:

- Foreign Estate: An estate where control and administration are not primarily executed within the US.

- Gross Income: Total income received before deductions.

- Deductions: Allowed subtractions from gross income for specific expenses.

- Tax Liability: The total amount of tax owed to the IRS.

Filing Deadlines and Important Dates

Adherence to filing deadlines is crucial to avoid penalties. For the 1041-NR, the key dates include:

- Standard Deadline: Generally, the 15th day of the 4th month following the end of the estate's tax year.

- Extension Requests: Deadlines may be extended under specific circumstances through approved IRS procedures.

Penalties for Missing Deadlines

- Failure-to-File Penalty: Imposed for late filing without a granted extension.

- Interest Charges: Calculated on unpaid taxes from the original filing date.

Required Documents for Form Submission

Several documents are necessary when preparing Form 1041-NR:

- Income Statements: Reflecting all income earned by the estate.

- Deduction Records: Documentation for all claimed deductions.

- Previous Tax Returns: Previous filings, if applicable, for reference.

- Supporting Schedules: Any additional forms supporting the tax return.

Who Issues the Form

The Form 1041-NR is issued by the Internal Revenue Service (IRS), the federal agency responsible for tax collection and law enforcement.

- Purpose: Ensures foreign estates comply with US taxation laws.

- Periodic Updates: The IRS updates forms periodically to align with regulatory changes.

Digital vs. Paper Version

The choice between digital and traditional filing methods depends on the preferences of the estate administrators:

- Digital Filing: Provides convenience, quicker processing times, and reduces the risk of errors.

- Paper Filing: Traditional method, preferred by some for a tangible paper trail.

Software Compatibility

- Tax Software: Form 1041-NR is compatible with software like TurboTax and QuickBooks, streamlining the filing process.

IRS Guidelines and Compliance

The IRS provides extensive guidelines to assist foreign estates in accurately completing Form 1041-NR, ensuring compliance with federal tax laws and regulations.

- Guidance Documents: Available on the IRS website.

- Regular Updates: Reflect changes in taxation law, which foreign estates need to remain up-to-date with for accurate filing.