Definition and Meaning

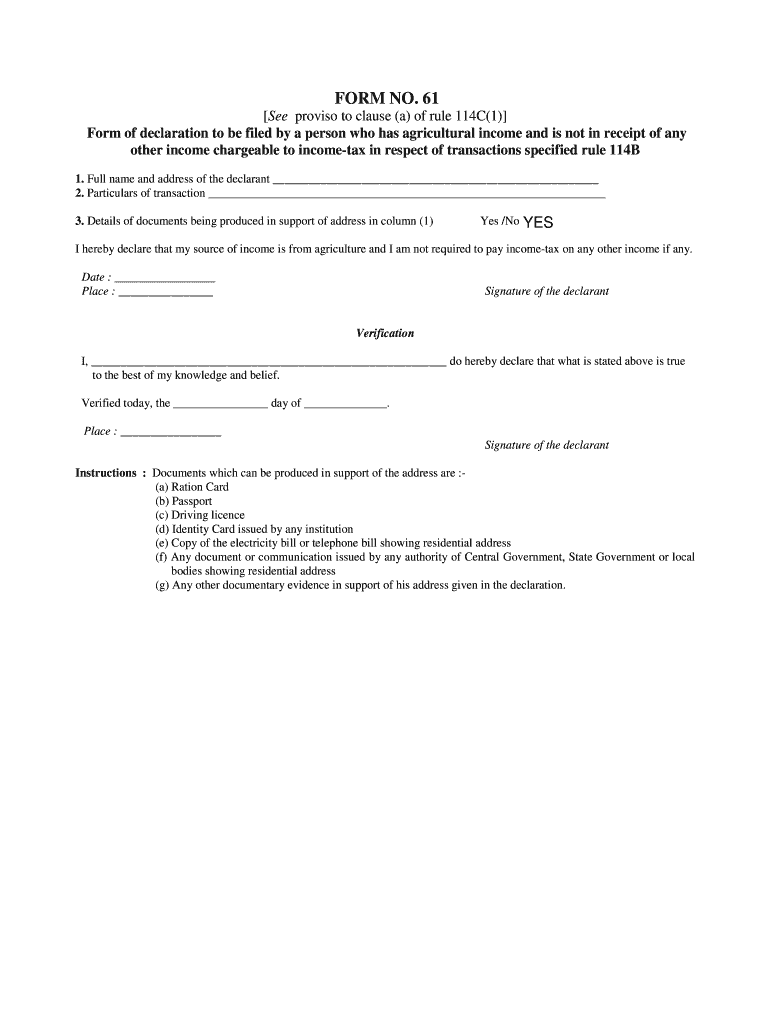

Form No. 61 is a declaration form primarily used by individuals who have agricultural income and no other taxable income in the United States. This document serves to validate that these individuals are not required to file an income tax return under the regular tax laws. By completing Form No. 61, declarants provide personal and transaction details to comply with legal requirements associated with declaring agricultural income.

Key Elements of Form No. 61

The form comprises several sections that are crucial to declaring income accurately. Declarants must include their personal information, such as their full name, address, and contact details. The main body of the form includes fields for specifying the nature and source of agricultural income. Additional documentation, such as proof of agricultural activities and identification verification, may be required to support the claims made in the form.

How to Use Form No. 61

Steps to Complete Form No. 61

- Gather Required Information: Collect personal details and accurate records of agricultural income.

- Fill Personal Details: Enter your full name, address, and contact information in the appropriate sections.

- Detail Income Sources: Specify the type and amount of agricultural income earned.

- Include Supporting Documents: Attach documents that verify your income source and identity, such as a government-issued ID and proof of farmland ownership or lease.

- Verification Section: Carefully read the verification section and sign to confirm that all provided information is accurate and truthful.

Submission Methods

Form No. 61 can be submitted through various methods to ensure it fits the needs of different individuals. Traditionally, it can be mailed to the relevant tax authority. However, an increasing number of taxpayers prefer online submissions for convenience. Some jurisdictions may also allow in-person submissions at local tax offices.

Importance of Form No. 61

This form plays a vital role for individuals with agricultural income who do not qualify for regular tax filings. It ensures compliance with tax regulations without the added burden of filing a standard tax return. Proper submission of Form No. 61 demonstrates a commitment to transparency and adherence to tax laws, reducing the risk of facing legal issues or penalties.

Penalties for Non-Compliance

Failure to submit Form No. 61 when required can result in significant legal repercussions. Penalties may include fines and a potential investigation by tax authorities. Non-compliance increases the risk of being perceived as attempting to avoid tax obligations, even for those whose income falls below taxable thresholds.

Who Typically Uses Form No. 61

Eligibility Criteria

Form No. 61 is specifically designed for individuals who earn their livelihood primarily from agricultural activities and have no other sources of taxable income. This includes farmers, ranchers, and anyone involved in producing crops, livestock, or other related agricultural products.

Taxpayer Scenarios

Various groups use Form No. 61, including:

- Self-employed farmers who rely solely on agriculture for income.

- Retired individuals who have transitioned to agriculture as their sole revenue source.

- Students or part-time workers who engage in farming and do not have taxable income elsewhere.

Legal Use of Form No. 61

Disclosure Requirements

Filing Form No. 61 provides a legal declaration that ensures agricultural income is accounted for in the context of tax regulations without necessitating a full tax filing. Declarants are required to provide accurate and truthful information, as any discrepancies discovered by tax authorities can lead to legal proceedings.

Examples of Using Form No. 61

Practical Scenarios

Consider a scenario where a retired teacher decides to engage in small-scale farming. If the income derived from this activity does not surpass the exemption limit, the individual would utilize Form No. 61 to declare the income without engaging in full tax filing procedures. Similarly, a college student who runs a seasonal farm stand can benefit from this form if farming is their only source of income.

Case Studies

In examining practical cases, consider how small business entities that focus on agricultural production utilize Form No. 61 to streamline their tax-related duties. In a situation where a partnership exists solely to manage a family farm, Form No. 61 helps each partner declare their share of agricultural income efficiently.

State-Specific Rules for Form No. 61

The application of Form No. 61 may vary slightly by state, as each jurisdiction might impose additional requirements or guidelines to supplement federal rules. Some states might require specific forms of documentation to accompany the submission, while others may have unique deadlines or eligibility criteria for using this form.