Definition & Meaning

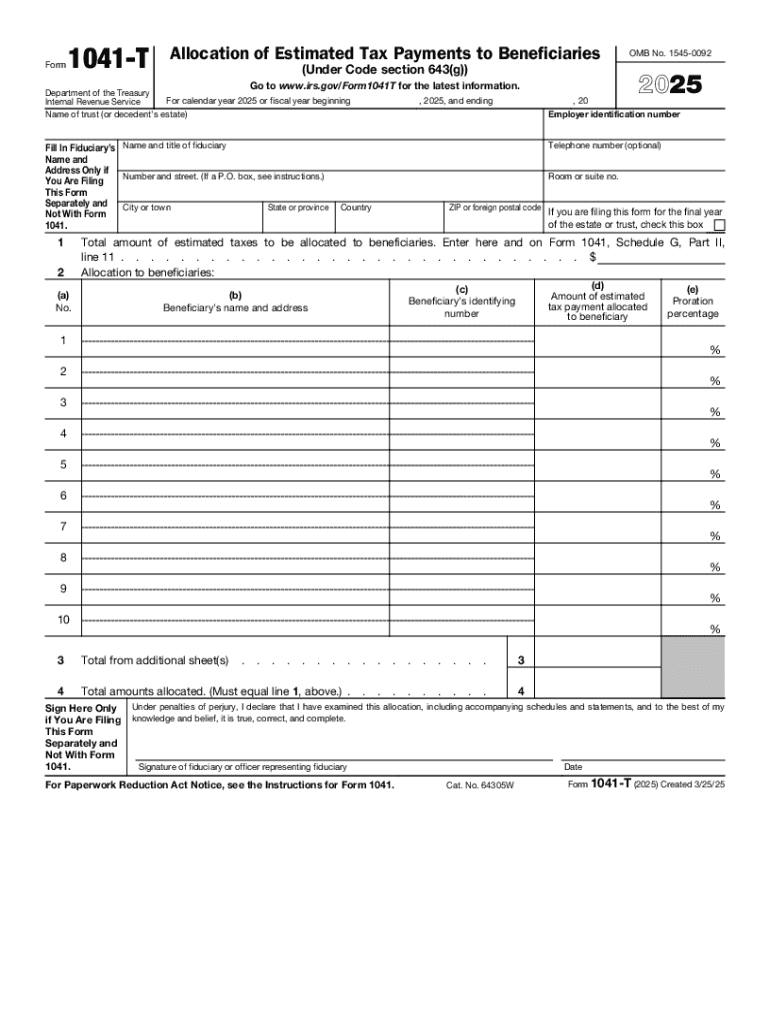

The 2025 Form 1041-T, officially titled "Allocation of Estimated Tax Payments to Beneficiaries," is utilized by fiduciaries of estates or trusts to allocate a portion of estimated tax payments to beneficiaries. This allocation, under Code section 643(g), is critical in ensuring that beneficiaries receive accurate tax credits. By filing this form, a fiduciary can allow beneficiaries to use allocated tax amounts as credits against their individual income tax obligations. Understandably, this is a strategic tool to optimize tax assessments for both the fiduciary entity and its beneficiaries.

Importance of Allocation

- Tax Efficiency: By allocating estimated tax payments, fiduciaries can manage tax liabilities more effectively.

- Beneficiary Benefits: Allows beneficiaries to apply credits directly against their tax returns, potentially reducing their overall tax liabilities.

Practical Implications

- Accurate Record-Keeping: Requires precise accounting and record maintenance by fiduciaries.

- Impacts Estate Planning: Integral in crafting estate and trust distributions, affecting financial planning strategies.

Steps to Complete the 2025 Form 1041-T

Filling out the 2025 Form 1041-T requires attention to specific details. Here's a breakdown of the process:

-

Fiduciary Details:

- Enter the fiduciary's name, address, and taxpayer identification number.

- List the estate or trust's name and identification number.

-

Beneficiary Identification:

- Include each beneficiary's name, social security number, and address for accurate tax credit allocation.

-

Tax Payment Allocation:

- Specify the total estimated tax payments to be allocated.

- Detail the amounts allocated to each beneficiary.

-

Submission Timing:

- Ensure submission by the fiduciary's tax return filing date to implement allocations for the beneficiaries' current tax year.

Common Pitfalls

- Incorrect Beneficiary Details: Mismatched names or identification numbers can delay processing.

- Payment Discrepancies: Allocation must exactly match available estimated payments.

Who Typically Uses the 2025 Form 1041-T

The form is primarily used by fiduciaries managing estates or trusts. Here's a closer look at potential users:

Fiduciary Roles

- Trustees: Often responsible for managing trusts on behalf of multiple beneficiaries.

- Estate Executors: Handle post-mortem estate tax obligations and beneficiary allocations.

Beneficiary Demographics

- Individual Beneficiaries: Often include family members or designated heirs.

- Charitable Organizations: Trusts may allocate to charitable institutions for tax credits under specific conditions.

Key Elements of the Form 1041-T

Understanding its key components helps accurately complete and file the form:

- Total Estimated Taxes: Critical figure reflecting all estimated taxes paid by the estate/trust.

- Allocation Breakdown: Detailing of tax credit portions for each beneficiary.

- Fiduciary Certification: Signature and declaration of fiduciary responsibility and accurate information provision.

Real-World Examples

- Simple Trusts: Allocate income annually, directing proportional credits to current beneficiaries.

- Complex Trusts/Estate Executions: May involve varied allocation strategies depending on current income, principal distributions, or specific estate planning goals.

Filing Deadlines / Important Dates

Timely filing is crucial for the effectiveness of the allocations and involves adhering to IRS deadlines:

- April 15th: Generally coincides with the standard tax filing deadline.

- Extensions: While possible, extensions can impact beneficiary tax return filings if not effectively coordinated.

Date Considerations

- Fiduciary Tax Year: Dictates the specific filing timeline.

- Beneficiary Impacts: Delays affect when beneficiaries can claim their assigned tax credits.

IRS Guidelines for Form 1041-T

Adhering to IRS stipulations ensures compliance and effective processing:

- Form Integrity: Must be submitted with accurate information and no significant alterations.

- IRS Access: Recommended to review the latest IRS updates annually for potential procedural changes.

Compliance Tips

- Record Maintenance: Keep accurate internal records to back filed allocations.

- Audit Preparedness: Have transparent methods and paper trails for allocation decisions ready if needed.

Penalties for Non-Compliance

Fiduciaries face specific penalties and consequences for improper or delayed filings:

- Monetary Fines: Potential fines for inaccurate allocations or omitted beneficiary information.

- Legal Repercussions: Increased scrutiny or audits following significant filing errors.

Minimizing Risks

- Double-Check Filings: Utilize fiduciary management software to validate form accuracy.

- Consult Tax Professionals: Seek expert advice for complex trusts or estate situations.

Examples of Using Form 1041-T

Several scenarios highlight form utilization and related complexities:

- Family Trusts: Annually allocate to minor children, simplifying their tax filing while funding educational savings.

- Philanthropic Trusts: Allocate to beneficiaries, optimizing tax benefits for involved non-profits.

Variation Insights

- Trust Nature: Differences between revocable vs. irrevocable nature impact allocation strategies.

- Beneficiary Types: Regularly review allocations for varying beneficiary or organizational tax statuses.