Definition & Meaning

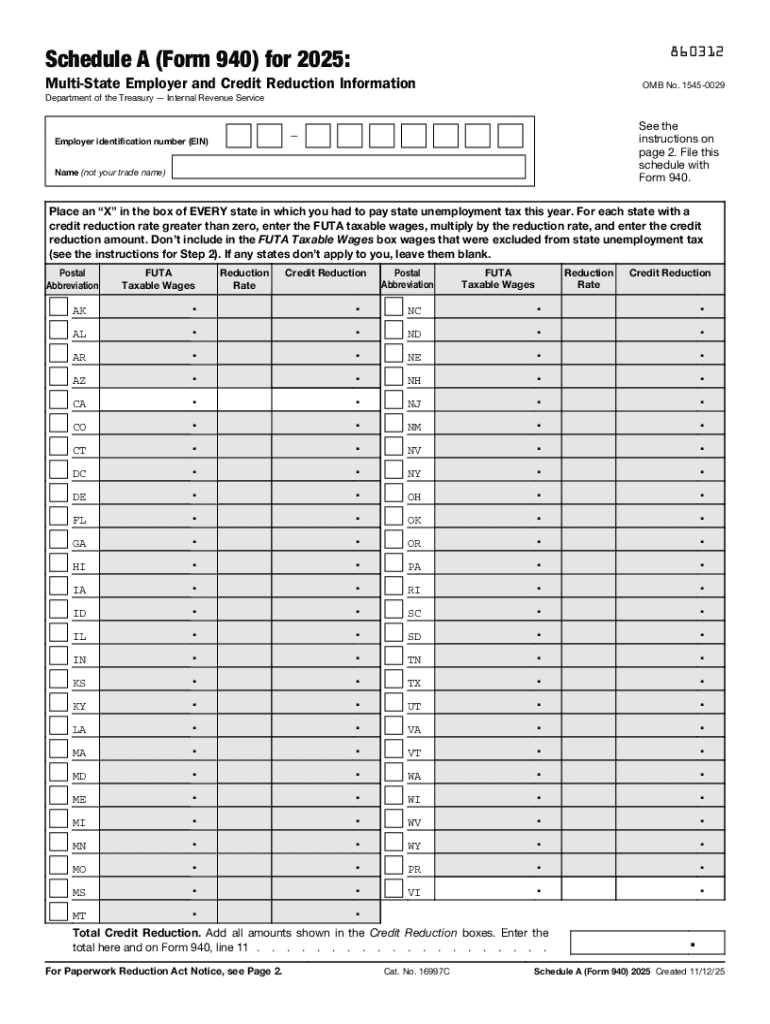

Schedule A (Form 940) is a supplementary form used by multi-state employers to report unemployment tax obligations, particularly focusing on credit reduction states. A credit reduction state is one that has not repaid money it borrowed from the federal government to cover unemployment benefits. As a result, employers in these states face a reduced credit against the federal unemployment tax rate. This form is essential for accurately calculating the total federal unemployment tax (FUTA) owed, ensuring compliance with federal requirements.

Credit Reduction Mechanism

A credit reduction affects the extent to which employers can offset state unemployment insurance taxes against the federal taxes. The standard FUTA tax rate is 6%, but employers typically receive a 5.4% credit for state unemployment taxes, reducing the effective rate to 0.6%. However, in credit reduction states, this credit is reduced, increasing the tax liability.

Importance for Multi-State Employers

For businesses operating in multiple states, this form helps systematically report and manage variations in unemployment tax obligations. It ensures that businesses accurately account for different state regulations and credit reductions affecting their tax responsibilities.

How to Use the Schedule A (Form 940)

Understanding the Structure

Schedule A (Form 940) involves detailing the FUTA taxable wages paid in credit reduction states and calculating the additional taxes due. The form includes fields for listing wages and determining the total credit reductions based on each state’s specific rates.

Practical Use

- Gather Wage Data: Compile data on the wages paid in each state.

- Identify Credit Reduction States: Use IRS resources to identify states with credit reduction statuses.

- Calculate Additional Tax: Compute the extra tax based on the credit reduction rate, which will be utilized to reconcile your federal tax obligations.

Software Integration

Employers often utilize accounting software such as QuickBooks or TurboTax that supports the completion of Schedule A (Form 940), simplifying the reporting process.

Steps to Complete the Schedule A (Form 940)

- Review IRS Notices: Check the IRS website or related notices to identify if your states of operation are subject to credit reductions.

- Calculate FUTA Taxable Wages: Determine the wages that fall under FUTA liability for each state.

- Fill in State Details: Enter each state's name along with the respective FUTA wages.

- Compute Credit Reduction: Apply the credit reduction rate to the wages to compute the additional tax due for each state.

- Summarize Total Addition: Summarize the additional taxes and transfer the total to Form 940.

Key Elements of the Schedule A (Form 940)

State Identification

Each state involved must be correctly identified, and their respective FUTA taxable wages accurately recorded.

Calculation Accuracy

The accurate application of credit reduction rates to the correct wage amounts is crucial for determining the precise additional tax owed.

Compliance Assurance

Completing this schedule guarantees compliance with federal tax obligations, avoiding potential penalties for inaccurate tax reporting.

Important Terms Related to Schedule A (Form 940)

Credit Reduction State

A designation given to states that owe the government for unpaid unemployment funds, which elevates their employer tax obligations.

FUTA Wage Base

The total amount of wages subject to federal unemployment tax per employee per calendar year, determining how much tax needs to be paid.

Taxable Wages

Employee earnings on which unemployment taxes are computed; crucial to calculating both state and federal unemployment taxes.

State-Specific Rules for the Schedule A (Form 940)

Variation Among States

Different states may have divergent rules and tax rates that require careful attention when completing the form. Consistent monitoring of state legislation updates is necessary.

Tax Rate Adjustments

Employers must stay informed about any legislative changes at the state level that alter credit reduction rates, influencing federal tax liability.

Filing Deadlines / Important Dates

Annual Filing Deadline

Schedule A (Form 940) must accompany Form 940, submitted annually by January 31 following the calendar year being reported.

Early Submission and Documentation

Employers are encouraged to gather necessary documents early and submit them as part of comprehensive tax filings to ensure accuracy and timely processing.

Penalties for Non-Compliance

Financial Repercussions

Failing to file Schedule A (Form 940) correctly can result in IRS-imposed penalties and interest on unpaid taxes resulting from inaccurate credit reductions.

Mitigation Strategies

Employers should regularly verify compliance requirements and consider engaging professional accounting services to prevent errors in filing and calculation.