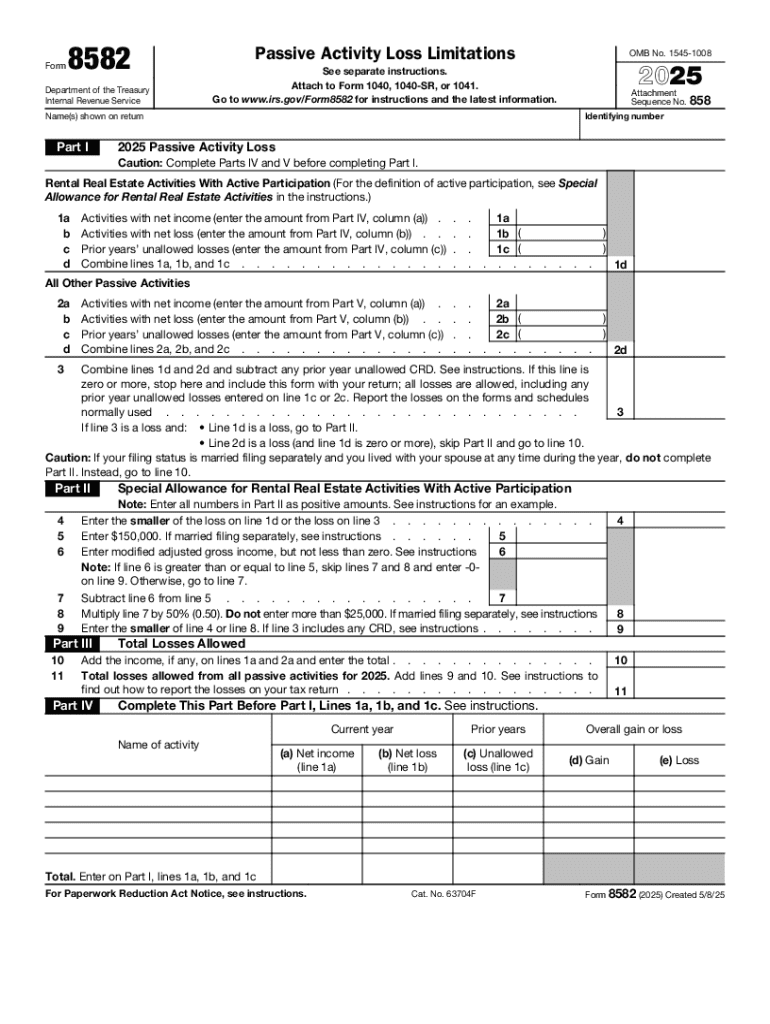

Definition and Purpose of Form 8582 - Passive Activity Loss Limitations

Form 8582, known fully as "Passive Activity Loss Limitations," is a document issued by the Department of the Treasury, Internal Revenue Service. This form is primarily used by individuals who need to report passive activity losses that they are not able to deduct due to limitations set by the IRS. Passive activities typically include rental activities or businesses in which one does not materially participate. The purpose of Form 8582 is to calculate the amount of passive activity loss (PAL) that can be applied against active income in a given tax year.

Key Elements

- Passive Activity Credits: These are credits passed through to individuals from trades, businesses, or rental activities. Form 8582 aids in determining the extent to which these credits can be utilized.

- Material Participation: It differentiates between activities a taxpayer materially participates in and those that are considered passive.

- At-Risk Rules: These rules are applied to ensure that losses are only deductible to the extent of involvement in the activity.

How to Use Desktop: Form 8582 - Passive Activity Loss Limitations

To accurately use Form 8582, it is essential for taxpayers to first collect information on all income and losses from passive activities. This data serves as input while calculating the permissible deduction:

- Collect Information: Gather all income, deductions, credits, and activity participation details from the tax year.

- Input Data: Carefully enter collected information into the form, ensuring that each category is completed with precise details.

- Calculate Allowable Loss: Use the worksheets provided in the form to determine the passive activity loss that can be deducted.

Step-by-Step Instructions

- Step 1: Identify passive income-generating activities and collect respective financial statements.

- Step 2: Utilize IRS-provided worksheets to calculate total passive losses.

- Step 3: Enter the summary figures from these calculations into the appropriate lines on Form 8582.

How to Obtain Form 8582

To obtain a copy of Form 8582:

- Visit IRS Website: Navigate to the official website of the IRS where the form can be downloaded.

- Tax Preparation Software: Most tax preparation software includes Form 8582 within their document library.

- Physical Copies: Taxpayers can request a physical copy from an IRS office or authorized entity.

Steps to Complete the Form

Filling out Form 8582 involves a systematic approach to document completion. Taxpayers should perform the following:

- Fill in Personal Information: Complete the top section with personal and contact details.

- Passive Loss Information: Accurately input data from passive activities.

- Validation and Review: Double-check each section to ensure accuracy and compliance with IRS guidelines.

Importance of Form 8582

Using Form 8582 is essential for individuals with passive income:

- Compliance: Fulfilling legal obligations by reporting passive activity losses.

- Tax Benefits: Accurately calculating how much of these losses can be used to offset taxable income.

- Financial Planning: Understanding financial exposure and potential refunds that can result from passive activity losses.

Typical Users of Form 8582

The form is commonly used by:

- Real Estate Investors: Those earning through rental properties.

- Limited Partners: Individuals in partnerships that do not engage actively in its operations.

- Small Business Stakeholders: Passive investors in corporations or LLCs.

IRS Guidelines

The IRS provides strict guidelines on how to handle the application of passive activity losses. Adhering to these guidelines is crucial:

- Loss Limitations: Only losses up to the extent of passive income can be deducted.

- Carryforward Policies: Excess losses that cannot be deducted can be carried forward to future tax years.

Filing Deadlines and Important Dates

- Annual Submission: Typically filed with the taxpayer's annual return by April 15th.

- Extensions: Applies if a taxpayer has filed for an extension on their overall tax returns.

Examples and Scenarios

Understanding real-life applications of Form 8582:

- Example 1: A taxpayer owns three rental properties, one of which incurs a loss. Calculate how these losses are allocated against income.

- Example 2: Exploring scenarios where an individual has a partial interest in a syndication yielding passive losses.

Required Documents

Before beginning with Form 8582, ensure you have:

- Income Statements: All passive activity financial records.

- Previous Year's Tax Returns: Useful for carryforward calculations.

- Legal Documents: Entity formation or partnership agreements establishing activity type.

Submission Methods

- Online Filing: Submit electronically with federal tax return via e-file platforms.

- Mail: Send a printed form along with the physical copy of the tax return to the IRS.

- In-Person: Submit directly at designated IRS locations if necessary.