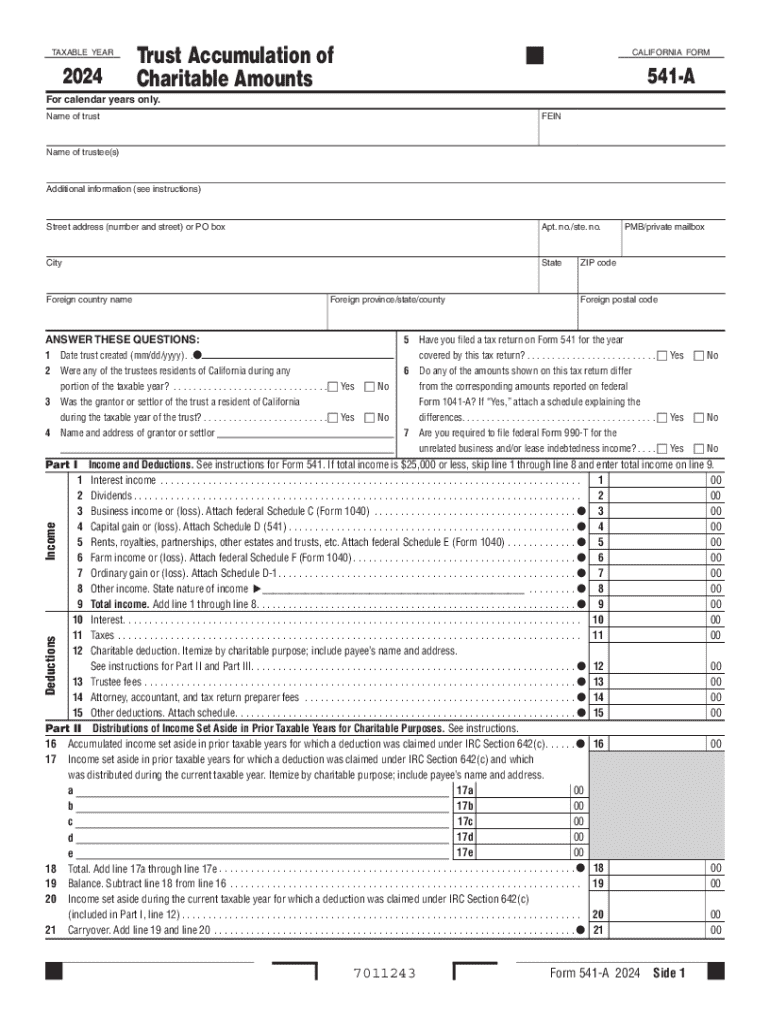

Definition and Purpose of Form 541-A

Form 541-A, in the context of California taxation, is specifically designed for trusts that accumulate charitable amounts. It involves detailed reporting of the trust's income, deductions, and distributions made for charitable purposes. This form plays a crucial role in documenting how the funds within the trust are managed and distributed, ensuring compliance with state tax regulations.

The primary sections include comprehensive input on trust identification, detailed breakdowns of income and deductions, and an overview of distributions earmarked for charitable activities. Trusts must accurately report all income sources and any deductions claimed to reflect the financial activities objectively.

Step-by-Step Instructions to Complete Form 541-A

-

Begin with Trust Identification:

- Enter the name and address of the trust.

- Provide the employer identification number (EIN).

- Confirm the trust's fiscal year.

-

Detail Income Sources:

- List various income streams such as interest, dividends, and capital gains.

- Include any tax-exempt income.

-

Document Deductions:

- Itemize administrative and operational expenses.

- Include deductions for trustee fees and any legal expenses incurred.

-

Summarize Charitable Distributions:

- Report amounts specifically distributed for charity.

- Ensure these match with the trust's stated purpose and intentions.

-

Review and Respond to Compliance Queries:

- Answer questions regarding prior tax filings.

- Declare the residency status of trustees and grantors.

-

Finalize Financial Statements:

- Complete the balance sheet sections.

- Double-check all figures for consistency and accuracy.

Tax Filing Requirements and Deadlines

The due date for submitting Form 541-A aligns with regular tax filings, typically on the 15th day of the fourth month following the close of the trust's tax year. For the 2024 tax year, trusts should ensure submission by April 15, 2025, unless an extension is granted.

Extensions can be requested if necessary, but the trust must still estimate and pay any taxes owed by the original deadline to avoid penalties. Keeping track of these timelines is crucial for maintaining compliance and avoiding unnecessary late filing fees.

Legal Use and Compliance Requirements

Form 541-A serves as an official document under state tax law to ensure transparency in how trusts manage and allocate funds designated for charitable purposes. Adherence to the legal framework is essential, as improper filing or fraudulent reporting may result in penalties or legal action.

Trust administrators are responsible for maintaining accurate and complete records for audit purposes. All figures reported on the form must correlate with actual transactions and distributions made during the fiscal year.

Required Documents for Form Submission

Trusts must submit several supporting documents alongside the Form 541-A:

- Financial Statements that corroborate income and expenses listed.

- Charitable Receipts or other proofs of distribution for validation.

- Prior Tax Filings if the form requires historical comparison data.

Ensuring all these accompany the form can help prevent delays or rejections due to incomplete submissions.

Importance of IRS Guidelines

Adhering to IRS guidelines is imperative when completing Form 541-A, as any inconsistency with federal tax regulations can result in discrepancies. While Form 541-A is specific to California, IRS guidance often provides a foundational basis for general compliance. Trusts must ensure that their state filings align with federal requirements to prevent audits and other issues.

State-Specific Rules for California

California has unique requirements for how trusts should manage and report their charitable distribution activities. Trust administrators should be well-versed in state-specific tax codes that relate to deductions and exemptions to prevent potential non-compliance issues.

Besides the Form 541-A, maintaining awareness of any changes in state legislation that affect trust taxation and reporting can ensure ongoing compliance and minimize penalties.

Penalties for Non-Compliance

Failure to properly file Form 541-A can result in significant penalties for the trust. These may include fines for late submission, inaccuracies in reported data, or even more severe financial repercussions if the IRS or California tax authorities find substantial discrepancies during audits.

Trust administrators are advised to establish rigorous internal controls and review processes to ensure that the form is completed accurately and submitted timely. Regular reviews with tax professionals can aid in mitigating risks associated with non-compliance.