Definition and Purpose of IRS Form 5227

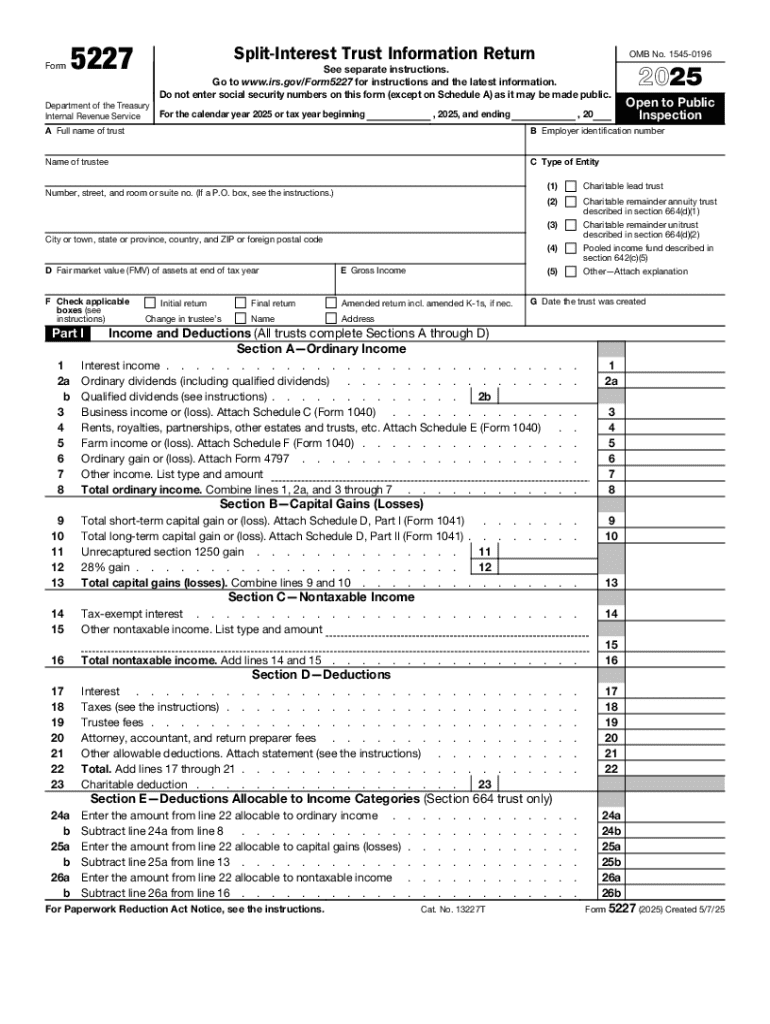

IRS Form 5227, titled "Split-Interest Trust Information Return," is utilized by certain trusts to report financial activities, primarily split-interest trusts that have significant charitable interests. The main purpose of this form is to report the financial activities and operations of these trusts to the Internal Revenue Service (IRS) and ensure compliance with charitable trust obligations. Examples of split-interest trusts include charitable remainder annuity trusts, charitable remainder unitrusts, and pooled income funds.

These trusts must file Form 5227 to disclose information critical for charity oversight, such as income distribution, capital gains, and trustee fees. The form helps the IRS monitor if charitable contributions adhere to federal tax regulations and if the trusts maintain their tax-exempt status.

Steps to Complete IRS Form 5227

Completing Form 5227 requires careful step-by-step adherence to IRS guidelines. Here is a detailed breakdown:

-

Enter Trust Information: Begin by providing basic details like the trust's name, address, employer identification number (EIN), and the trustee's contact information.

-

Identify Trust Type: Specify the type of split-interest trust and whether it operates as a charitable remainder annuity trust, unitrust, or pooled income fund.

-

Report Income: Detail income sources including interest, dividends, and any additional gross income. Calculate total trust income accurately.

-

Calculate Deductions: Enter deductions such as trustee fees, attorney fees, and other administrative expenses. This may also include distributions to non-charitable beneficiaries.

-

Distribute Income: Note the allocations to charitable and non-charitable beneficiaries, highlighting how the income is distributed according to trust agreements.

-

Record Charitable Contributions: Specify any charitable contributions made during the tax year, identifying recipient entities and donated asset types.

-

Complete Signature Section: Ensure that the trustee or an authorized person signs the form to validate the information provided.

Filing Deadlines and Important Dates

Submissions for IRS Form 5227 must be completed by April 15th of the year following the tax year the form covers. Extensions may be requested using Form 8868, though timely submission is encouraged to avoid penalties.

Late submissions might incur penalties, particularly when tax liabilities are underestimated. Trusts should account for additional processing time if filing via mail to meet the deadline.

Required Documents for Form 5227

Preparation for filing Form 5227 involves collating multiple documents:

- Trust instrument to verify trust terms and provisions.

- Previous year's Form 5227 if applicable.

- Statements of account activities, listing income, and expenditures.

- Documentation of asset transfers, sales, or distributions.

- Receipts for charitable contributions made by or to the trust.

Organizing these records will ensure accurate recording and reporting on the form.

Key Elements of IRS Form 5227

The key elements of Form 5227 that influence trust compliance include:

- Income Reporting: Capture all types of income, emphasizing proper allocation.

- Distributions: Clearly identify and calculate both charitable and non-charitable distributions.

- Deduction Listings: Document all eligible deductions, supporting operational transparency.

- Charitable Contributions: Highlight contributions with specific details of recipients and donated amounts.

Accurate data entry in these sections is critical to trust compliance and monitoring.

IRS Guidelines and Instructions

The IRS provides extensive guidelines for completing Form 5227, accessible online at their official website. These instructions cover each line item, offering explanations and examples to guide filers through complex sections of the form. Compliance with these guidelines ensures accurate reporting and minimizes errors.

Trustees can consult these resources to clarify questions during the filing process or to correct previous submissions.

Penalties for Non-Compliance

Failure to file IRS Form 5227 on time or submitting inaccurate information can lead to significant penalties. These can include:

- Monetary Penalties: Fines calculated based on unpaid tax or misreported amounts.

- Loss of Tax-Exempt Status: Non-compliance may affect the trust's ability to maintain tax exemption.

Ensuring thorough and timely submission of the form is essential in preserving a trust's favorable tax status and avoiding financially burdensome penalties.

Digital vs. Paper Submission Options

Form 5227 can be submitted digitally or on paper. Electronic submission through the IRS's online platforms is promoted for its efficiency and expedited processing. It minimizes errors associated with manual entry and provides timely confirmation upon receipt.

Paper submissions remain valid but necessitate longer processing times and an increased risk of misplacement or delay. Trustees must choose the method that aligns best with their resources and timelines.