Definition & Meaning

Form 1041-QFT (Rev December 2025) is the U.S. Income Tax Return for Qualified Funeral Trusts (QFTs), issued by the Internal Revenue Service (IRS). A QFT refers to a trust set up to manage funds specifically for funeral expenses, benefiting the trust's designated beneficiaries. The form serves as a tax return to report the income, deductions, tax computation, and payments connected to a QFT’s financial activities for a designated tax year. This means that trustees of qualified funeral trusts need to use this form to disclose financial information related to the management of the funeral trust, ensuring compliance with tax laws.

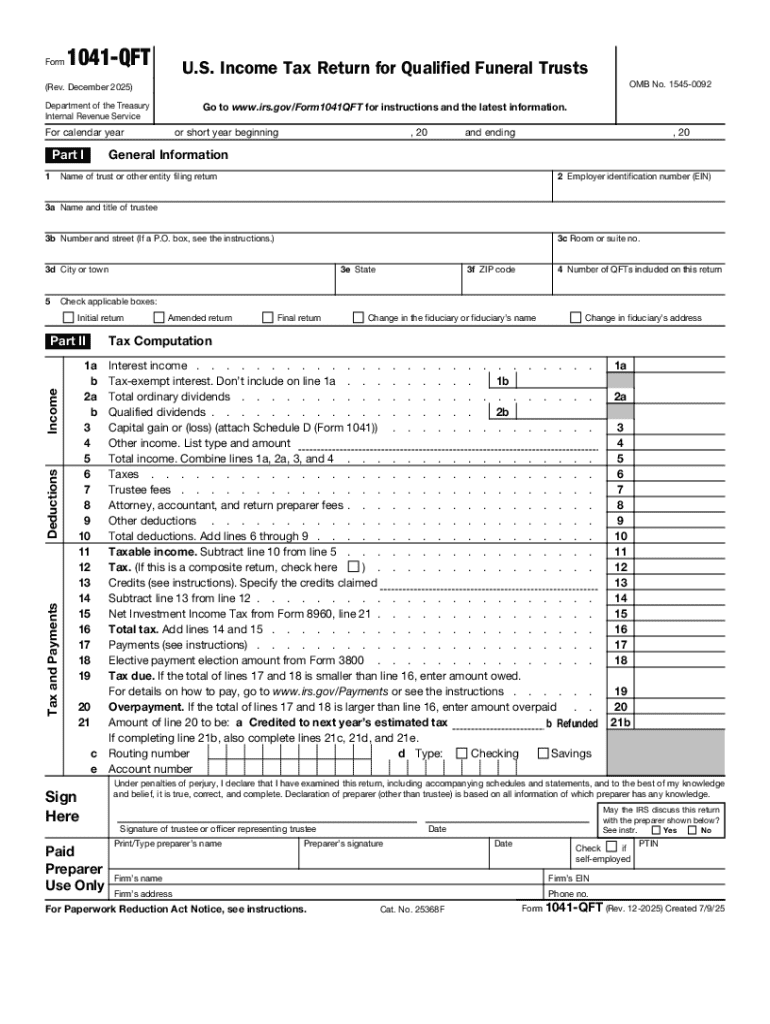

Steps to Complete the Form 1041-QFT (Rev December 2025)

Filing Form 1041-QFT requires careful adherence to IRS guidelines to ensure accuracy and compliance. The process involves several steps:

-

Gather Necessary Information: Collect all relevant data, including the trust's EIN, financial records showing income and expenses, and beneficiary details.

-

Fill in General Information: Complete the preliminary sections with the QFT's name, address, Employer Identification Number (EIN), and the tax year.

-

Report Income: Document all income received by the trust, such as dividends, interest, and capital gains, on the respective lines as indicated in the form.

-

Deductions: List allowable deductions, including expenses directly related to the trust's administration. Ensure to differentiate between deductible and non-deductible expenses to avoid discrepancies.

-

Calculate Tax: Use the provided tax computation sections to determine the trust's taxable income and the associated tax liability.

-

Complete Payments and Credits: Note any payments made throughout the year, such as estimated tax payments, and apply credits where applicable to reduce tax liability.

-

Signing and Filing: Ensure the form is signed by the trustee managing the trust before submission. Retain a copy for internal records and compliance checks.

Who Typically Uses the Form 1041-QFT (Rev December 2025)

The primary users of Form 1041-QFT are trustees of Qualified Funeral Trusts. These individuals are responsible for managing funds allocated for funeral expenses, primarily set aside to ensure that beneficiaries do not bear the financial burden when funeral services are required. Typically, these trustees may include:

- Funeral service providers: Acting as fiduciaries managing pre-allocated funds.

- Designated trust officers or legal firm representatives: Handling financial and tax matters for the trust.

- Dedicated financial advisors or accountants: Providing specialized insight into tax-related implications for the trust.

These users must possess detailed knowledge about trust administration and tax reporting to efficiently complete the form.

Who Issues the Form

Form 1041-QFT is issued by the Internal Revenue Service (IRS), a U.S. government agency responsible for tax collection and enforcement. The IRS provides the most up-to-date forms, instructions, and guidelines regarding the completion and filing of the document. Taxpayers can access the form through the IRS website or request a physical copy through standard mail from IRS offices.

Filing Deadlines / Important Dates

The deadline for filing Form 1041-QFT aligns with the U.S. tax return schedule:

- Annual Filing: The form is due on the 15th day of the 4th month following the end of the trust's tax year. For calendar-year trusts, this is typically April 15.

- Extension: Trustees can file Form 7004 to request a six-month extension if additional time is required to complete the form.

Missing these deadlines may result in penalties and interest, emphasizing the importance of timely and accurate filing.

Required Documents

When preparing Form 1041-QFT, trustees need to gather several documents to ensure complete information:

- Trust Agreement: Verifying the existence and terms of the trust.

- Financial Statements: Documenting income, expenses, gains, and losses.

- Beneficiary Details: Identifying individuals for whom the funds are set aside.

- Previous Tax Returns: Providing a reference for continuity and comparison.

Accurate documentation is critical to ensure compliance with IRS regulations and avoid potential audits.

Penalties for Non-Compliance

Failure to comply with the IRS filing requirements for Form 1041-QFT can lead to several penalties:

- Late Filing Penalty: A percentage of the unpaid tax, assessed monthly.

- Inaccurate Information Penalty: Penalties are imposed for incorrect declarations or omissions.

- Interest on Unpaid Taxes: Accrued from the original due date until payment is made.

These penalties highlight the necessity for trustees to maintain comprehensive and accurate records and adhere to filing deadlines.

Software Compatibility (TurboTax, QuickBooks, etc.)

To assist in the preparation and filing process, several tax software platforms support Form 1041-QFT:

- TurboTax: Known for user-friendly interfaces and comprehensive tax preparation tools.

- QuickBooks: Offers integration for financial tracking and reporting.

- H&R Block Tax Software: Provides step-by-step guidance tailored for trusts.

Using compatible software can simplify data entry, reduce errors, and ensure compliance with tax regulations while easing the administrative burden of managing a QFT's tax affairs.

IRS Guidelines

The IRS provides comprehensive guidelines within the instructions for Form 1041-QFT:

- Eligibility criteria: outlines which trusts qualify as a QFT and should use this form.

- Filing instructions: Detailed steps for accurately completing the form.

- Deductions and credits: Lists qualifying expenses and available credits for trusts.

These guidelines are crucial for ensuring compliance and providing a roadmap for trustees who manage funeral trust finances.