Definition & Meaning

Form 8840, officially called the "Closer Connection Exception Statement for Aliens," is a tax document used by non-resident aliens in the United States. It helps these individuals establish a closer connection to a foreign country, exempting them from being considered a U.S. resident under the substantial presence test. This form is crucial for those who wish to avoid being taxed as U.S. residents, despite significant time spent in the U.S. It requires detailed information about the individual's tax home, significant contacts with foreign countries, and visa status.

Eligibility Criteria

To be eligible to file Form 8840, an individual must meet specific criteria:

- Non-U.S. Citizen: The filer must not be a U.S. citizen.

- Presence in the U.S.: The individual still needs to meet the substantial presence test, which generally involves spending 31 days in the U.S. during the current year and 183 days over a three-year period, calculated using a specific formula.

- Closer Connection: The filer must prove a closer connection to another country. This involves maintaining a tax home and significant cultural, familial, or financial ties to the other country.

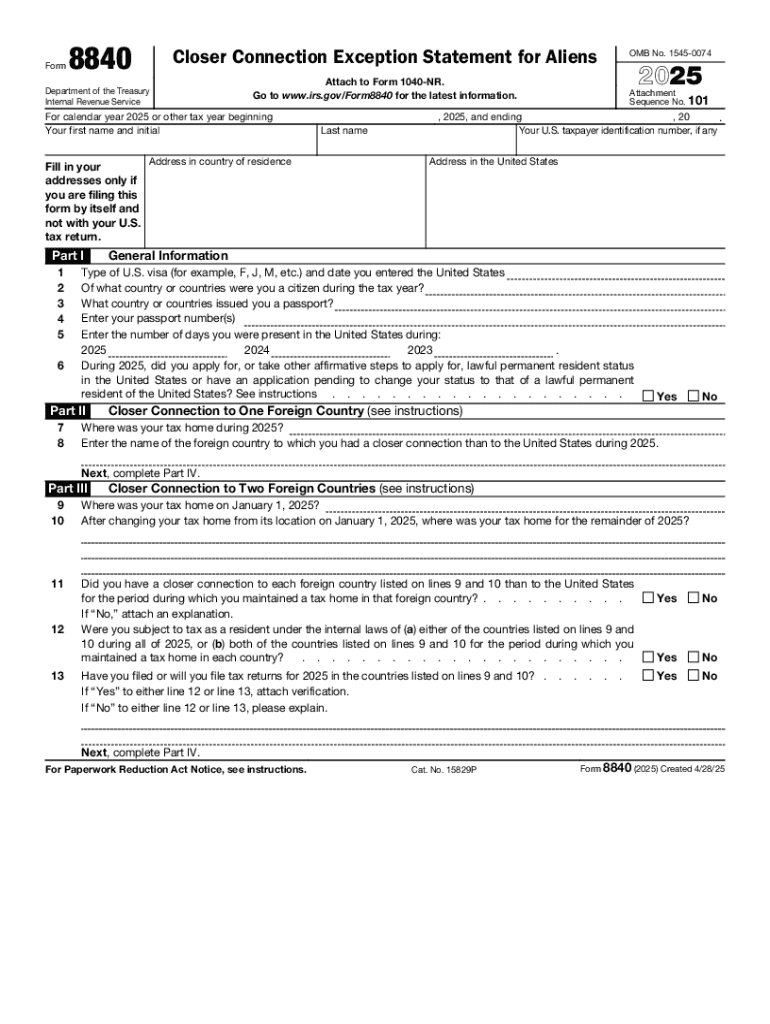

Steps to Complete the Form 8840

- Personal Information: Start by providing your full name, address, and taxpayer identification number (TIN).

- Days of Presence: Calculate and enter the number of days you spent in the U.S. over the current year and the previous two years.

- Visa Status: Indicate your current U.S. immigration status, including the type of visa held during your stay.

- Foreign Connection: Detail your tax home and primary ties to the foreign country, such as property ownership, family members, or employment.

- Signature and Date: Ensure the form is signed and dated to validate your declaration.

Required Documents

When filing Form 8840, you should be prepared to provide additional documentation:

- Visa Records: Copies of your U.S. visa and entry/exit records to support your absence or presence in the U.S. during the specified periods.

- Proof of Foreign Ties: Documents such as foreign tax return filings, property ownership, and proof of immediate family members residing abroad.

- Travel Itinerary: Detailed records of your travel history, including entries and exits from the U.S.

IRS Guidelines

The IRS provides specific guidelines for completing Form 8840:

- Ensure that the form is filed annually along with your U.S. tax return, even if you do not owe taxes as a non-resident.

- Retain copies of all documentation supporting your closer connection claim for at least three years.

- Be accurate and truthful in the information provided, as misrepresentation can lead to penalties and denied claims.

Filing Deadlines / Important Dates

The deadline for submitting Form 8840 is the same as the filing deadline for U.S. tax returns, typically April 15th of the following year. If an extension is granted for your tax return, this also applies to Form 8840. It's essential to file on time to avoid penalties or unwanted tax implications.

Penalties for Non-Compliance

Failure to file Form 8840 when required can result in being treated as a U.S. resident for tax purposes, leading to:

- Increased Tax Liability: Potential taxation on worldwide income at U.S. rates.

- Fines and Interest: Penalties for late filing and interest on any underpaid taxes.

- Audit Risks: Increased scrutiny from the IRS in subsequent filings.

Who Issues the Form

The Internal Revenue Service (IRS) issues Form 8840. It is available for download from the IRS website and may also be accessed through tax preparation software like TurboTax. The form is intended for use by individuals and is not typically filed by businesses or partnerships.

Digital vs. Paper Version

Form 8840 can be completed and submitted in both digital and paper formats:

- Digital Submission: Benefits include faster processing and immediate acknowledgement of receipt by the IRS. It can be filed through e-file systems or compatible tax software.

- Paper Submission: Although it takes longer to process, a paper form can be sent by mail if preferred. Ensure that it's postmarked by the filing deadline to avoid delays.