Definition & Meaning

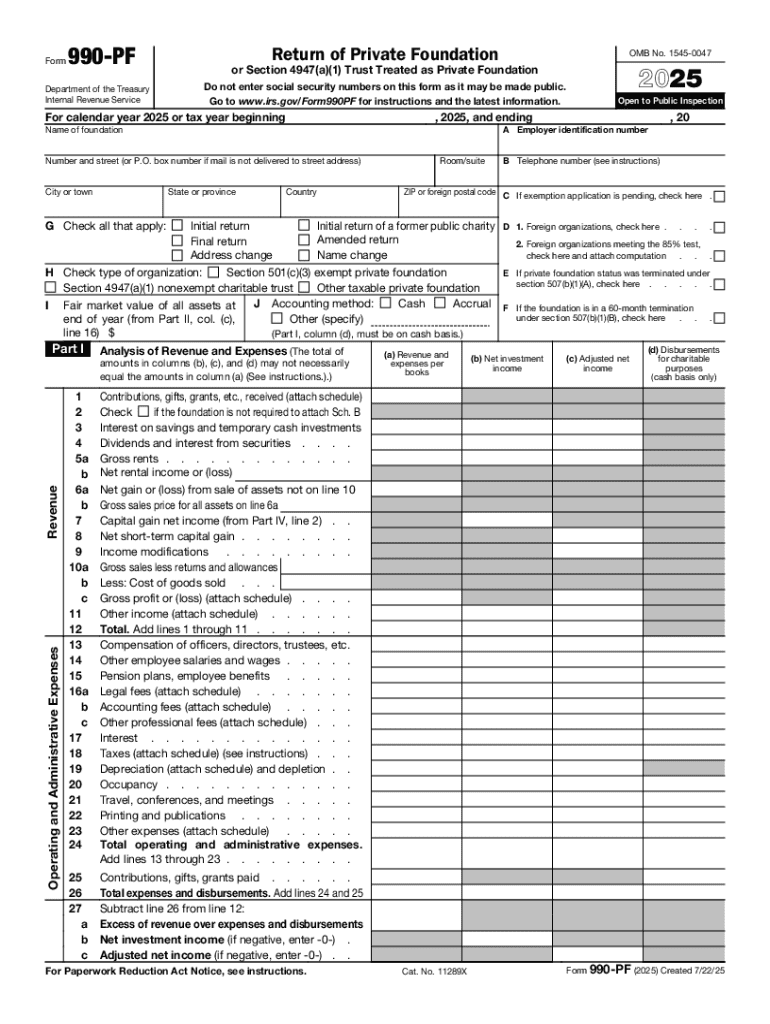

The 2025 Form 990-PF, "Return of Private Foundation or Section 4947(a)(1) Trust Treated as Private Foundation," is a tax document mandated by the IRS for private foundations and certain trusts that are treated as private foundations. This form serves multiple purposes, including providing the IRS with essential information about the foundation’s financial activities, charitable distributions, and compliance with tax laws. By detailing the financial transactions and activities of a private foundation, this form ensures that these organizations adhere to the regulations concerning their tax-exempt status. This form also prompts organizations to remain transparent about their finances and operations, assisting regulators, donors, and the public in understanding how funds are utilized and missions fulfilled.

Key Elements of the 2025 Form 990-PF

Certain sections within the 2025 Form 990-PF are critical for a comprehensive representation of a private foundation's financial standing and compliance status. The form includes sections for recording the foundation’s income, expenses, assets, and liabilities. It also requests detailed information on charitable distributions to ensure compliance with minimum distribution requirements. Additionally, the form requires disclosure of minimum investment returns, taxable expenditures, relationships with disqualified persons, and information on officers, directors, trustees, and other employees. Each section is designed to capture specific data, which collectively helps regulators ascertain if the foundation is maintaining its tax-exempt status in line with legal requirements.

Detailed Breakdown

- Income and Expenses: Outline all revenue streams and expenditures, enhancing transparency of financial activities.

- Assets and Liabilities: Provide insight into the foundation's financial health and operational capacity.

- Charitable Distributions: Ensure compliance with mandatory payout requirements, providing a list of grants made.

- Foundation Management and Compensation: Require details of the foundation’s governance structure and any payments made to insiders.

Steps to Complete the 2025 Form 990-PF

Completing the Form 990-PF involves several key steps, from data gathering to final submission. Here's a simplified process to guide you:

- Gather Financial Records: Collect all relevant financial documents, including income statements, balance sheets, transaction records, and details of charitable distributions.

- Accurate Data Entry: Carefully enter the financial data into the appropriate sections of the form, ensuring accuracy and consistency with underlying records.

- Review Legal Compliance: Ensure that all required disclosures are made, and cross-check for compliance with IRS regulations and guidelines.

- Consult Professionals: Consider seeking assistance from tax professionals to verify accuracy and enhance understanding, particularly for complex financial arrangements.

- Submission: File the form by the due date using an accepted method, ensuring all sections are complete and the form is accompanied by any requisite attachments.

How to Obtain the 2025 Form 990-PF

Obtaining the Form 990-PF is straightforward. It can be downloaded directly from the IRS website in a fillable PDF format. Tax professionals and accounting firms often have copies available for use and distribution. Additionally, tax preparation software like TurboTax and QuickBooks can import the form, providing users an integrated platform to prepare and submit their filings efficiently. This accessibility ensures that foundations of all sizes can comply with filing requirements without undue burden.

Who Typically Uses the 2025 Form 990-PF

The primary users of the Form 990-PF are private foundations and certain trusts classified under Section 4947(a)(1) of the Internal Revenue Code. These entities are usually non-profit organizations with substantial endowments, whose financial transactions and operations are subject to oversight due to their tax-exempt status. These organizations utilize the form to report their annual financial activities, ensuring transparency and adherence to regulatory requirements. Additionally, professional advisors and accountants frequently work with these organizations to ensure the accurate completion and submission of the form.

IRS Guidelines

The IRS provides comprehensive guidelines to help private foundations accurately complete and file the Form 990-PF. These guidelines outline the specific reporting requirements, filing deadlines, and the necessary record-keeping practices. Understanding these directions is essential for maintaining compliance and avoiding potential penalties. The IRS periodically updates these guidelines, particularly when there are changes to tax laws or filing procedures, emphasizing the importance of reviewing the most current information before filing.

Real-World Scenarios

- Scenario One: A small private foundation receiving significant donations needs to accurately report its financial standing to the IRS using the Form 990-PF. By adhering to IRS guidelines, they maintain their tax-exempt status.

- Scenario Two: A trust treated as a private foundation must disclose its investment returns and distributions, ensuring compliance with payout requirements and maintaining transparency.

Filing Deadlines / Important Dates

For the 2025 taxation year, private foundations generally must file Form 990-PF by the 15th day of the 5th month after the end of their fiscal year. This means that for organizations operating on a calendar year, the deadline is typically May 15th, 2026. Foundations can request an extension by filing Form 8868, which grants additional time to file, but not to pay any taxes owed. It is crucial to observe these deadlines to avoid late filing penalties, which can be substantial.

Penalties for Non-Compliance

Non-compliance with filing requirements for the Form 990-PF can result in significant penalties. The IRS imposes a daily penalty for late filings, which can accrue up to a maximum depending on the size of the foundation's gross receipts. Additionally, the failure to submit complete or accurate information may result in further scrutiny from the IRS and could jeopardize the foundation's tax-exempt status. Private foundations must be diligent in fulfilling filing requirements to prevent financial penalties and ensure ongoing compliance with tax laws.