Definition and Purpose of Form VAT652

The VAT652 form, issued by HM Revenue and Customs (HMRC), is designed for UK importers and their representatives to voluntarily declare any underpayment of customs duties and VAT. This form is crucial for rectifying any discrepancies in previously submitted customs declarations. It provides a structured approach to ensure compliance with tax laws by allowing a systematic process for amending clearance details when underpayments are identified.

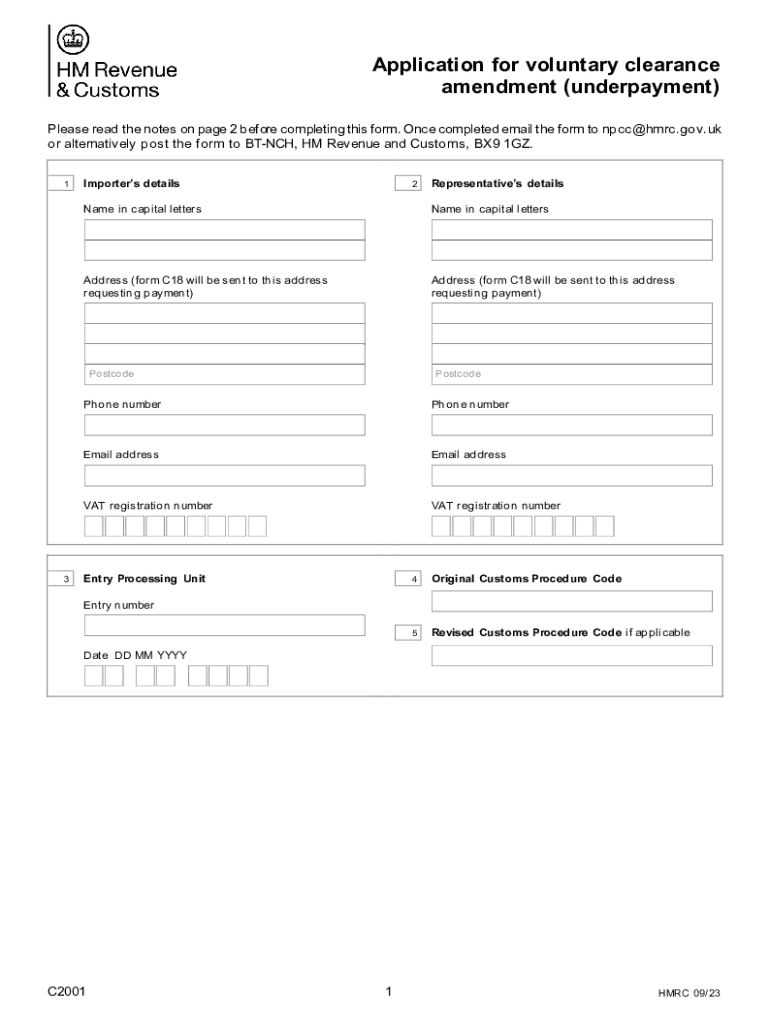

How to Use Form VAT652

To effectively use the VAT652 form, it's important to comprehend its structure and requirements thoroughly. Start by gathering all relevant documentation that will support your amendment. Typical documents include original customs filings, invoices, and any communications related to the import. The form must be filled out precisely according to the instructions provided by HMRC to ensure accuracy and prevent processing delays.

Steps to Complete Form VAT652

- Review the Form Instructions: Before filling out the form, thoroughly read the accompanying guidelines to understand the information HMRC requires.

- Gather Supporting Documents: Collect all necessary documents that substantiate the need for an amendment, such as proof of incorrect tariff classification or valuation errors.

- Fill Out the Form Accurately: Enter all details, including personal identification, original declaration information, and specifics of the underpayment.

- Submit the Form: Send the completed form and accompanying documentation to HMRC via the submission method specified in the form instructions.

Who Typically Uses Form VAT652

Form VAT652 is primarily utilized by importers within the UK who are required to amend previously filed customs and VAT duties due to underpayment. Representatives such as customs agents or brokers acting on behalf of importers may also fill out this form. It ensures businesses comply with tax obligations by voluntarily correcting any discrepancies, preventing potential penalties from HMRC.

Legal Use and Implications

Using the VAT652 form correctly is essential for legal compliance. It provides a formal mechanism to declare underpayments voluntarily before HMRC identifies these errors through audits. Submission of this form can mitigate penalties associated with undeclared customs duties and VAT by demonstrating proactive compliance.

Key Elements of Form VAT652

Key components of the VAT652 form include:

- Importer Details: Name, address, and VAT registration number.

- Original Declaration Information: Reference number, date of original submission, and port of entry.

- Amendment Details: Description of error, corrected amounts, and reasons for the discrepancy.

- Supporting Documentation: Attach relevant documents that corroborate the corrections made.

Examples of Using Form VAT652

Consider a scenario where an importer incorrectly classified goods under a tariff heading with a lower duty rate, leading to underpayment. In such cases, the VAT652 form allows them to voluntarily declare the error and pay the correct amount owed. Another example involves rectifying incorrect valuation on imported items, which led to VAT discrepancies.

Filing Deadlines and Important Dates

While HMRC does not define a statutory deadline for submitting the VAT652 form, it is in the importer’s best interest to do so promptly upon discovering an error. This helps minimize potential penalties and demonstrates good faith in maintaining compliance with VAT regulations.

Required Documents for Submission

- Original Customs Declaration: Initial documents filed during goods importation.

- Invoices and Receipts: To verify the monetary values declared and actual transactions.

- Communication Records with HMRC: Any correspondence related to prior amendments or inquiries.

Penalties for Non-Compliance

Failing to use the VAT652 form to correct underpayments can result in penalties from HMRC. These can include fines based on the value of the duties and taxes owed, plus additional charges for non-cooperation during audits. Voluntary disclosure using the form can substantially reduce these penalties, highlighting the form’s importance in maintaining compliance.

Form Submission Methods

Importers can submit the VAT652 form to HMRC via email or postal services. It is essential to follow the submission instructions accurately, as outlined in the form guidelines. Maintaining copies of submitted documents for records and future reference is also advisable.